MetLife 2007 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2007 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

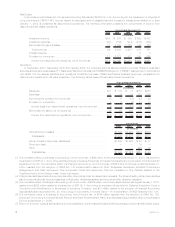

consolidate such investments. The accounting rules for the determination of the primary beneficiary are complex and require evaluation of

the contractual rights and obligations associated with each party involved in the entity, an estimate of the entity’s expected losses and

expected residual returns and the allocation of such estimates to each party.

The use of different methodologies and assumptions as to the determination of the fair value of investments, the timing and amount of

impairments, the recognition of income, or consolidation of investments may have a material effect on the amounts presented within the

consolidated financial statements.

Derivative Financial Instruments

The Company enters into freestanding derivative transactions including swaps, forwards, futures and option contracts. The Company

uses derivatives primarily to manage various risks. The risks being managed are variability in cash flows or changes in fair values related to

financial instruments and currency exposure associated with net investments in certain foreign operations. To a lesser extent, the Company

uses credit derivatives, such as credit default swaps, to synthetically replicate investment risks and returns which are not readily available

in the cash market. The Company also purchases certain securities, issues certain insurance policies and engages in certain reinsurance

contracts that have embedded derivatives.

Fair value of derivatives is determined by quoted market prices or through the use of pricing models. The determination of fair value,

when quoted market values are not available, is based on valuation methodologies and assumptions deemed appropriate under the

circumstances. Derivative valuations can be affected by changes in interest rates, foreign currency exchange rates, financial indices, credit

spreads, market volatility, and liquidity. Values can also be affected by changes in estimates and assumptions used in pricing models. Such

assumptions include estimates of volatility, interest rates, foreign currency exchange rates, other financial indices and credit ratings.

Essential to the analysis of the fair value is risk of counterparty default. The use of different assumptions may have a material effect on the

estimated derivative fair value amounts, as well as the amount of reported net income. Also, fluctuations in the fair value of derivatives

which have not been designated for hedge accounting may result in significant volatility in net income.

The accounting for derivatives is complex and interpretations of theprimaryaccountingstandardscontinuetoevolveinpractice.

Judgment is applied in determining the availability and application of hedge accounting designations and the appropriate accounting

treatment under these accounting standards. If it was determined that hedge accounting designations were not appropriately applied,

reported net income could be materially affected. Differences in judgment as to the availability and application of hedge accounting

designations and the appropriate accounting treatment may result in a differing impact on the consolidated financial statements of the

Company from that previously reported. Measurements of ineffectiveness of hedging relationships are also subject to interpretations and

estimations and different interpretations or estimates may have a material effect on the amount reported in net income.

Additionally, there is a risk that embedded derivatives requiring bifurcation may not be identified and reported at fair value in the

consolidated financial statements and that their related changes in fair value could materially affect reported net income.

Deferred Policy Acquisition Costs and Value of Business Acquired

The Company incurs significant costs in connection with acquiring new and renewal insurance business. Costs that vary with and relate

to the production of new business are deferred as DAC. Such costs consist principally of commissions and agency and policy issue

expenses. VOBA is an intangible asset that reflects the estimated fair value of in-force contracts in a life insurance company acquisition and

represents the portion of the purchase price that is allocated to the value of the right to receive future cash flows from the business in-force

at the acquisition date. VOBA is based on actuarially determined projections, by each block of business, of future policy and contract

charges, premiums, mortality and morbidity, separate account performance, surrenders, operating expenses, investment returns and other

factors. Actual experience on the purchased business may vary from these projections. The recovery of DAC and VOBA is dependent upon

the future profitability of the related business. DAC and VOBA are aggregated in the financial statements for reporting purposes.

DAC for property and casualty insurance contracts, which is primarily composed of commissions and certain underwriting expenses, is

amortized on a pro rata basis over the applicable contract term or reinsurance treaty.

DAC and VOBA on life insurance or investment-type contracts are amortized in proportion to gross premiums, gross margins or gross

profits, depending on the type of contract as described below.

The Company amortizes DAC and VOBA related to non-participating and non-dividend-paying traditional contracts (term insurance,

non-participating whole life insurance, non-medical health insurance, and traditional group life insurance) over the entire premium paying

period in proportion to the present value of actual historic and expected future gross premiums. The present value of expected premiums is

based upon the premium requirement of each policy and assumptions for mortality, morbidity, persistency, and investment returns at policy

issuance, or policy acquisition, as it relates to VOBA, that include provisions for adverse deviation and are consistent with the assumptions

used to calculate future policyholder benefit liabilities. These assumptions are not revised after policy issuance or acquisition unless the

DAC or VOBA balance is deemed to be unrecoverable from future expected profits. Absent a premium deficiency, variability in amortization

after policy issuance or acquisition is caused only by variability in premium volumes.

The Company amortizes DAC and VOBA related to participating, dividend-paying traditional contracts over the estimated lives of the

contracts in proportion to actual and expected future gross margins. The amortization includes interest based on rates in effect at inception

or acquisition of the contracts. The future gross margins are dependent principally on investment returns, policyholder dividend scales,

mortality, persistency, expenses to administer the business, creditworthiness of reinsurance counterparties, and certain economic

variables, such as inflation. For participating contracts (dividend paying traditional contracts within the closed block) future gross margins

are also dependent upon changes in the policyholder dividend obligation. Of these factors, the Company anticipates that investment

returns, expenses, persistency, and other factor changes and policyholder dividend scales are reasonably likely to impact significantly the

rate of DAC and VOBA amortization. Each reporting period, the Company updates the estimated gross margins with the actual gross

margins for that period. When the actual gross margins change from previously estimated gross margins, the cumulative DAC and VOBA

amortization is re-estimated and adjusted by a cumulative charge or credit to current operations. When actual gross margins exceed those

previously estimated, the DAC and VOBA amortization will increase, resulting in a current period charge to earnings. The opposite result

occurs when the actual gross margins are below the previously estimated gross margins. Each reporting period, the Company also

updates the actual amount of business in-force, which impacts expected future gross margins.

The Company amortizes DAC and VOBA related to fixed and variable universal life contracts and fixed and variable deferred annuity

contracts over the estimated lives of the contracts in proportion to actual and expected future gross profits. The amortization includes

10 MetLife, Inc.