MetLife 2007 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2007 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

In addition to reinsuring mortality risk as described previously, the Company reinsures other risks, as well as specific coverages. The

Company routinely reinsures certain classes of risks in order to limit its exposure to particular travel, avocation and lifestyle hazards. The

Company has exposure to catastrophes, which could contribute to significant fluctuations in the Company’s results of operations. The

Company uses excess of retention and quota share reinsurance arrangements to provide greater diversification of risk and minimize

exposure to larger risks.

The Company had also protected itself through the purchase of combination risk coverage. This reinsurance coverage pooled risks

from several lines of business and included individual and group life claims in excess of $2 million per policy, as well as excess property and

casualty losses, among others. This combination risk coverage was commuted during 2005.

The Company reinsures its business through a diversified group of reinsurers. No single unaffiliated reinsurer has a material obligation to

the Company nor is the Company’s business substantially dependent upon any reinsurance contracts. The Company is contingently liable

with respect to ceded reinsurance should any reinsurer be unable to meet its obligations under these agreements.

In the Reinsurance Segment, Reinsurance Group of America, Incorporated (“RGA”) retains a maximum of $6 million of coverage per

individual life with respect to its assumed reinsurance business.

The amounts in the consolidated statements of income are presented net of reinsurance ceded. Information regarding the effect of

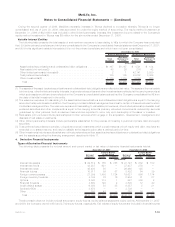

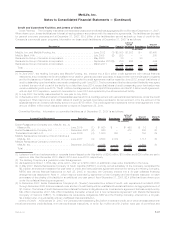

reinsurance is as follows:

2007 2006 2005

Years Ended December 31,

(In millions)

Directpremiums................................................... $24,168 $23,324 $22,232

Reinsuranceassumed ............................................... 6,181 5,294 4,646

Reinsuranceceded................................................. (2,454) (2,206) (2,018)

Netpremiums..................................................... $27,895 $26,412 $24,860

Reinsurance recoverables netted against policyholder benefits and claims . . . . . . . . . . . . . $ 2,622 $ 2,313 $ 2,400

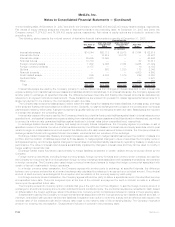

Reinsurance recoverables, included in premiums and other receivables, were $10.4 billion and $10.2 billion at December 31, 2007 and

2006, respectively, including $1.2 billion at both December 31, 2007 and 2006 relating to reinsurance of long-term GICs and structured

settlement lump sum contracts accounted for as a financing transaction; $3.4 billion and $3.0 billion at December 31, 2007 and 2006,

respectively, relating to reinsurance on the run-off of long-term care business written by Travelers; $1.2 billion and $1.3 billion at

December 31, 2007 and 2006, respectively, relating to reinsurance on the run-off of workers compensation business written by Travelers;

and $1.1 billion and $1.4 billion at December 31, 2007 and 2006, respectively, relating to the reinsurance of investment-type contracts

held by small market defined benefit contribution plans. Reinsurance and ceded commissions payables, included in other liabilities, were

$571 million and $275 million at December 31, 2007 and 2006, respectively.

9. Closed Block

On April 7, 2000, (the “Demutualization Date”), MLIC converted from a mutual life insurance company to a stock life insurance company

and became a wholly-owned subsidiary of MetLife, Inc. The conversion was pursuant to an order by the New York Superintendent of

Insurance(the“Superintendent”)approvingMLIC’splanofreorganization,asamended(the“Plan”).OntheDemutualizationDate,MLIC

established a closed block for the benefit of holders of certain individual life insurance policies of MLIC. Assets have been allocated to the

closed block in an amount that has been determined to produce cash flows which, together with anticipated revenues from the policies

included in the closed block, are reasonably expected to be sufficient to support obligations and liabilities relating to these policies,

including, but not limited to, provisions for the payment of claims and certain expenses and taxes, and to provide for the continuation of

policyholder dividend scales in effect for 1999, if the experience underlying such dividend scales continues, and for appropriate

adjustments in such scales if the experience changes. At least annually, the Company compares actual and projected experience

against the experience assumed in the then-current dividend scales. Dividend scales are adjusted periodically to give effect to changes in

experience.

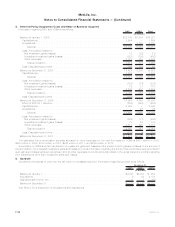

The closed block assets, the cash flows generated by the closed block assets and the anticipated revenues from the policies in the

closed block will benefit only the holders of the policies in the closed block. To the extent that, over time, cash flows from the assets

allocated to the closed block and claims and other experience related to the closed block are, in the aggregate, more or less favorable than

what was assumed when the closed block was established, total dividends paid to closed block policyholders in the future may be greater

than or less than the total dividends that would have been paid to these policyholders if the policyholder dividend scales in effect for 1999

had been continued. Any cash flows in excess of amounts assumed will be available for distribution over time to closed block policyholders

and will not be available to stockholders. If the closed block has insufficient funds to make guaranteed policy benefit payments, such

payments will be made from assets outside of the closed block. The closed block will continue in effect as long as any policy in the closed

block remains in-force. The expected life of the closed block is over 100 years.

The Company uses the same accounting principles to account for the participating policies included in the closed block as it used prior

to the Demutualization Date. However, the Company establishes a policyholder dividend obligation for earnings that will be paid to

policyholders as additional dividends as described below. The excess of closed block liabilities over closed block assets at the effective

date of the demutualization (adjusted to eliminate the impact of related amounts in accumulated other comprehensive income) represents

the estimated maximum future earnings from the closed block expected to result from operations attributed to the closed block after

income taxes. Earnings of the closed block are recognized in income over the period the policies and contracts in the closed block remain

in-force. Management believes that over time the actual cumulative earnings of the closed block will approximately equal the expected

cumulative earnings due to the effect of dividend changes. If, over the period the closed block remains in existence, the actual cumulative

F-43MetLife, Inc.

MetLife, Inc.

Notes to Consolidated Financial Statements — (Continued)