Reebok 2012 Annual Report Download - page 199

Download and view the complete annual report

Please find page 199 of the 2012 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

|

|

adidas Group

/

2012 Annual Report

Group Management Report – Financial Review

177

2012

/

03.5

/

Risk and Opportunity Report

/

Financial risks

05

/

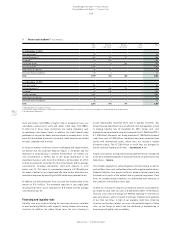

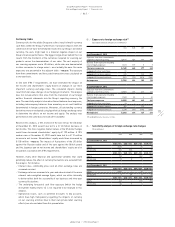

Exposure to foreign exchange risk 1)

(based on notional amounts, € in millions)

USD RUB GBP JPY

As at December 31, 2012

Exposure from firm commitments

and forecasted transactions (3,819) 359 369 354

Balance sheet exposure including

intercompany exposure (321) 109 8 8

Total gross exposure (4,140) 468 377 362

Hedged with other cash flows 91

Hedged with currency options 225 (12) (24)

Hedged with forward contracts 2101 (72) (263) (188)

Net exposure (1,723) 396 102 150

As at December 31, 2011

Exposure from firm commitments

and forecasted transactions (3,859) 298 330 331

Balance sheet exposure including

intercompany exposure (140) 83 2 30

Total gross exposure (3,999) 381 332 361

Hedged with other cash flows 93 – – –

Hedged with currency options 365 – (11) –

Hedged with forward contracts 2,298 (47) (194) (145)

Net exposure (1,243) 334 127 216

1) Rounding difference may arise in totals.

06

/

Sensitivity analysis of foreign exchange rate changes

(€ in millions)

USD RUB GBP JPY

As at December 31, 2012

EUR +10% USD +10% EUR +10% EUR +10%

Equity (129) – 20 15

Net income (13) (10) 0 (1)

EUR –10% USD –10% EUR –10% EUR –10%

Equity 158 – (24) (18)

Net income 12 8 0 1

As at December 31, 2011

EUR +10% USD +10% EUR +10% EUR +10%

Equity (195) – 15 11

Net income 5 (9) 0 (3)

EUR –10% USD –10% EUR –10% EUR –10%

Equity 243 – (19) (13)

Net income (6) 7 0 4

Currency risks

Currency risks for the adidas Group are a direct result of multi-currency

cash flows within the Group. Furthermore, translation impacts from the

conversion of non-euro-denominated results into our Group’s functional

currency, the euro, might lead to a material negative impact on our

Group’s financial performance. The biggest single driver behind this risk

results from the mismatch of the currencies required for sourcing our

products versus the denominations of our sales. The vast majority of

our sourcing expenses are in US dollars, while sales are denominated

in other currencies to a large extent – most notably the euro. Our main

exposures are presented in the adjacent table

/

TABLE 05. The exposure

from firm commitments and forecasted transactions was calculated on

a one-year basis.

In line with IFRS 7 requirements, we have estimated the impact on

net income and shareholders’ equity based on changes in our most

important currency exchange rates. The calculated impacts mainly

result from fair value changes of our hedging instruments. The analysis

does not include effects that arise from the translation of our foreign

entities’ financial statements into the Group’s reporting currency, the

euro. The sensitivity analysis is based on the net balance sheet exposure,

including intercompany balances from monetary assets and liabilities

denominated in foreign currencies. Moreover, all outstanding currency

derivatives were re-evaluated using hypothetical foreign exchange rates

to determine the effects on net income and equity. The analysis was

performed on the same basis for both 2011 and 2012.

Based on this analysis, a 10% increase in the euro versus the US dollar

at December 31, 2012 would have led to a € 13 million decrease in

net income. The more negative market values of the US dollar hedges

would have decreased shareholders’ equity by € 129 million. A 10%

weaker euro at December 31, 2012 would have led to a € 12 million

increase in net income. Shareholders’ equity would have increased by

€ 158 million

/

TABLE 06. The impacts of fluctuations of the US dollar

against the Russian rouble and of the euro against the British pound

and the Japanese yen on net income and shareholders’ equity are also

included in accordance with IFRS requirements.

However, many other financial and operational variables that could

potentially reduce the effect of currency fluctuations are excluded from

the analysis. For instance:

/

Interest rates, commodity prices and all other exchange rates are

assumed constant.

/

Exchange rates are assumed at a year-end value instead of the more

relevant sales-weighted average figure, which we utilise internally

to better reflect both the seasonality of our business and intra-year

currency fluctuations.

/

The underlying forecasted cash flow exposure (which the hedge

instrument mainly relates to) is not required to be revalued in this

analysis.

/

Operational issues, such as potential discounts to key accounts,

which have high transparency regarding the impacts of currency

on our sourcing activities (due to their own private label sourcing

efforts), are also excluded from this presentation.