Sallie Mae 2011 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2011 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

|

|

used by lenders; loan terms, conditions and pricing; consumer protections available to borrowers; and fair

lending considerations. The Dodd-Frank Act also created a “Private Education Ombudsman” within the CFPB to

receive and attempt to informally resolve complaints about Private Education Loans, and the CFPB plans to

receive such complaints through its online consumer complaint system. We are currently working with the CFPB

and providing information relating to these two important initiatives.

The Dodd-Frank Act also authorizes state officials to enforce regulations issued by the CFPB and to enforce

the Dodd-Frank Act’s general prohibition against unfair, deceptive or abusive practices, and makes it more

difficult than in the past for federal financial regulators to declare state laws that differ from federal standards

preempted.

Regulation of Systemically Important Non-Bank Financial Companies

As directed by the Dodd-Frank Act, the Financial Stability Oversight Council (“FSOC”) has proposed a

process for designating non-bank financial companies as systemically important. The Dodd-Frank Act mandated

the development of such a process through which the FSOC would identify and designate non-bank financial

companies whose material financial distress could pose a threat to the financial stability of the United States. If

designated as a systemically important financial institution (i.e., a “SIFI”), a non-bank financial company will be

supervised by the Board of Governors of the Federal Reserve System (the “FRB”) and be subject to enhanced

prudential supervision and regulatory standards to be developed by the FRB. For a further discussion of the risks

and implications of SLM Corporation being designated a SIFI, see Item 1A “Risk Factors — Regulatory and

Compliance.”

In October 2011, the FSOC published additional proposed rulemaking regarding the designation process.

While not yet final, the proposed rules focus the process for determining if a non-bank financial company’s

distress could pose a threat to the financial stability of the United States on three criteria: the size, substitutability

and interconnectedness of the particular company. The proposed rules also stipulate the criteria the FSOC will

utilize to focus on the likelihood of material distress within a non-bank financial company: leverage, liquidity

risk and maturity mismatch, and existing regulatory scrutiny. Presumably, if the FSOC determines a non-bank

financial company does not pose a threat to the financial stability of the United States, no further analysis would

be required. However, the proposed rules shed little light on how the FSOC will conduct its evaluation, only the

criteria it might utilize.

While we have no way of knowing the qualitative judgments the FSOC will use to determine if SLM

Corporation merits SIFI designation, we believe SLM Corporation poses no threat to the financial stability of the

United States. While SLM Corporation would meet certain criteria in Stage 1 of the FSOC’s second proposed

rulemaking, those criteria focus mainly on size and give little or no attention to the nature of the majority of

financial assets on our balance sheet, the minimal interconnectivity between our businesses and the financial

economy of the United States or the numerous sophisticated competitors who can provide substitute services to

those we provide. We believe any review by FSOC should focus primarily on the following:

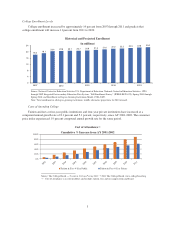

• For AY 2010-2011, we provided approximately one percent of the $235 billion total funds used to finance

post-secondary expenses.(1)

• At December 31, 2011, $138 billion of our $174 billion student loan assets are related to FFELP Loans,

of which at least 97 percent of their principal and interest payments are protected by contractual rights to

recovery from the United States. As previously noted, FFELP was ended by Congress in 2010 and as a

result, these amounts will continue to decline in future years.

• Our annual charge-offs of FFELP Loans were 0.08 percent of loans in repayment in 2011. We have low

charge-off rates on FFELP Loans given the previously noted federal backing of these loans.

(1) Source: The College Board — Trends in Student Aid 2011.

9