Reebok 2013 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2013 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

|

|

adidas Group

/

2013 Annual Report

Group Management Report – Financial Review

119

2013

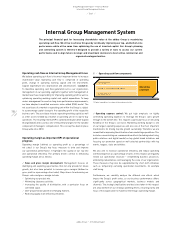

Internal Group Management System

/

03.1

/

Optimisation of non-operating components

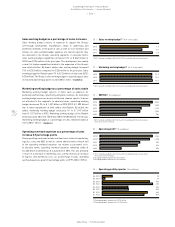

Our Group also puts a high priority on the optimisation of non-operating

components such as financial result and taxes, as these items strongly

impact the Group’s cash outflows and therefore the Group’s free cash

flow. Financial expenses are managed centrally by our Group Treasury

department

/

SEE TREASURY, P. 135. The Group’s current and future tax

expenditure is optimised globally by our Group Taxes department.

Tight operating working capital management

Due to a comparatively low level of fixed assets required in our business,

the efficiency of the Group’s balance sheet depends to a large degree

on our operating working capital management. Our key metric is

operating working capital as a percentage of net sales. Monitoring

the development of this key metric facilitates the measurement of our

progress in improving the efficiency of our business cycle. We have

significantly enhanced operating working capital management over

recent years through improvement of the Group’s inventories, accounts

receivable and accounts payable.

We strive to proactively manage our inventory levels to meet market

demand and ensure fast replenishment. Inventory ageing is controlled

tightly to reduce inventory obsolescence and to minimise clearance

activities. As a result, stock turn development is the key performance

indicator as it measures the number of times average inventory is sold

during a year, highlighting the efficiency of capital locked up in products.

To optimise capital tied up in accounts receivable, we strive to improve

collection efforts in order to reduce the Days of Sales Outstanding (DSO)

and improve the ageing of accounts receivable. Likewise, we strive to

optimise payment terms with our suppliers to best manage our accounts

payable.

Capital expenditure targeted to maximise future returns

Improving the effectiveness of the Group’s capital expenditure is

another lever to maximise our operating cash flow. We control capital

expenditure with a top-down, bottom-up approach. In a first step,

Group management defines focus areas and an overall investment

budget based on investment requests from various functions of the

organisation. Our operating units then align their initiatives within the

scope of assigned priorities and available budget. We evaluate potential

return on planned investments utilising the net present value method.

Risk is accounted for, adding a risk premium to the cost of capital and

thus reducing our estimated future earnings streams where appropriate.

By means of scenario planning, the sensitivity of investment returns is

tested against changes in initial assumptions. For large investment

projects, timelines and deviations versus budget are monitored on a

monthly basis throughout the course of the project.

The final step of optimising return on investments is our selective

post-mortem reviews, where larger projects in particular are evaluated

and learnings are documented to be available for future capital

expenditure decisions.

M&A activities focus on long-term value

creation potential

We see the vast majority of the Group’s future growth opportunities

coming from our existing portfolio of brands. However, as part of our

commitment to ensuring sustainable profitable development, we

regularly review merger and acquisition (M&A) options that may provide

additional commercial and operational opportunities. Acquisitive growth

focus is primarily related to improving the Group’s positioning within

a certain sports category, strengthening our technology portfolio or

addressing new consumer segments.

Any potential acquisition candidate must correspond with the Group’s

strategic direction. Maximising return on invested capital above the cost

of capital in the long term is a core consideration in our decision-making

process. Of particular importance is evaluating the potential impact

on our Group’s free cash flow. We assess current and future projected

key financial metrics to evaluate a target’s operating profit potential. In

addition, careful consideration is given to potential financing needs and

their impact on the Group’s financial leverage.

Cost of capital metric used to measure

investment potential

Creating value for our shareholders by earning a return on invested

capital above the cost of that capital is a guiding principle of our Group

strategy. We source capital from equity and debt markets. Therefore, we

have a responsibility that our return on capital meets the expectations of

both equity shareholders and creditors. We calculate the cost of capital

utilising the weighted average cost of capital (WACC) formula. This

metric allows us to calculate the minimum required financial returns

of planned capital investments. The cost of equity is computed utilising

the risk-free rate, market risk premium and beta factor. Cost of debt is

calculated using the risk-free rate, credit spread and average tax rate.