PNC Bank 2013 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2013 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

|

|

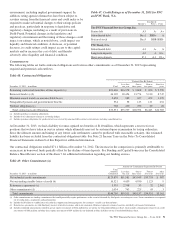

The following table summarizes the notional or contractual amounts and net fair value of financial derivatives at December 31,

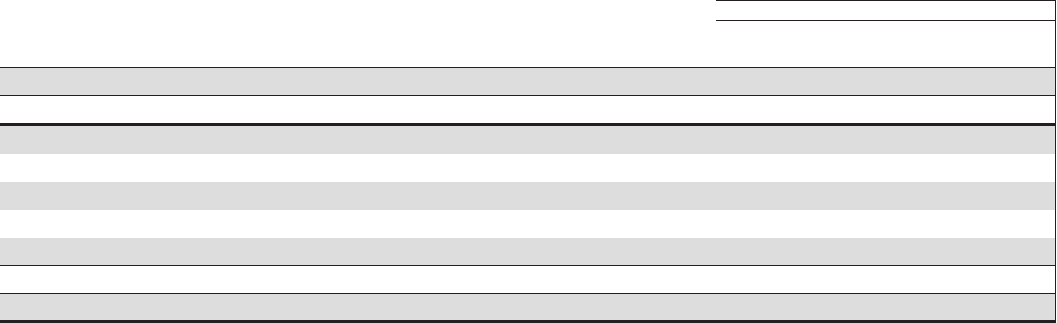

2013 and December 31, 2012.

Table 56: Financial Derivatives Summary

December 31, 2013 December 31, 2012

In millions

Notional/

Contractual

Amount

Net Fair

Value (a)

Notional/

Contractual

Amount

Net Fair

Value (a)

Derivatives designated as hedging instruments under GAAP

Total derivatives designated as hedging instruments $ 36,197 $ 825 $ 29,270 $1,720

Derivatives not designated as hedging instruments under GAAP

Total derivatives used for residential mortgage banking activities $119,679 $ 330 $166,819 $ 588

Total derivatives used for commercial mortgage banking activities 53,149 (12) 4,606 (23)

Total derivatives used for customer-related activities 169,534 138 163,848 30

Total derivatives used for other risk management activities 2,697 (422) 1,813 (357)

Total derivatives not designated as hedging instruments $345,059 $ 34 $337,086 $ 238

Total Derivatives $381,256 $ 859 $366,356 $1,958

(a) Represents the net fair value of assets and liabilities.

2012 V

ERSUS

2011

C

ONSOLIDATED

I

NCOME

S

TATEMENT

R

EVIEW

Summary Results

Net income for 2012 was $3.0 billion, or $5.30 per diluted

common share, compared with $3.1 billion, or $5.64 per

diluted common share, for 2011. Revenue growth of 8% and a

decline in the provision for credit losses were more than offset

by a 16% increase in noninterest expense in 2012 compared to

2011.

Net Interest Income

Net interest income increased to $9.6 billion in 2012

compared with $8.7 billion in 2011, primarily due to the

impact of the RBC Bank (USA) acquisition, organic loan

growth and lower funding costs.

The net interest margin remained relatively flat at 3.94% in

2012 compared with 3.92% in 2011. The modest increase in

the comparison was primarily due to a decrease in the

weighted-average rate paid on total interest-bearing liabilities,

primarily due to the runoff of maturing retail certificates of

deposit and the redemption of additional trust preferred and

hybrid capital securities during 2012, in addition to an

increase in FHLB borrowings and commercial paper as lower-

cost funding sources. This impact was mostly offset by a

decrease in the yield on total interest-earning assets, which

reflected lower rates on new loan volume and lower yields on

new securities.

Noninterest Income

Noninterest income increased to $5.9 billion in 2012

compared with $5.6 billion in 2011. The overall increase in

the comparison was primarily due to an increase in residential

mortgage loan sales revenue driven by higher loan origination

volume, gains on sales of Visa Class B common shares and

higher corporate service fees, largely offset by higher

provision for residential mortgage repurchase obligations.

Noninterest income as a percentage of total revenue was 38%

in 2012 compared with 39% in 2011.

Asset management revenue increased to $1.2 billion in 2012

compared with $1.1 billion in 2011, primarily due to higher

earnings from our BlackRock investment. Discretionary assets

under management increased to $112 billion at December 31,

2012 compared with $107 billion at December 31, 2011

driven by stronger average equity markets, positive net flows,

after adjustments to total net flows for cyclical client

activities, and strong sales performance.

Consumer services fees declined to $1.1 billion compared

with $1.2 billion in 2011. The decline reflected the regulatory

impact of lower interchange fees on debit card transactions

partially offset by customer growth. As further discussed in

the Retail Banking portion of the Business Segments Review

section of Item 7 in our 2012 Form 10-K, the Dodd-Frank

limits on interchange rates were effective October 1, 2011 and

had a negative impact on revenue of approximately $314

million in 2012 and $75 million in 2011. This impact was

partially offset by higher volumes of merchant, customer

credit card and debit card transactions and the impact of the

RBC Bank (USA) acquisition.

Corporate services revenue increased by $.3 billion, or 30%,

to $1.2 billion in 2012 compared with $.9 billion in 2011 due

to higher commercial mortgage servicing revenue and higher

merger and acquisition advisory fees in 2012. The comparison

also reflected the impact of valuation gains from rising interest

rates on commercial mortgage servicing rights valuations,

which were $31 million in 2012 compared to a loss of $152

million in 2011.

96 The PNC Financial Services Group, Inc. – Form 10-K