MetLife 2007 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2007 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

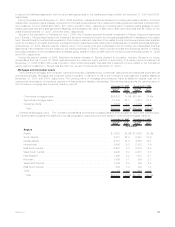

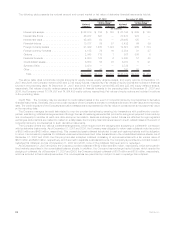

The table below illustrates the potential loss in fair value of the Company’s interest rate sensitive financial instruments at December 31,

2007. In addition, the potential loss with respect to the fair value of currency exchange rates and the Company’s equity price sensitive

positions at December 31, 2007 is set forth in the table below.

The potential loss in fair value for each market risk exposure of the Company’s portfolio at December 31, 2007 was:

December 31, 2007

(In millions)

Non-trading:

Interestraterisk....................................................... $5,170

Equitypricerisk....................................................... $ 96

Foreigncurrencyexchangeraterisk.......................................... $ 711

Trading:

Interestraterisk....................................................... $ 18

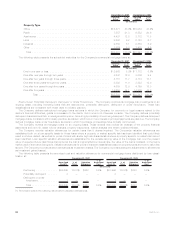

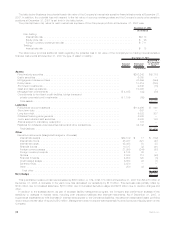

The table below provides additional detail regarding the potential loss in fair value of the Company’s non-trading interest sensitive

financial instruments at December 31, 2007 by type of asset or liability:

Notional

Amount Estimated

Fair Value

Assuming a

10% increase

in the yield

curve

December 31, 2007

(In millions)

Assets

Fixedmaturitysecurities............................................... $242,242 $(5,177)

Equitysecurities .................................................... 6,050 —

Mortgageandconsumerloans........................................... 47,599 (594)

Policyloans....................................................... 10,419 (235)

Short-terminvestments................................................ 2,648 (15)

Cashandcashequivalents ............................................. 10,368 —

Mortgageloancommitments ............................................ $ 4,035 (43) (50)

Commitments to fund bank credit facilities, bridge loans and

privatecorporatebondinvestments ...................................... $ 1,196 (59) —

Totalassets...................................................... $(6,071)

Liabilities

Policyholderaccountbalances........................................... $114,466 $ 840

Short-termdebt .................................................... 667 —

Long-termdebt..................................................... 9,532 307

Collateralfinancingarrangements......................................... 5,365 —

Juniorsubordinateddebtsecurities........................................ 4,338 136

Sharessubjecttomandatoryredemption .................................... 178 —

Payablesforcollateralundersecuritiesloanedandothertransactions.................. 44,136 —

Totalliabilities .................................................... $1,283

Other

Derivative instruments (designated hedges or otherwise)

Interestrateswaps................................................. $62,519 $ 17 $ (132)

Interestratefloors.................................................. 48,937 621 (47)

Interestratecaps.................................................. 45,498 50 33

Financialfutures................................................... 10,817 32 (41)

Foreigncurrencyswaps.............................................. 21,399 (244) (97)

Foreigncurrencyforwards ............................................ 4,185 60 —

Options ........................................................ 2,043 712 (93)

Financialforwards.................................................. 4,600 120 (5)

Creditdefaultswaps................................................ 6,850 23 (1)

SyntheticGICs.................................................... 3,670 — —

Other.......................................................... 250 43 1

Totalother ..................................................... $ (382)

Net change ........................................................ $(5,170)

This quantitative measure of risk has decreased by $805 million, or 13%, to $5,170 million at December 31, 2007 from $5,975 million at

December 31, 2006. A decrease in the yield curve has decreased our sensitivity by $1.5 billion. This decrease was partially offset by

$140 million due to increased asset size, $270 million due to increased derivative usage and $285 million due to duration charges and

other.

In addition to the analysis above, as part of its asset liability management program, the Company also performs an analysis of the

sensitivity to changes in interest rates, including both insurance liabilities and financial instruments. As of December 31, 2007, a

hypothetical instantaneous 10% decrease in interest rates applied to the Company’s liabilities, insurance and associated asset portfolios

would reduce the fair value of equity by $12 million. Management does not expect that this sensitivity would produce a liquidity strain on the

Company.

88 MetLife, Inc.