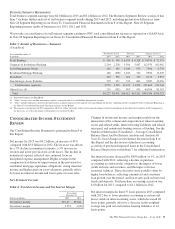

PNC Bank 2013 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2013 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

|

|

ITEM

7–M

ANAGEMENT

’

S

D

ISCUSSION AND

A

NALYSIS OF

F

INANCIAL

C

ONDITION AND

R

ESULTS OF

O

PERATIONS

(MD&A)

E

XECUTIVE

S

UMMARY

K

EY

S

TRATEGIC

G

OALS

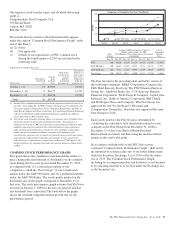

At PNC we manage our company for the long term. We are

focused on the fundamentals of growing customers, loans,

deposits and fee revenue and improving profitability, while

investing for the future and managing risk, expenses and

capital. We continue to invest in our products, markets and

brand, and embrace our corporate responsibility to the

communities where we do business.

We strive to expand and deepen customer relationships by

offering a broad range of fee-based and credit products and

services. We are focused on delivering those products and

services where, when and how our customers want to receive

them with the goal of offering insight that reflects their

specific needs. Our approach is concentrated on organically

growing and deepening client relationships that meet our risk/

return measures. Our strategies for growing fee income across

our lines of business are focused on achieving deeper market

penetration and cross selling our diverse product mix.

Our strategic priorities are designed to enhance value over the

long term. A key priority is to drive growth in acquired and

underpenetrated markets, including in the Southeast. We are

seeking to attract more of the investable assets of new and

existing clients. PNC is focused on redefining our retail banking

business to a more customer-centric and sustainable model

while lowering delivery costs as customer banking preferences

evolve. We are working to build a stronger residential mortgage

banking business with the goal of becoming the provider of

choice for our customers. Additionally, we continue to focus on

expense management while bolstering critical infrastructure and

streamlining our processes.

Our capital priorities are to support client growth and business

investment, maintain appropriate capital in light of economic

uncertainty and the Basel III framework and return excess

capital to shareholders, in accordance with our capital plan

included in our 2014 Comprehensive Capital Analysis and

Review (CCAR) submission to the Board of Governors of the

Federal Reserve System (Federal Reserve). We continue to

improve our capital levels and ratios through retention of

quarterly earnings and expect to build capital through

retention of future earnings. PNC continues to maintain

adequate liquidity positions at both PNC and PNC Bank,

National Association (PNC Bank, N.A.). For more detail, see

the Capital and Liquidity Actions portion of this Executive

Summary, the Funding and Capital Sources portion of the

Consolidated Balance Sheet Review section and the Liquidity

Risk Management section of this Item 7 and the Supervision

and Regulation section in Item 1 Business of this Report.

PNC faces a variety of risks that may impact various aspects

of our risk profile from time to time. The extent of such

impacts may vary depending on factors such as the current

economic, political and regulatory environment, merger and

acquisition activity and operational challenges. Many of these

risks and our risk management strategies are described in

more detail elsewhere in this Report.

R

ECENT

M

ARKET AND

I

NDUSTRY

D

EVELOPMENTS

There have been numerous legislative and regulatory

developments and dramatic changes in the competitive

landscape of our industry over the last several years. The

United States and other governments have undertaken major

reform of the regulation of the financial services industry,

including engaging in new efforts to impose requirements

designed to strengthen the stability of the financial system and

protect consumers and investors. We expect to face further

increased regulation of our industry as a result of current and

future initiatives intended to enhance the regulation of

financial services companies, the stability of the financial

system, the protection of consumers and investors, and the

liquidity and solvency of financial institutions and markets.

We also expect in many cases more intense scrutiny from our

supervisors in the examination process and more aggressive

enforcement of regulations on both the federal and state

levels. Compliance with new regulations will increase our

costs and reduce our revenue. Some new regulations may limit

our ability to pursue certain desirable business opportunities.

The Dodd-Frank Wall Street Reform and Consumer

Protection Act (Dodd-Frank), enacted in July 2010, mandates

the most wide-ranging overhaul of financial industry

regulation in decades. Many parts of the law are now in effect,

and others are now in the implementation stage, which is

likely to continue for several years. Dodd-Frank (through

provisions commonly known as the “Volcker Rule”) prohibits

banks and their affiliates from engaging in some types of

proprietary trading and restricts the ability of banks and their

affiliates to sponsor, invest in or have other financial

relationships with private equity, hedge and similar funds. In

December 2013, the five agencies with authority for

rulemaking issued final rules to implement the Volcker Rule.

At the same time, the Federal Reserve also issued an order

that extended, until July 21, 2015, the date by which banking

entities (including PNC) must conform their activities and

investments to the limitations and requirements of the final

rule. For additional information on the final regulations

implementing the Volcker Rule, as well as the potential

impact of them on PNC, see the Supervision and Regulation

section of Item 1 Business and Item 1A Risk Factors of this

Report.

In January 2014, the Office of the Comptroller of the

Currency (OCC) requested comment on a proposal that would

establish enforceable minimum guidelines governing the

design and implementation of an effective risk governance

framework at large national banks, including PNC Bank, N.A.

The proposal, which builds upon heightened supervisory

30 The PNC Financial Services Group, Inc. – Form 10-K