Reebok 2013 Annual Report Download - page 257

Download and view the complete annual report

Please find page 257 of the 2013 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264

|

|

adidas Group

/

2013 Annual Report

Additional Information

253

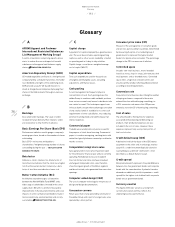

2013

Glossary

/

05.2

/

Licensed apparel

Apparel products which are produced and

marketed under a licence agreement. The adidas

Group has licence agreements with several

associations (e.g. FIFA, UEFA), leagues (e.g. NBA,

NHL), teams (e.g. Real Madrid, AC Milan) and

universities (e.g. UCLA, Notre Dame).

Licensees

Companies that have the authorisation to use the

name of a brand or business for the production and

sale of products. For example, for adidas, licensed

products include cosmetics, watches and eyewear,

for Reebok, fitness equipment.

Lien

The right to take and hold or sell the asset of a

debtor as security or payment for a debt.

Liquidity I, II, III

The liquidity ratio indicates how quickly a company

can liquidate its assets to pay for current liabilities.

Liquidity I:

[(Cash + short-term financial assets) / current

liabilities] × 100

Liquidity II:

[(Cash + short-term financial assets + accounts

receivable) / current liabilities] × 100

Liquidity III:

[(Cash + short-term financial assets + accounts

receivable + inventories) / current liabilities] × 100

/

M

Market capitalisation

Total market value of all shares outstanding.

Market capitalisation = number of shares

outstanding × current market price

Marketing working budget (MWB)

Promotion and communication spending including

sponsorship contracts with teams and individual

athletes, as well as advertising, events and other

communication activities, but excluding marketing

overhead expenses. As marketing working budget

expenses are not distribution channel specific, they

are not allocated to the adidas Group’s operating

segments.

Mature markets

Developed countries which have highly

industrialised economies, high income levels and

in which most people have a high standard of living.

For the adidas Group, mature markets are the

high-income countries of Western Europe, North

America and Japan.

Mono-branded franchise stores

Stores that are not operated or owned by the adidas

Group but by franchise partners. This concept is

used especially in the emerging markets such

as China, benefiting from local expertise of the

respective franchise partners.

/

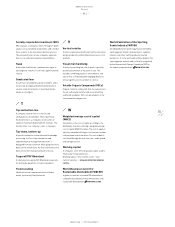

N

Natural hedges

Offset of currency risks that occurs naturally as a

result of a company’s normal operations, without

the use of derivatives. For example, revenue

received in a foreign currency and used to pay

known commitments in the same foreign currency.

Net cash/Net borrowings

Net cash is when the sum of cash and short-term

financial assets exceeds gross borrowings. Net

borrowings is the portion of gross borrowings

not covered by the sum of cash and short-term

financial assets.

Net cash/Net borrowings = cash and cash

equivalents + short-term financial assets – short-

term borrowings – long-term borrowings

Non-controlling interests

Part of net income or equity which is not

attributable to the shareholders of the reporting

company as it relates to outside ownership

interests in subsidiaries that are consolidated

with the parent company for financial reporting

purposes.

/

O

OHSAS 18000

An international occupational health and safety

management system specification.

ÖKO-Tex Standard 100

An international testing and certification system

for textiles, defining and limiting the use of certain

chemicals.

Omni-channel sales approach

Describes the ambition to achieve a globally

consistent product offer, brand communication,

availability and service across all sales channels

(Wholesale, Retail and eCommerce) and consumer

touchpoints.

Operating cash flow

Comprises operating profit, change in operating

working capital and net investments.

Operating cash flow = operating profit +/– change

in operating working capital +/– net investments

(capital expenditure less depreciation and

amortisation)

Operating lease

Method of leasing assets over periods less than

the expected lifetime of those assets. An operating

lease is accounted for by the lessee without

showing an asset or a liability on the balance sheet.

Periodic payments are accounted for by the lessee

as operating expenses for the period.

Operating overheads

Expenses which are not directly attributable to

the products or services sold, such as costs for

distribution, marketing overhead costs, logistics,

research and development, as well as general and

administrative costs, but not including costs for

promotion, advertising and communication.

Operating working capital

A company’s short-term disposable capital which

is used to finance its day-to-day business. In

comparison to working capital, operating working

capital does not include non-operational items

such as financial assets and taxes.

Operating working capital = accounts receivable

+ inventories – accounts payable

/

SEE ALSO

WORKING CAPITAL.

Option

Financial instrument which ensures the right

to purchase (call option) or to sell (put option) a

particular asset (e.g. shares or foreign exchange)

at a predetermined price (strike price) on or before

a specific date.