Sallie Mae 2011 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2011 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

|

|

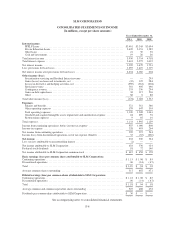

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

2. Significant Accounting Policies (Continued)

Similar to the rules governing FFELP payment requirements, our collection policies allow for periods of

nonpayment for borrowers requesting additional payment grace periods upon leaving school or experiencing

temporary difficulty meeting payment obligations. This is referred to as forbearance status and is considered

separately in our allowance for loan losses. The loss confirmation period is in alignment with our typical

collection cycle and takes into account these periods of nonpayment.

In the first quarter of 2011, we implemented a new model to estimate the Private Education Loan default

amount. Both the prior model and new model are considered “migration models”. Our prior allowance model (in

place through December 31, 2010) segmented the portfolio into categories of similar risk characteristics of which

we consider school type, credit scores, existence of a cosigner, loan status and loan seasoning as the key credit

quality indicators. Our new model uses these credit quality indicators, but incorporates a more granular

segmentation of seasoning data into the calculation. Another change in the new allowance model relates to the

historical period of experience that we use as a starting point for projecting future defaults. Our new model is

based upon a seasonal average, adjusted to the most recent three to six months of actual collection experience as

the starting point and applies expected macroeconomic changes and collection procedure changes to estimate

expected losses caused by loss events incurred as of the balance sheet date. Our previous model primarily used a

one-year historical default experience period and incorporated the estimated impact of macroeconomic factors

and collection procedure changes on a qualitative basis. Our current model places a greater emphasis on the more

recent default experience rather than the default experience for older historical periods, as we believe the recent

default experience is more indicative of the probable losses incurred in the loan portfolio today. While we

incorporated the new model in the first quarter of 2011, the overall process for calculating the appropriate

amount of allowance for Private Education Loan loss did not change. Significantly more judgment has been

required over the last several years, compared with years prior, in light of the U.S. economy and its effect on our

customers’ ability to pay their obligations. We believe that the current model more accurately reflects recent

borrower behavior, loan performance and collection performance, as well as expectations about economic

factors. There was no adjustment to our allowance for loan losses upon implementing this new default projection

model in the first quarter of 2011.

On July 1, 2011, we adopted new guidance that clarified when a loan restructuring constitutes a troubled

debt restructuring (“TDR”). In applying the new guidance we determined that certain Private Education Loans

for which we granted forbearance of greater than three months are classified as troubled debt restructurings. If a

loan meets the criteria for troubled debt accounting then an allowance for loan loss is established which

represents the present value of the losses that are expected to occur over the remaining life of the loan. This

accounting results in a higher allowance for loan losses than our previously established allowance for these loans

as our previous allowance for these loans represented an estimate of charge-offs expected to occur over the next

two years (two years being our loss confirmation period). The new accounting guidance was effective as of

July 1, 2011 but was required to be applied retrospectively to January 1, 2011. This resulted in $124 million of

additional provision for loan losses in the third quarter of 2011 from approximately $3.8 billion of student loans

being classified as troubled debt restructurings. This new accounting guidance is only applied to certain

borrowers who use their fourth or greater month of forbearance during the time period this new guidance is

effective. This new accounting guidance has the effect of accelerating the recognition of expected losses related

to our Private Education Loan portfolio. The increase in the provision for losses as a result of this new

accounting guidance does not reflect a decrease in credit expectations of the portfolio or an increase in the

expected life-of-loan losses related to this portfolio. We believe forbearance is an accepted and effective

collections and risk management tool for Private Education Loans. We plan to continue to use forbearance and as

a result, we expect to have additional loans classified as troubled debt restructurings in the future (see “Note 4 —

Allowance for Loan Losses” for a further discussion on the use of forbearance as a collection tool).

F-14