The Hartford 2007 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2007 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

80

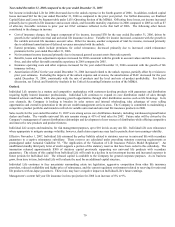

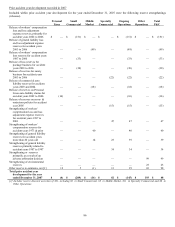

• Within Middle Market, the change from an increase in earned premium in 2006 to a decrease in earned premium in 2007 was

primarily attributable to earned pricing decreases, a decrease in new business written premium over the last six months of 2006 and

the first six months of 2007 and a decrease in premium renewal retention over the first six months of 2007.

• The rate of decline in Specialty Commercial earned premium slowed in 2007, primarily due to a lower earned premium decrease in

casualty and property, partially offset by a lower earned premium increase in professional liability, fidelity and surety. Casualty

earned premium experienced a larger decrease in 2006, primarily because of a decrease in 2006 earned premium from a single

captive insured program that expired in 2005. Earned premium decreases in property were larger in 2006 than in 2007 as a result of

a strategic decision in 2006 not to renew certain accounts with properties in catastrophe-prone areas. The growth rate in

professional liability, fidelity and surety earned premium slowed in 2007 due to a decrease in earned pricing and a decline in new

business growth and premium renewal retention.

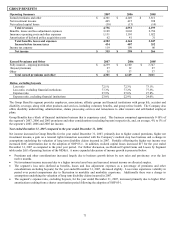

Ongoing Operations combined ratio

For the year ended December 31, 2007, the Ongoing Operations’ combined ratio increased 1.5 points, to 90.8, due to a 2.5 point

increase in the combined ratio before catastrophes and prior accident year development, partially offset by a 0.8 point improvement in

prior accident year reserve development and the effect of the sale of Omni in the fourth quarter of 2006. Omni had a higher combined

ratio before catastrophes and prior accident year development than other business written by the Company.

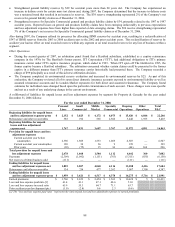

• The increase in the combined ratio before catastrophes and prior accident year development, from 88.0 to 90.5, was primarily due

to a 1.4 point increase in the current accident year loss and loss adjustment expense ratio before catastrophes and, to a lesser extent,

an increase in the expense ratio. The increase in the loss and loss adjustment expense ratio before catastrophes and prior accident

year development was primarily due to increased severity on Personal Lines auto liability claims, increased frequency on Personal

Lines auto property damage claims and, to a lesser extent, increased severity on Personal Lines homeowners claims and a higher

loss and loss adjustment expense ratio for both Small Commercial package business and Middle Market workers’ compensation

claims. Contributing to the increase in the expense ratio was the effect of a $41 reduction of estimated Florida Citizens’

assessments in 2006 related to the 2005 Florida hurricanes.

• The catastrophe ratio increased, primarily due to the effect of net favorable reserve development of prior accident year catastrophe

losses in 2006. In 2006, the Company recognized $83 of net reserve releases related to the 2005 and 2004 hurricanes.

• Net non-catastrophe prior accident year reserve development was slightly unfavorable in 2006, but favorable in 2007. Favorable

reserve development in 2007 was largely attributable to the release of reserves for workers’ compensation claims, primarily related

to accident years 2002 to 2006. See the “Reserves” section for a discussion of prior accident year reserve development for Ongoing

Operations in 2007.

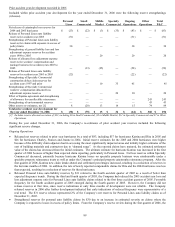

Other Operations net income (loss)

• Other Operations reported net income of $30 in 2007 compared to a net loss of $35 in 2006. The improvement in results was

primarily due to a decrease in unfavorable prior accident year reserve development, partially offset by a change from net realized

gains in 2006 to net realized losses in 2007 and a decrease in net investment income. See the Other Operations segment MD&A for

further discussion.

Investment yield and average invested assets

• In 2007, the after-tax investment yield increased due to a higher yield on limited partnerships, hedge funds and mortgage loans as

well as due to a change in asset mix, including shifting a greater share of investments to these asset classes.

• The average annual invested assets at cost increased as a result of positive operating cash flows and an increase in collateral held

from increased securities lending activities.

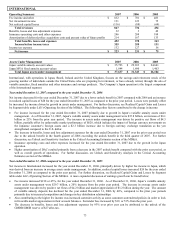

Year ended December 31, 2006 compared to the year ended December 31, 2005

Ongoing Operations earned premium growth

• The lower growth rate in Personal Lines was primarily due to unfavorable changes in earned pricing and the effect of higher

property catastrophe treaty reinsurance costs. Partially offsetting the lower growth rate was the effect of $31 of catastrophe treaty

reinstatement premium recorded as a reduction of earned premium in 2005 and an increase in new business written premium in auto

and homeowners. During 2006, there was a decline in earned pricing increases in homeowners and a change from slight earned

pricing increases for auto in 2005 to flat earned pricing for auto in 2006.

• The lower growth rate in Small Commercial was primarily attributable to a decrease in new business written premium, lower

earned pricing increases and higher property catastrophe treaty reinsurance costs.

• The lower growth rate in Middle Market was primarily attributable to a decrease in new business written premium in the first six

months of 2006, larger earned pricing decreases and higher property catastrophe treaty reinsurance costs.

• The decline in Specialty Commercial earned premium in 2006 primarily resulted from the non-renewal of a single captive insurance

program within specialty casualty that accounted for $241 of earned premium in 2005 and a decrease in specialty property earned

premium, partially offset by the effect of $26 of catastrophe treaty reinstatement premium recorded as a reduction of earned

premium in 2005 and a higher growth rate in professional liability, fidelity and surety business.