MetLife 2007 Annual Report Download - page 12

Download and view the complete annual report

Please find page 12 of the 2007 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

As expectations for global economic growth are lowered, factors such as consumer spending, business investment, government

spending, the volatility and strength of the capital markets, and inflation all affect the business and economic environment and, ultimately,

the amount and profitability of the business we conduct. In an economic downturn characterized by higher unemployment, lower family

income, lower corporate earnings, lower business investment and lower consumer spending, the demand for financial and insurance

products could be adversely affected. Adverse changes in the economy could affect earnings negatively and have a material adverse effect

on our business, results of operations and financial condition.

Demographics. In the coming decade, a key driver shaping the actions of the life insurance industry will be the rising income

protection, wealth accumulation and needs of the retiring Baby Boomers. As a result of increasing longevity, retirees will need to

accumulate sufficient savings to finance retirements that may span 30 or more years. Helping the Baby Boomers to accumulate assets for

retirement and subsequently to convert these assets into retirement income represents an opportunity for the life insurance industry.

Life insurers are well positioned to address the Baby Boomers’ rapidly increasing need for savings tools and for income protection. The

Company believes that, among life insurers, those with strong brands, high financial strength ratings and broad distribution, are best

positioned to capitalize on the opportunity to offer income protection products to Baby Boomers.

Moreover, the life insurance industry’s products and the needs they are designed to address are complex. The Company believes that

individuals approaching retirement age will need to seek information to plan for and manage their retirements and that, in the workplace, as

employees take greater responsibility for their benefit options and retirement planning, they will need information about their possible

individual needs. One of the challenges for the life insurance industry will be the delivery of this information in a cost effective manner.

Competitive Pressures. The life insurance industry remains highly competitive. The product development and product life-cycles have

shortened in many product segments, leading to more intense competition with respect to product features. Larger companies have the

ability to invest in brand equity, product development, technology and risk management, which are among the fundamentals for sustained

profitable growth in the life insurance industry. In addition, several of the industry’s products can be quite homogeneous and subject to

intense price competition. Sufficient scale, financial strength and financial flexibility are becoming prerequisites for sustainable growth in

the life insurance industry. Larger market participants tend to have the capacity to invest in additional distribution capability and the

information technology needed to offer the superior customer service demanded by an increasingly sophisticated industry client base.

Regulatory Changes. The life insurance industry is regulated at the state level, with some products and services also subject to federal

regulation. As life insurers introduce new and often more complex products, regulators refine capital requirements and introduce new

reserving standards for the life insurance industry. Regulations recently adopted or currently under review can potentially impact the

reserve and capital requirements of the industry. In addition, regulators have undertaken market and sales practices reviews of several

markets or products, including equity-indexed annuities, variable annuities and group products.

Pension Plans. On August 17, 2006, President Bush signed the Pension Protection Act of 2006 (“PPA”) into law. The PPA is

considered to be the most sweeping pension legislation since the adoption of the Employee Retirement Income Security Act of 1974

(“ERISA”) on September 2, 1974. The provisions of the PPA may, over time, have a significant impact on demand for pension, retirement

savings, and lifestyle protection products in both the institutional and retail markets. The impact of the legislation may have a positive effect

on the life insurance and financial services industries in the future.

Impact of Hurricanes

On August 29, 2005, Hurricane Katrina made landfall in the states of Louisiana, Mississippi and Alabama, causing catastrophic damage

to these coastal regions. MetLife’s cumulative gross losses from Hurricane Katrina were $314 million, $333 million and $335 million at

December 31, 2007, 2006 and 2005, respectively, primarily arising from the Company’s homeowners business. During the years ended

December 31, 2007, 2006 and 2005, the Company recognized net losses, net of income tax and reinsurance recoverables and including

reinstatement premiums and other reinsurance-related premium adjustments related to the catastrophe, of ($13) million, ($2) million and

$134 million, respectively.

On October 24, 2005, Hurricane Wilma made landfall across the state of Florida. MetLife’s cumulative gross losses from Hurricane

Wilma were $66 million, $64 million and $57 million at December 31, 2007, 2006 and 2005, respectively, primarily arising from the

Company’s homeowners and automobile businesses. During the years ended December 31, 2006 and 2005, the Company’s Auto & Home

segment recognized net losses, net of income tax and reinsurance recoverables, of ($3) million and $32 million, respectively, related to

Hurricane Wilma. The Company did not recognize any loss during the year ended December 31, 2007, related to Hurricane Wilma.

Additional hurricane-related losses may be recorded in future periods as claims are received from insureds and claims to reinsurers are

processed. Reinsurance recoveries are dependent upon the continued creditworthiness of the reinsurers, which may be affected by their

other reinsured losses in connection with Hurricanes Katrina and Wilma and otherwise. In addition, lawsuits, including purported class

actions, have been filed in Louisiana and Mississippi challenging denial of claims for damages caused to property during Hurricane Katrina.

Metropolitan Property and Casualty Insurance Company is a named party in some of these lawsuits. In addition, rulings in cases in which

Metropolitan Property and Casualty Insurance Company is not a party may affect interpretation of its policies. Metropolitan Property and

Casualty Insurance Company intends to vigorously defend these matters. However, any adverse rulings could result in an increase in the

Company’s hurricane-related claim exposure and losses. Based on information known by management, it does not believe that additional

claim losses resulting from Hurricane Katrina will have a material adverse impact on the Company’s consolidated financial statements.

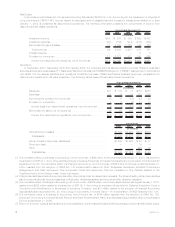

Summary of Critical Accounting Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America

(“GAAP”) requires management to adopt accounting policies and make estimates and assumptions that affect amounts reported in the

consolidated financial statements. The most critical estimates include those used in determining:

i) the fair value of investments in the absence of quoted market values;

ii) investment impairments;

iii) the recognition of income on certain investments;

8MetLife, Inc.