Sallie Mae 2011 Annual Report Download - page 180

Download and view the complete annual report

Please find page 180 of the 2011 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

|

|

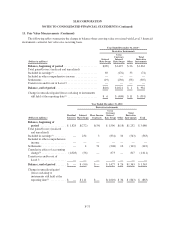

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

13. Fair Value Measurements (Continued)

amounts change based on changes in the balance of, or pool of assets or debt) hedging trust debt use

internally derived assumptions for the trust assets’ prepayment speeds and default rates to model the

notional amortization. Management makes assumptions concerning the extension features of

derivatives hedging rate-reset notes denominated in a foreign currency. These inputs are not market

observable; therefore, these derivatives are level 3 fair value estimates.

• Floor Income Contracts — Derivatives are valued using an option pricing model. Inputs to the model

include the LIBOR swap yield curve and LIBOR interest rate volatilities. The inputs are observable

inputs in active markets and these derivatives are level 2 fair value estimates.

The carrying value of borrowings designated as the hedged item in a fair value hedge are adjusted for

changes in fair value due to benchmark interest rates and foreign-currency exchange rates. These valuations are

determined through standard bond pricing models and option models (when applicable) using the stated terms of

the borrowings, and observable yield curves, foreign currency exchange rates, and volatilities.

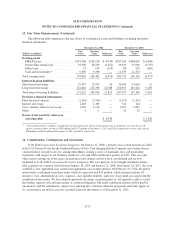

Residual Interests

Prior to the adoption of the new consolidation accounting guidance on January 1, 2010 (see “Note 2 —

Significant Accounting Policies — Consolidation), the Residual Interests were carried at fair value in the

financial statements. No active market exists for student loan Residual Interests; as such, the fair value was

calculated using discounted cash flow models and option models. Observable inputs from active markets were

used where available, including yield curves and volatilities. Significant unobservable inputs such as prepayment

speeds, default rates, certain bonds’ costs of funds and discount rates were used in determining the fair value and

required significant judgment. These unobservable inputs were internally determined based upon analysis of

historical data and expected industry trends. On a quarterly basis we back-tested our prepayment speeds, default

rates and costs of funds assumptions by comparing those assumptions to actual results experienced. We used

non-binding broker quotes and industry analyst reports which show changes in the indicative prices of the asset-

backed securities tranches immediately senior to the Residual Interest as an indication of potential changes in the

discount rate used to value the Residual Interests. Market transactions were not available to validate the models’

results.

F-71