Reebok 2012 Annual Report Download - page 197

Download and view the complete annual report

Please find page 197 of the 2012 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

|

|

adidas Group

/

2012 Annual Report

Group Management Report – Financial Review

175

2012

/

03.5

/

Risk and Opportunity Report

/

Financial risks

As our brands remain a key factor for our Group’s success, we assess the

potential impact related to counterfeiting and imitation as significant but,

as a result of our relentless and intensive efforts against counterfeiting,

we rate the likelihood of being impacted to such a degree as unlikely.

Product quality risks

The adidas Group faces a risk of selling defective products, which

may result in injury to consumers and/or brand and product image

impairment. We mitigate this risk by employing dedicated teams that

monitor the quality of our products on all levels of the supply chain

through rigorous testing prior to production, close cooperation with

suppliers throughout the manufacturing process, random testing after

retail delivery, open communication about defective products and quick

settlement of product liability claims when necessary. In 2012, we did not

recall any products.

The potential impact of product liability cases or having to conduct

wide-scale product recalls could be significant but, given our internal

standards and control activities regarding product quality, we regard the

likelihood as possible.

Fraud and corruption risks

We face the risk that our employees breach rules and standards that

guide appropriate and responsible business behaviour. This includes

the risks of fraud and corruption. In order to successfully manage

these risks, the Group Policy Manual was launched at the end of 2006

to provide a framework for basic work procedures and processes. It

also includes our Code of Conduct

/

SEE CORPORATE GOVERNANCE REPORT

INCLUDING THE DECLARATION ON CORPORATE GOVERNANCE, P. 51 which stipulates

that every employee shall act ethically in compliance with the laws and

regulations of the legal systems where they conduct Group business.

All of our employees have to participate in a special Code of Conduct

training as part of our Global Compliance Programme.

In addition, we utilise controls such as segregation of duties in IT

systems to prevent fraudulent activities. Moreover, we have created a

network of Compliance Officers across the Group who guide and advise

our operating managers regarding fraud and corruption topics, and we

are further strengthening our internal control activities by highlighting

key controls in our business processes to prevent and detect fraudulent

or corruptive behaviour. Various additional mechanisms are in place to

monitor compliance. Whenever reasonable, we actively investigate and,

in case of unlawful conduct, we work with state authorities to ensure

rigorous enforcement of criminal law.

We believe the potential impact on the Group’s performance caused by

fraud or corruption could be significant. Despite the substantial growth

of our global workforce in recent years, we regard the likelihood of being

impacted by fraud and corruption risks to such an extent as unlikely,

due to our preventative measures and controls. However, we believe the

likelihood of occurrence of smaller fraud or corruption cases is higher.

Financial risks

Credit risks

A credit risk arises if a customer or other counterparty to a financial

instrument fails to meet its contractual obligations. The adidas Group

is exposed to credit risks from its operating activities and from certain

financing activities. Credit risks arise principally from accounts

receivable and, to a lesser extent, from other third-party contractual

financial obligations such as other financial assets, short-term bank

deposits and derivative financial instruments

/

SEE NOTE 29, P. 224.

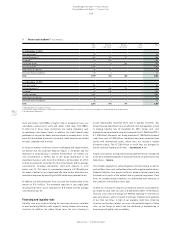

Without taking into account any collateral, the carrying amount of

financial assets and accounts receivable represents the maximum

exposure to credit risk.

At the end of 2012, there was no relevant concentration of credit risk

by type of customer or geography. Our credit risk exposure is mainly

influenced by individual customer characteristics. Under the Group’s

credit policy, new customers are analysed for creditworthiness before

standard payment and delivery terms and conditions are offered.

Tolerance limits for accounts receivable are also established for each

customer. Both creditworthiness and accounts receivable limits are

monitored on an ongoing basis. Customers that fail to meet the Group’s

minimum creditworthiness are, in general, allowed to purchase products

only on a prepayment basis.

Other activities to mitigate credit risks include retention of title clauses

as well as, on a selective basis, credit insurances, accounts receivable

sales without recourse and bank guarantees.

Objective evidence that financial assets are impaired includes, for

instance, significant financial difficulty of the issuer or debtor, indications

of the potential bankruptcy of the borrower and the disappearance of an

active market for a financial asset because of financial difficulties. The

Group utilises allowance accounts for impairments that represent our

estimate of incurred credit losses with respect to accounts receivable.

Allowance accounts are used as long as the Group is satisfied that

recovery of the amount due is possible. Once this is no longer the case,

the amounts are considered irrecoverable and are directly written off

against the financial asset. The allowance consists of two components:

(1) an allowance established for all receivables dependent on the ageing

structure of receivables past due date and

(2) a specific allowance that relates to individually assessed risk for

each specific customer – irrespective of ageing.

At the end of 2012, no Group customer accounted for more than 10% of

accounts receivable. Based on our allowance accounts, we believe that

the potential financial impact of our credit risks from customers could

be major but we rate the likelihood of materialising only as possible.

The adidas Group Treasury department arranges currency and interest

rate hedges, and invests cash, with major banks of a high credit standing

throughout the world. adidas Group companies are authorised to