Reebok 2012 Annual Report Download - page 198

Download and view the complete annual report

Please find page 198 of the 2012 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

|

|

adidas Group

/

2012 Annual Report

Group Management Report – Financial Review

176

2012

/

03.5

/

Risk and Opportunity Report

/

Financial risks

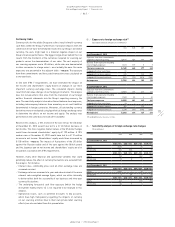

04

/

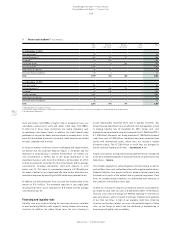

Future cash outflows 1) (€ in millions)

Up to

1 year

Between

1 and 3 years

Between

3 and 5 years

After

5 years

Total

As at December 31, 2012

Bank borrowings 2) 59 – – – 59

Private placements 3) 242 169 117 528

Eurobond 3) 24 514 538

Convertible bond 3) 1 3 503 – 507

Accounts payable 1,790 1,790

Other financial liabilities 26 14 40

Derivative financial liabilities 57 3 60

Total 2,199 703 620 – 3,522

As at December 31, 2011

Bank borrowings 2) 126 – – – 126

Private placements 3) 193 418 119 – 730

Eurobond 3) 24 538 – – 562

Accounts payable 1,887 – – – 1,887

Other financial liabilities 34 7 – – 41

Derivative financial liabilities 32 2 – – 34

Total 2,296 965 119 3,380

1) Rounding difference may arise in totals.

2) Classified as long-term (between 1 and 3 years) in the consolidated financial statements, as they are covered by the committed mid-term syndicated loan.

3) Including interest payments.

work with banks rated BBB+ or higher. Only in exceptional cases are

subsidiaries authorised to work with banks rated lower than BBB+.

To limit risk in these cases, restrictions are clearly stipulated, such

as maximum cash deposit levels. In addition, the credit default swap

premiums of our partner banks are monitored on a weekly basis. In the

event that the defined threshold is exceeded, credit balances are shifted

to banks compliant with the limit.

As financial market conditions remain challenging and highly volatile,

we believe that the potential financial impact is moderate and the

likelihood of materialising is unlikely. Furthermore, we believe our

risk concentration is limited due to the broad distribution of our

investment business with more than 20 banks. At December 31, 2012,

no bank accounted for more than 5% of our investments and the average

concentration, including subsidiaries’ short-term deposits in local

banks, was 1%. This leads to a maximum exposure of € 98 million in

the event of default of any single bank. We have further diversified our

investment exposure by investing into AAA-rated money market funds.

In addition, we held derivatives with a positive fair market value in the

amount of € 61 million. The maximum exposure to any single bank

resulting from these assets amounted to € 8 million and the average

concentration was 5%.

Financing and liquidity risks

Liquidity risks arise from not having the necessary resources available

to meet maturing liabilities with regard to timing, volume and currency

structure. In addition, the adidas Group faces the risk of having to

accept unfavourable financing terms due to liquidity restraints. Our

Group Treasury department uses an efficient cash management system

to manage liquidity risk. At December 31, 2012, Group cash, cash

equivalents and marketable securities amounted to € 1.935 billion (2011:

€ 1.370 billion). Moreover, our Group maintains € 1.863 billion bilateral

credit lines and a € 500 million committed long-term syndicated loan

facility with international banks, which does not include a market

disruption clause. The € 2.363 billion in credit lines are designed to

ensure sufficient liquidity at all times

/

SEE TREASURY, P. 141.

Future cash outflows arising from financial liabilities that are recognised

in the Consolidated Statement of Financial Position are presented in the

table above

/

TABLE 04.

This includes payments to settle obligations from borrowings as well as

cash outflows from cash-settled derivatives with negative market values.

Financial liabilities that may be settled in advance without penalty are

included on the basis of the earliest date of potential repayment. Cash

flows for variable-interest liabilities are determined with reference to

the conditions at the balance sheet date.

In 2012, we continued to improve our financial position substantially as

we ended the year with net cash of € 448 million (2011: € 90 million).

Thus the ratio of net borrowings over EBITDA improved to –0.3 times at

year-end, which is well in line with the Group’s medium-term guideline

of less than two times. In light of our available credit lines, financing

structure and business model, we assess the potential impact of these

risks on the Group as minor and the likelihood of materialising of

financing and liquidity risks as unlikely.