Reebok 2013 Annual Report Download - page 168

Download and view the complete annual report

Please find page 168 of the 2013 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

|

|

adidas Group

/

2013 Annual Report

Group Management Report – Financial Review

164

2013

/

03.5

/

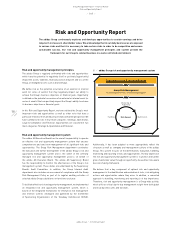

Risk and Opportunity Report

/

Strategic Risks

Risks related to distribution strategy

The inability to appropriately influence in which channels the Group’s

products are sold constitutes a continuous risk. Grey market activity,

parallel imports or the distribution of our products on open online

marketplaces could negatively affect our own sales performance and

the image of our Group’s brands. In a few individual markets, we work

with distributors or strategic partners whose approach might differ from

our own distribution practices and standards. This could also negatively

impact the adidas Group’s business performance. Furthermore, weakly

defined segmentation and channel strategies could lead to an unhealthy

utilisation of our multiple distribution channels as well as strong

retaliation from our customers. As a result, the Group has developed

and implemented clearly defined distribution policies and procedures to

avoid over-distribution of products in a particular channel and limit the

exposure to unwanted channels such as grey markets or open online

marketplaces. In addition, we conduct specific trainings for our sales

force to appropriately manage product distribution and ensure that the

right product is sold at the right point of sale to the right consumer at an

adequate price

/

SEE GLOBAL SALES STRATEGY, P. 72.

Nevertheless, we still believe that unbalanced product distribution and

the inability to effectively manage our different sales channels could

have a significant impact on the Group. As a result of the dynamic market

environment and the fast-changing world of online sales, we continue to

evaluate the likelihood of materialising as possible.

Dependency risks

Risks arise from a dependence on particular suppliers, customers,

other business partners, products or even markets. An over-reliance

on a supplier for a substantial portion of the Group’s product volume,

or an over-dependence on a particular customer, increases the Group’s

vulnerability to delivery and sales shortfalls and could lead to significant

margin pressure. Similarly, a strong dependence on certain products or

markets could make the Group very susceptible to swings in consumer

demand or changes in the market environment.

To mitigate these risks, the Group works with a broad network of

suppliers and for the vast majority of its products does not have a single-

sourcing model. Likewise, we utilise a broad distribution strategy which

includes further expanding our controlled space activities. This enables

us to reduce negative consequences resulting from sales shortfalls

that can occur with key customers. Specifically, no single customer

of our Group accounted for more than 10% of Group sales in 2013.

Furthermore, we consistently provide a well-balanced product portfolio

with no particular model or article contributing more than 1% to Group

sales, which enables us to minimise negative effects from sudden

unexpected changes in consumer demand.

Despite our global diversification, which reduces reliance on a particular

market as far as possible, we still remain vulnerable to negative

developments in key sales markets such as Russia/CIS, China or North

America as well as our important sourcing countries. Therefore, we

continue to regard the potential impact of these risks as significant.

Due to our strong relationships with suppliers and customers as well as

our positive expectations for our key sales markets we now assess the

likelihood of materialising as unlikely (2012: possible).

Risks related to media and stakeholder activities

The adidas Group faces considerable risk if we are unable to uphold

high levels of consumer awareness, affiliation and purchase intent

for our brands. Adverse media coverage on our products or business

practices, unfavourable stakeholder initiatives as well as negative social

media discussion may significantly hurt the Group’s reputation and

brand image and eventually lead to a sales slowdown. To mitigate these

risks, we pursue proactive, open communication with key stakeholders

(e.g. consumers, media, non-governmental organisations, the financial

community, etc.) on a continuous basis. We have also defined clear

mission statements, values and goals for all our brands

/

SEE GLOBAL

BRANDS STRATEGY, P. 77

/

SEE OTHER BUSINESSES STRATEGY, P. 86. These

form the foundation of our product and brand communication strategies.

Furthermore, we continue to invest significant marketing resources to

build brand equity and foster consumer awareness.

Nevertheless, we continue to believe that unsubstantiated negative

media coverage, uncontrolled social media activities and stakeholder

activism could have a significant impact on our Group. Despite the

fast-moving and hardly controllable nature of social media as well as

ever-increasing media and other stakeholder activities worldwide, we

still regard the likelihood of being affected to such an extent as likely.

Customer consolidation and cross-border expansion/

private label risks

The adidas Group is exposed to risks from consolidation amongst

retailers as well as the increase of retailers’ own private label

businesses. In addition, several key accounts, particularly in Europe,

continue to expand internationally while centralising their purchasing

activities. As a result, we may experience a reduction of our bargaining

power, reduced shelf space allocation from retailers and lower sales and

margin due to price arbitrage.