The Hartford 2007 Annual Report Download - page 248

Download and view the complete annual report

Please find page 248 of the 2007 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued)

F-71

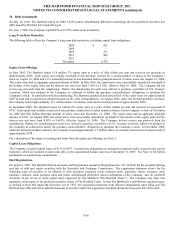

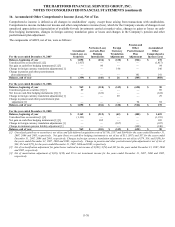

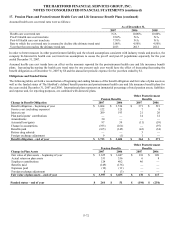

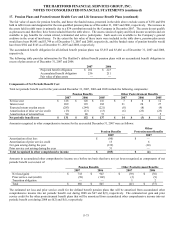

17. Pension Plans and Postretirement Health Care and Life Insurance Benefit Plans

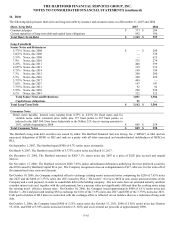

The Company maintains a qualified defined benefit pension plan (the “Plan”) that covers substantially all employees. Effective for all

employees who joined the Company on or after January 1, 2001, a new component or formula was applied under the Plan referred to as

the “cash balance formula”. As of January 1, 2009, the cash balance formula will be used to calculate future pension benefits for

services rendered on or after January 1, 2009 for all employees hired before January 1, 2001. These amounts are in addition to amounts

earned by those employees through December 31, 2008 under the traditional final average pay formula.

The Company also maintains non-qualified pension plans to accrue retirement benefits in excess of Internal Revenue Code limitations.

The Company provides certain health care and life insurance benefits for eligible retired employees. The Company’ s contribution for

health care benefits will depend upon the retiree’ s date of retirement and years of service. In addition, the plan has a defined dollar cap

for certain retirees which limits average Company contributions. The Hartford has prefunded a portion of the health care obligations

through a trust fund where such prefunding can be accomplished on a tax effective basis. Effective January 1, 2002, Company-

subsidized retiree medical, retiree dental and retiree life insurance benefits were eliminated for employees with original hire dates with

the Company on or after January 1, 2002.

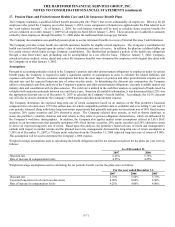

Assumptions

Pursuant to accounting principles related to the Company’ s pension and other postretirement obligations to employees under its various

benefit plans, the Company is required to make a significant number of assumptions in order to calculate the related liabilities and

expenses each period. The two economic assumptions that have the most impact on pension and other postretirement expense are the

discount rate and the expected long-term rate of return on plan assets. In determining the discount rate assumption, the Company

utilizes a discounted cash flow analysis of the Company’ s pension and other postretirement obligations, currently available market and

industry data and consultation with its plan actuaries. The yield curve utilized in the cash flow analysis is comprised of bonds rated Aa

or higher with maturities primarily between zero and thirty years. Based on all available information, it was determined that 6.25% was

the appropriate discount rate as of December 31, 2007 to calculate the Company’s benefit liability. Accordingly, the 6.25% discount

rate will also be used to determine the Company’ s 2008 pension and other postretirement expense.

The Company determines the expected long-term rate of return assumption based on an analysis of the Plan portfolio’ s historical

compound rates of return since 1979 (the earliest date for which comparable portfolio data is available) and over rolling 5 year and 10

year periods, balanced along with future long-term return expectations that generally anticipate an investment mix of 60% fixed income

securities, 20% equity securities and 20% alternative assets. The Company selected these periods, as well as shorter durations, to

assess the portfolio’ s volatility, duration and total returns as they relate to pension obligation characteristics, which are influenced by

the Company’ s workforce demographics. In addition, the Company also applies market return assumptions utilized in Life’ s DAC

analysis to an investment mix that generally anticipates 60% fixed income securities, 20% equity securities and 20% alternative assets

to derive an expected long-term rate of return. Based upon this analysis, the portfolio’ s historical rates of return and management’ s

outlook with respect to market returns and the planned asset mix, management decreased the long-term rate of return assumption to

7.30% as of December 31, 2007, a 70 basis point reduction from the December 31, 2006 expected long-term rate of return of 8.00%.

This assumption will be used to determine the Company’ s 2008 expense.

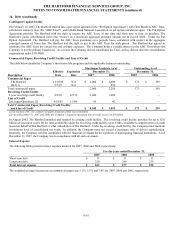

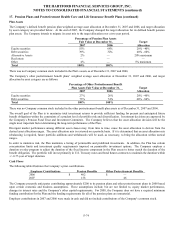

Weighted average assumptions used in calculating the benefit obligations and the net amount recognized for the plans per year were as

follows:

As of December 31,

2007 2006

Discount rate 6.25% 5.75%

Rate of increase in compensation levels 4.25% 4.25%

Weighted average assumptions used in calculating the net periodic benefit cost for the plans were as follows:

For the year ended December 31,

2007 2006 2005

Discount rate 5.75% 5.50% 5.75%

Expected long-term rate of return on plan assets 8.00% 8.00% 8.50%

Rate of increase in compensation levels 4.25% 4.00% 4.00%