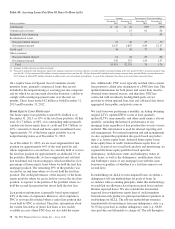

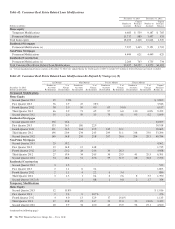

PNC Bank 2013 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2013 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

|

|

and remediating any problems with the soundness, accuracy,

improper use or operating environment of our models. We

recognize that models must be monitored over time to ensure

their continued accuracy and functioning, and our policies also

address the type and frequency of monitoring that is

appropriate according to the importance of each model.

There are a number of practices we undertake to identify and

control model risk. A primary consideration is that models be

well understood by those who use them as well as by other

parties. Our policies require detailed written model

documentation for significant models to assist in making their

use transparent and understood by users, independent

reviewers, and regulatory and auditing bodies. The

documentation must include details on the data and methods

used to develop each model, assumptions utilized within the

model, an assessment of model performance and a description

of model limitations and circumstances in which a model

should not be relied upon.

Our modeling methods and data are reviewed by independent

model reviewers not involved in the development of the model

to identify possible errors or areas where the soundness of the

model could be in question. Issues identified by the

independent reviewer are tracked and reported using our

existing governance structure until the issue has been fully

remediated.

It is important that models operate in a controlled environment

where access to code or the ability to make changes is limited

to those who are authorized. Additionally, proper back-up and

recovery mechanisms are needed for the ongoing functioning

of models. Our use of independent model control reviewers

aids in the evaluation of the existing control mechanisms to

help ensure that controls are appropriate and are functioning

properly.

L

IQUIDITY

R

ISK

M

ANAGEMENT

Liquidity risk has two fundamental components. The first is

potential loss assuming we were unable to meet our funding

requirements at a reasonable cost. The second is the potential

inability to operate our businesses because adequate contingent

liquidity is not available in a stressed environment. We manage

liquidity risk at the consolidated company level (bank, parent

company, and nonbank subsidiaries combined) to help ensure

that we can obtain cost-effective funding to meet current and

future obligations under both normal “business as usual” and

stressful circumstances, and to help ensure that we maintain an

appropriate level of contingent liquidity.

Management monitors liquidity through a series of early

warning indicators that may indicate a potential market, or

PNC-specific, liquidity stress event. In addition, management

performs a set of liquidity stress tests over multiple time

horizons with varying levels of severity and maintains a

contingency funding plan to address a potential stress event.

In the most severe liquidity stress simulation, we assume that

PNC’s liquidity position is under pressure, while the market in

general is under systemic pressure. The simulation considers,

among other things, the impact of restricted access to both

secured and unsecured external sources of funding,

accelerated run-off of customer deposits, valuation pressure

on assets and heavy demand to fund contingent obligations.

Risk limits are established within our Enterprise Capital and

Liquidity Management Policy. Management’s Asset and

Liability Committee and the Board of Directors’ Risk

Committee regularly review compliance with the established

limits.

Parent company liquidity guidelines are designed to help

ensure that sufficient liquidity is available to meet our parent

company obligations over the succeeding 24-month period.

Risk limits for parent company liquidity are established within

our Enterprise Capital and Liquidity Management Policy.

Management’s Asset and Liability Committee and the Board

of Directors’ Risk Committee regularly review compliance

with the established limits.

B

ANK

L

EVEL

L

IQUIDITY

–U

SES

Obligations requiring the use of liquidity can generally be

characterized as either contractual or discretionary. At the

bank level, primary contractual obligations include funding

loan commitments, satisfying deposit withdrawal requests and

maturities and debt service related to bank borrowings. As of

December 31, 2013, there were approximately $11.1 billion of

bank borrowings with contractual maturities of less than one

year. We also maintain adequate bank liquidity to meet future

potential loan demand and provide for other business needs, as

necessary. See the Bank Level Liquidity – Sources section

below.

On March 15, 2013 we redeemed $375 million of REIT

preferred securities issued by PNC Preferred Funding Trust III

with a current distribution rate of 8.7%.

B

ANK

L

EVEL

L

IQUIDITY

–S

OURCES

Our largest source of bank liquidity on a consolidated basis is

the deposit base that comes from our retail and commercial

businesses. Total deposits increased to $220.9 billion at

December 31, 2013 from $213.1 billion at December 31,

2012, primarily driven by growth in transactions deposits,

partially offset by lower retail certificates of deposit. Assets

determined by PNC to be liquid (liquid assets) and unused

borrowing capacity from a number of sources are also

available to maintain our liquidity position. Borrowed funds

come from a diverse mix of short and long-term funding

sources.

At December 31, 2013, our liquid assets consisted of short-

term investments (Federal funds sold, resale agreements,

trading securities and interest-earning deposits with banks)

totaling $17.2 billion and securities available for sale totaling

$48.6 billion. Of our total liquid assets of $65.8 billion, we

The PNC Financial Services Group, Inc. – Form 10-K 87