Reebok 2012 Annual Report Download - page 193

Download and view the complete annual report

Please find page 193 of the 2012 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

|

|

adidas Group

/

2012 Annual Report

Group Management Report – Financial Review

171

2012

/

03.5

/

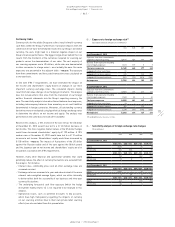

Risk and Opportunity Report

/

Operational risks

To mitigate these risks, we continuously monitor the global

transportation market in order to be able to quickly adapt to changes

in the transportation environment and secure required capacity. We

work closely with multiple logistics service providers to guarantee

transportation of our products to the desired destinations. In addition,

we buy insurance coverage against theft or physical damage during

transportation and storage. Furthermore, in case of malfunctioning

logistics systems, we actively re-prioritise the allocation of products to

minimise damage caused.

Given the importance of logistics processes to ensure the proper flow of

goods, we evaluate the potential impact of logistics risks as significant.

We assess the likelihood of materialising as likely, due to our global

footprint.

Marketing risks

Flawless execution of marketing activities is critical to the success of

the Group and its brands. Therefore, unaligned product creation, range

development, go-to-market or brand communication processes could

lead to additional costs, suboptimal sales performance and the inability

to resonate with the consumer as desired. Poorly executed marketing

activities may also result in negative media coverage and hurt brand

image. Similarly, inadequate or insufficient investment in brand-building

could negatively affect our ability to maintain brand momentum and our

competitive edge in the marketplace.

In order to reduce such risks, our global and local marketing departments

are constantly cooperating and thereby ensuring consistent execution

of key initiatives. Through continuous planning and alignment within

the marketing organisation and also cross-functionally, we enable

both consumer relevance and operational excellence. Despite our

brands’ marketing strength and track record, these risks could have a

significant potential impact for the Group, and we assess the likelihood

of materialising as likely.

Customer relationship risks

Building strong relationships with retailers to become a valuable and

reliable business partner for them is one of the guiding principles of our

Wholesale segment

/

SEE WHOLESALE STRATEGY, P. 73. Failure to cement

and maintain strong relationships with retailers could have substantial

negative effects on our wholesale activities and thus the Group’s business

performance. Losing important customers in key markets due to subpar

relationship management would result in significant sales shortfalls.

Therefore, the Group is committed to delivering outstanding customer

service, providing our retail partners with the support and tools to

establish and maintain a mutually successful business relationship.

Customer relationship management is not only a key activity for our

sales force but also of highest importance to our Group’s top executives

and second-line management. As a result, the Group’s CEO, for example,

regularly meets with key customers to ensure a strong partnership

between the Group and its retail customers. Should customer

relationship risks materialise, however, the potential impact for the

Group could be major. However, due to our commitment, dedication

and continuous efforts to strengthen our partnerships with retailers, we

regard the likelihood of materialising as unlikely.

Sales and pricing risks

To achieve our sales and profitability targets, it is paramount to

successfully convert orders into sales, drive sell-through at the point of

sale and have product prices that are competitive in the marketplace.

Failure to do so would result in sales and profit shortfalls. In addition,

price increases required to compensate for higher product costs might

not be realised in the marketplace, leading to margin declines.

To mitigate these risks, we pursue a range of pricing strategies. We closely

monitor order book conversion, sell-out and sell-through performance

and adjust prices where required. In addition, our continuous investment

in brand-building and marketing helps us drive our business at various

price points and supports a premium positioning. Furthermore, we

work closely with our retail customers to minimise mark-downs and

potentially re-allocate product.

We believe the potential impact of sales and pricing risks could be

major. Given our brand strength, consumer appeal and surgical pricing

activities, we rate the likelihood of materialising only as possible.

Supplier risks

Almost the entire adidas Group product offering is sourced through

independent suppliers, mainly located in Asia

/

SEE GLOBAL OPERATIONS,

P. 100. To reduce the risk of business interruptions following the potential

underperformance of a supplier or a potential supplier default, we

work with vendors who demonstrate reliability, quality, innovation and

continuous improvement.

Furthermore, in order to minimise any potential negative consequences

such as product quality shortfalls, increased product lead times or

violation of our Workplace Standards, we enforce strict control and

inspection procedures at our suppliers and also demand adherence to

social and environmental standards throughout our supply chain

/

SEE

SUSTAINABILITY, P. 117. In addition, we have bought insurance coverage for

the risk of business interruptions caused by physical damage to supplier

premises. As a result, and in spite of our mitigating actions, we assess

supplier risks as having a major potential impact. However, we regard

the likelihood of being impacted to such a degree as unlikely.