Reebok 2012 Annual Report Download - page 241

Download and view the complete annual report

Please find page 241 of the 2012 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

|

|

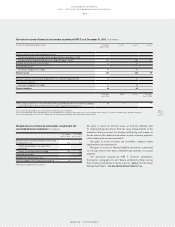

adidas Group

/

2012 Annual Report

Consolidated Financial Statements

219

2012

/

04.8

/

Notes

/

Notes to the Consolidated Statement of Financial Position

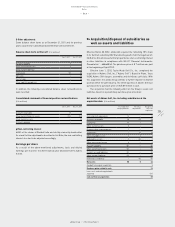

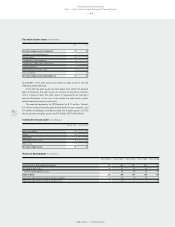

Amounts for defined benefit plans recognised in the

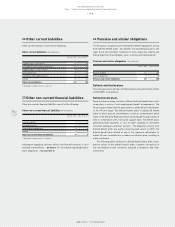

consolidated statement of financial position (€ in millions)

Dec. 31, 2012 Dec. 31, 2011

Present value of funded obligation 89 76

Fair value of plan assets (76) (67)

Funded status 13 9

Present value of unfunded obligation 228 184

Asset ceiling effect 0 1

Net defined benefit liability 241 194

Thereof: liability 241 195

Thereof: adidas AG 196 154

Thereof: asset (0) (1)

Thereof: adidas AG – (1)

The asset ceiling effect arises from a funded defined benefit plan

in Germany and is recognised in the consolidated statement of

comprehensive income.

The determination of assets and liabilities for defined benefit plans

is based upon statistical and actuarial valuations. In particular, the

present value of the defined benefit obligation is driven by financial

variables (such as the discount rates or future increases in salaries) and

demographic variables (such as mortality and employee turnover). The

actuarial assumptions may differ significantly from the actual results,

i.e. the present value of the actual future performance may differ from

the reported present value.

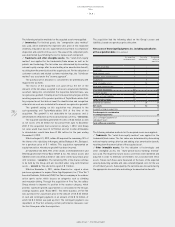

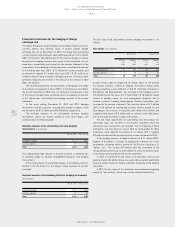

Actuarial assumptions (in %)

Dec. 31, 2012 Dec. 31, 2011

Discount rate 3.5 4.3

Expected rate of salary increases 3.2 3.3

Expected pension increases 2.1 2.1

Expected return on plan assets 4.0 4.8

The actuarial assumptions as at the balance sheet date are used to

determine the defined benefit liability at that date and the pension

expense for the upcoming financial year.

The actuarial assumptions for withdrawal and mortality rates are

based on statistical information available in the various countries, the

latter for Germany on the Heubeck 2005 G mortality tables.

The calculation of the pension liabilities in Germany is based on a

discount rate determined using the Mercer Pension Discount Yield Curve

(MPDYC) approach which was adjusted in 2012 due to the current market

development. Had a discount rate been used which was based on the

previous year-end’s approach, the defined benefit obligation would have

increased by approximately € 20 million.

The Group recognises actuarial gains or losses arising in defined

benefit plans during the financial year immediately outside the income

statement in the consolidated statement of comprehensive income.

The actuarial losses recognised in this statement for 2012 amount to

€ 35 million (2011: € 13 million). The accumulated actuarial losses

recognised amount to € 86 million (2011: € 51 million).

In 2012, the expected return on plan assets assumption was set

separately, by aggregating the expected rate of return for each asset

class over the underlying asset allocation, for the various benefit plans.

Historical markets were studied and expected returns were based on

widely accepted capital market principles.

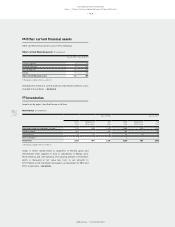

Pension expenses for defined benefit plans (€ in millions)

Year ending

Dec. 31, 2012

Year ending

Dec. 31, 2011

Current service cost 16 12

Interest cost 11 11

Expected return on plan assets (3) (4)

Pension expenses for defined benefit plans 24 19

Of the total pension expenses, an amount of € 15 million (2011:

€ 13 million) relates to employees of adidas AG. The pension expense

is mainly recorded within other operating expenses. The production-

related part of the pension expenses is recognised within cost of sales.

Present value of the defined benefit obligation (€ in millions)

2012 2011

Present value of the defined benefit obligation

as at January 1 260 237

Currency translation differences 2 3

Current service cost 16 12

Interest cost 11 11

Contribution by plan participants 0 0

Pensions paid (11) (10)

Actuarial loss 39 10

Plan settlements 0 (3)

Present value of the defined benefit obligation

as at December 31 317 260