MetLife 2007 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2007 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

interest based on rates in effect at inception or acquisition of the contracts. The amount of future gross profits is dependent principally

upon returns in excess of the amounts credited to policyholders, mortality, persistency, interest crediting rates, expenses to administer the

business, creditworthiness of reinsurance counterparties, the effect of any hedges used, and certain economic variables, such as inflation.

Of these factors, the Company anticipates that investment returns, expenses, and persistency are reasonably likely to impact significantly

the rate of DAC and VOBA amortization. Each reporting period, the Company updates the estimated gross profits with the actual gross

profits for that period. When the actual gross profits change from previously estimated gross profits, the cumulative DAC and VOBA

amortization is re-estimated and adjusted by a cumulative charge or credit to current operations. When actual gross profits exceed those

previously estimated, the DAC and VOBA amortization will increase, resulting in a current period charge to earnings. The opposite result

occurs when the actual gross profits are below the previously estimated gross profits. Each reporting period, the Company also updates

the actual amount of business remaining in-force, which impacts expected future gross profits.

Separate account rates of return on variable universal life contracts and variable deferred annuity contracts affect in-force account

balances on such contracts each reporting period. Returns that are higher than the Company’s long-term expectation produce higher

account balances, which increases the Company’s future fee expectations and decreases future benefit payment expectations on

minimum death benefit guarantees, resulting in higher expected future gross profits. The opposite result occurs when returns are lower

than the Company’s long-term expectation. The Company’s practice to determine the impact of gross profits resulting from returns on

separate accounts assumes that long-term appreciation in equity markets is not changed by short-term market fluctuations, but is only

changed when sustained interim deviations are expected. The Company monitors these changes and only changes the assumption when

its long-term expectation changes. The effect of an increase/(decrease) by 100 basis points in the assumed future rate of return is

reasonably likely to result in a decrease/(increase) in the DAC and VOBA balances of approximately $95 million with an offset to the

Company’s unearned revenue liability of approximately $20 million for this factor.

The Company also reviews periodically other long-term assumptions underlying the projections of estimated gross margins and profits.

These include investment returns, policyholder dividend scales, interest crediting rates, mortality, persistency, and expenses to administer

business. Management annually updates assumptions used in the calculation of estimated gross margins and profits which may have

significantly changed. If the update of assumptions causes expected future gross margins and profits to increase, DAC and VOBA

amortization will decrease, resulting in a current period increase to earnings. The opposite result occurs when the assumption update

causes expected future gross margins and profits to decrease.

Over the past two years, the Company’s most significant assumption updates resulting in a change to expected future gross margins

and profits and the amortization of DAC and VOBA have been updated due to revisions to expected future investment returns, expenses,

in-force or persistency assumptions and policyholder dividends on contracts included within the Individual segment. The Company

expects these assumptions to be the ones most reasonably likely to cause significant changes in the future. Changes in these assumptions

can be offsetting and the Company is unable to predict their movement or offsetting impact over time.

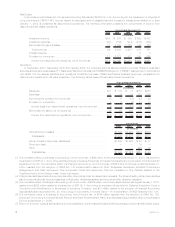

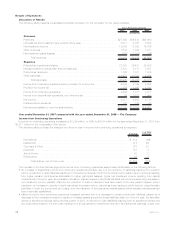

The following chart illustrates the effect on DAC and VOBA within the Company’s Individual segment of changing each of the respective

assumptions during the years ended December 31, 2007 and 2006:

2007 2006

Years Ended

December 31,

(In millions)

Investmentreturn ....................................................... $100 $192

Expense ............................................................. (53) 45

In-force/Persistency...................................................... 17 (7)

Policyholderdividendsandother.............................................. (55) (39)

Total................................................................ $ 9 $191

As of December 31, 2007 and 2006, DAC and VOBA for the Individual segment were $14.2 billion and $14.0 billion, respectively, and

for the total Company were $21.5 billion and $20.8 billion, respectively.

Goodwill

Goodwill is the excess of cost over the fair value of net assets acquired. Goodwill is not amortized but is tested for impairment at least

annually or more frequently if events or circumstances, such as adverse changes in the business climate, indicate that there may be

justification for conducting an interim test.

Impairment testing is performed using the fair value approach, which requires the use of estimates and judgment, at the “reporting unit”

level. A reporting unit is the operating segment or a business one level below the operating segment, if discrete financial information is

prepared and regularly reviewed by management at that level. For purposes of goodwill impairment testing, goodwill within Corporate &

Other is allocated to reporting units within the Company’s business segments. If the carrying value of a reporting unit’s goodwill exceeds its

fair value, the excess is recognized as an impairment and recorded as a charge against net income. The fair values of the reporting units

are determined using a market multiple, a discounted cash flow model, or a cost approach. The critical estimates necessary in determining

fair value are projected earnings, comparative market multiples and the discount rate.

Liability for Future Policy Benefits

The Company establishes liabilities for amounts payable under insurance policies, including traditional life insurance, traditional

annuities and non-medical health insurance. Generally, amounts are payable over an extended period of time and related liabilities are

calculated as the present value of expected future benefits to be paid, reduced by the present value of expected future premiums. Such

liabilities are established based on methods and underlying assumptions in accordance with GAAP and applicable actuarial standards.

Principal assumptions used in the establishment of liabilities for future policy benefits are mortality, morbidity, policy lapse, renewal,

retirement, investment returns, inflation, expenses and other contingent events as appropriate to the respective product type. These

assumptions are established at the time the policy is issued and are intended to estimate the experience for the period the policy benefits

11MetLife, Inc.