PNC Bank 2013 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2013 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

|

|

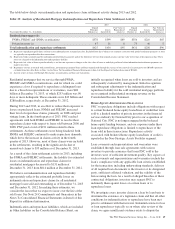

Table 40: Accruing Loans Past Due 90 Days Or More (a)(b)

Amount Percentage of Total Outstandings

Dollars in millions

December 31

2013

December 31

2012

December 31

2013

December 31

2012

Commercial $ 42 $ 42 .05% .05%

Commercial real estate 2 15 .01 .08

Equipment lease financing 2 .03

Residential real estate

Non government insured 35 46 .23 .30

Government insured 1,025 1,855 6.80 12.17

Credit card 34 36 .77 .84

Other consumer

Non government insured 14 18 .06 .08

Government insured 339 337 1.50 1.57

Total $1,491 $2,351 .76 1.26

(a) Amounts in table represent recorded investment.

(b) Pursuant to alignment with interagency supervisory guidance on practices for loans and lines of credit related to consumer lending in the first quarter of 2013, accruing consumer loans

past due 30 – 59 days decreased $44 million, accruing consumer loans past due 60 – 89 days decreased $36 million and accruing consumer loans past due 90 days or more decreased

$315 million, of which $295 million related to residential real estate government insured loans. As part of this alignment, these loans were moved into nonaccrual status.

On a regular basis our Special Asset Committee closely

monitors loans, primarily commercial loans, that are not

included in the nonperforming or accruing past due categories

and for which we are uncertain about the borrower’s ability to

comply with existing repayment terms over the next six

months. These loans totaled $.2 billion at both December 31,

2013 and December 31, 2012.

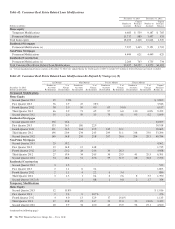

H

OME

E

QUITY

L

OAN

P

ORTFOLIO

Our home equity loan portfolio totaled $36.4 billion as of

December 31, 2013, or 19% of the total loan portfolio. Of that

total, $21.7 billion, or 60%, was outstanding under primarily

variable-rate home equity lines of credit and $14.7 billion, or

40%, consisted of closed-end home equity installment loans.

Approximately 3% of the home equity portfolio was on

nonperforming status as of December 31, 2013.

As of December 31, 2013, we are in an originated first lien

position for approximately 49% of the total portfolio and,

where originated as a second lien, we currently hold or service

the first lien position for approximately an additional 2% of

the portfolio. Historically, we have originated and sold first

lien residential real estate mortgages, which resulted in a low

percentage of home equity loans where we hold the first lien

mortgage position. The remaining 49% of the portfolio was

secured by second liens where we do not hold the first lien

position. The credit performance of the majority of the home

equity portfolio where we are in, hold or service the first lien

position, is superior to the portion of the portfolio where we

hold the second lien position but do not hold the first lien.

Lien position information is generally based upon original

LTV at the time of origination. However, after origination

PNC is not typically notified when a senior lien position that

is not held by PNC is satisfied. Therefore, information about

the current lien status of junior lien loans is less readily

available in cases where PNC does not also hold the senior

lien. Additionally, PNC is not typically notified when a junior

lien position is added after origination of a PNC first lien. This

updated information for both junior and senior liens must be

obtained from external sources, and therefore, PNC has

contracted with an industry leading third-party service

provider to obtain updated loan, lien and collateral data that is

aggregated from public and private sources.

We track borrower performance monthly, including obtaining

original LTVs, updated FICO scores at least quarterly,

updated LTVs semi-annually, and other credit metrics at least

quarterly, including the historical performance of any

mortgage loans regardless of lien position that we may or may

not hold. This information is used for internal reporting and

risk management. For internal reporting and risk management

we also segment the population into pools based on product

type (e.g., home equity loans, brokered home equity loans,

home equity lines of credit, brokered home equity lines of

credit). As part of our overall risk analysis and monitoring, we

segment the home equity portfolio based upon the

delinquency, modification status and bankruptcy status of

these loans, as well as the delinquency, modification status

and bankruptcy status of any mortgage loan with the same

borrower (regardless of whether it is a first lien senior to our

second lien).

In establishing our ALLL for non-impaired loans, we utilize a

delinquency roll-rate methodology for pools of loans. In

accordance with accounting principles, under this methodology,

we establish our allowance based upon incurred losses and not

lifetime expected losses. We also consider the incremental

expected losses when home equity lines of credit transition

from interest-only products to principal and interest products in

establishing our ALLL. The roll-rate methodology estimates

transition/roll of loan balances from one delinquency state (e.g.,

30-59 days past due) to another delinquency state (e.g., 60-89

days past due) and ultimately to charge-off. The roll through to

78 The PNC Financial Services Group, Inc. – Form 10-K