Reebok 2013 Annual Report Download - page 206

Download and view the complete annual report

Please find page 206 of the 2013 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

|

|

adidas Group

/

2013 Annual Report

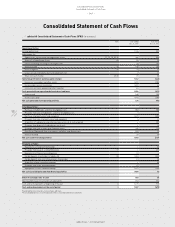

Consolidated Financial Statements

202

2013

Notes

/

04.8

/

Financial assets

All purchases and sales of financial assets are recognised on the trade date. Costs of purchases include transaction

costs. Available-for-sale financial assets include non-derivative financial assets which are not allocable under

another category of IAS 39. If their respective fair value can be measured reliably, they are subsequently carried at

fair value. If this is not the case, these are measured at amortised cost. Realised and unrealised gains and losses

arising from changes in the fair value of financial assets are included in the income statement for the period in

which they arise, except for available-for-sale financial assets where unrealised gains and losses are recognised

in equity unless they are impaired.

Borrowings and other liabilities

Borrowings and other liabilities are recognised at fair value using the “effective interest method”, net of

transaction costs incurred. In subsequent periods, long-term borrowings are stated at amortised cost using the

“effective interest method”. Any difference between proceeds (net of transaction costs) and the redemption value

is recognised in the income statement over the term of the borrowing.

In 2012, adidas AG issued a convertible bond which grants the holder the right to convert the bond into

adidas AG shares. The number of underlying shares is fixed and does not vary subject to the fair value of the

shares.

Compound financial instruments (e.g. convertible bonds) are divided into a liability component shown under

borrowings and into an equity component resulting from conversion rights. The equity component is included

in the capital reserve. The fair value of the liability component is determined by discounting the interest and

principal payments of a comparable liability without conversion rights, applying risk-adjusted interest rates. The

liability component is subsequently measured at amortised cost using the “effective interest method”. The equity

component is determined as the difference between the fair value of the total compound financial instrument and

the fair value of the liability component and is reported within equity. There is no subsequent measurement of

the equity component. At initial recognition, directly attributable transaction costs are assigned to the equity and

liability component pro rata on the basis of the respective carrying amounts.

Other provisions and accrued liabilities

Other provisions are recognised where a present obligation (legal or constructive) to third parties has been

incurred as a result of a past event which can be estimated reliably and is likely to lead to an outflow of resources,

and where the timing or amount is uncertain. Other non-current provisions are discounted if the effect of

discounting is material.

Accrued liabilities are liabilities to pay for goods or services that have been received or supplied but have not

been paid, invoiced or formally agreed with the supplier, including amounts due to employees. Here, however, the

timing and amount of an outflow of resources is not uncertain.

Pensions and similar obligations

Provisions and expenses for pensions and similar obligations relate to the Group’s obligations for defined benefit

and defined contribution plans. The obligations under defined benefit plans are determined separately for each

plan by valuing the employee benefits accrued in return for their service during the current and prior periods.

These benefit accruals are discounted to calculate their present value, and the fair value of any plan assets is

deducted in order to determine the net liability. The discount rate is set on the basis of yields of high-quality

corporate bonds at the balance sheet date provided there is a deep market for high-quality corporate bonds

in a given currency. Otherwise, government bond yields are used as a reference. Calculations are performed

by qualified actuaries using the “projected unit credit method” in accordance with IAS 19 “Employee Benefits”.

Obligations for contributions to defined contribution plans are recognised as an expense in the income statement

as incurred.