The Hartford 2007 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2007 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

117

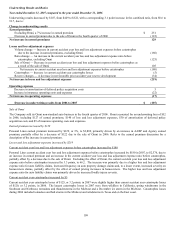

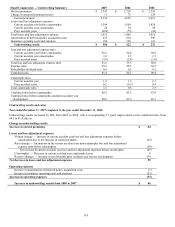

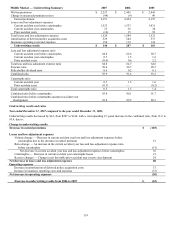

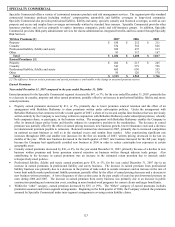

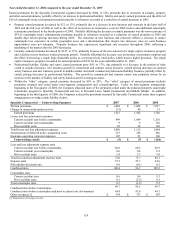

Operating expenses increased by $25

The expense ratio decreased by 1.7 points, to 28.5, primarily due to a decrease in insurance operating costs and expenses. Insurance

operating costs decreased by $13, largely because of a $10 decrease in estimated Citizens’ assessments in 2006 compared to a $16

increase in Citizens assessments in 2005. Partially offsetting the improvement due to changes in the Citizens’ assessments was an

increase in IT and other insurance operating costs. Amortization of deferred policy acquisition costs increased by $38, due largely to

the increase in earned premium.

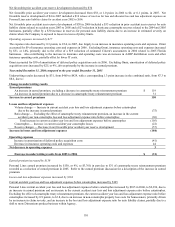

Outlook

Management expects written premium in 2008 to be flat to 3% higher than in 2007 as it seeks to increase the flow of new business from

its agents. Small Commercial expects to increase written premium by selectively expanding its underwriting appetite, refining its

pricing models and upgrading product features. In 2008, the Company expects to add a pricing tier for workers’ compensation business

to provide more pricing flexibility and introduce an enhanced renewal pricing model for the Company’ s Spectrum business owners’

package product. Despite a decline in new business in 2007, management expects new business will increase in 2008, driven by an

increased flow of new business submissions from the larger producers. Including supplemental commissions, the Company has

increased commissions paid to agents and expects that this will help it achieve its growth objectives in 2008.

Through technology and process improvements, in 2008, the Company plans to improve efficiency and service levels in its underwriting

centers and enhance the agent’ s on-line experience. Average premium per policy is expected to continue to decline due to the sale of

more liability-only policies, workers’ compensation rate reductions and a lower average premium on Next Generation Auto business.

Written pricing has remained relatively flat for Small Commercial business as carriers have competed for new business through new

product features and expanded coverage. In 2008, the Company will continue to focus on renewal retention, particularly in the mid-

Western states, where competition has been particularly strong.

Reflecting favorable trends in workers’ compensation loss costs in recent accident years, management expects a slightly lower loss and

loss adjustment expense ratio for workers’ compensation claims in the 2008 accident year, although the improvement, if any, depends

on continued favorable frequency. Loss costs are expected to continue to increase on non-catastrophe commercial auto property claims,

reflecting a continuation of higher loss costs on commercial auto business in 2007. Based on anticipated trends in earned pricing and

loss costs, the combined ratio before catastrophes and prior accident year development is expected to be in the range of 86.0 to 89.0 in

2008. The combined ratio before catastrophes and prior accident year development was 88.0 in 2007.

To summarize, management’ s outlook in Small Commercial for the 2008 full year is:

• Written premium flat to 3% higher

• A combined ratio before catastrophes and prior accident year development of 86.0 to 89.0