The Hartford 2007 Annual Report Download - page 125

Download and view the complete annual report

Please find page 125 of the 2007 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

125

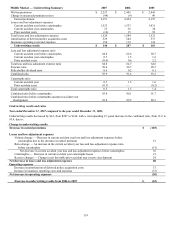

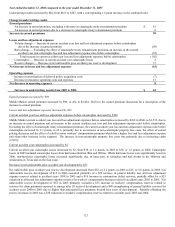

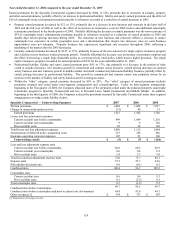

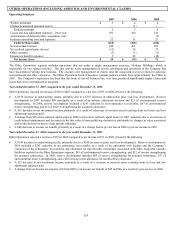

Underwriting Results and Ratios

Year ended December 31, 2007 compared to the year ended December 31, 2006

Underwriting results decreased by $58, with a corresponding 3.7 point increase in the combined ratio, to 100.4, due to:

Change in underwriting results

Decrease in earned premiums $(47)

Losses and loss adjustment expenses

Volume change — Decrease in current accident year loss and loss adjustment expenses before

catastrophes due to the decrease in earned premium

37

Ratio change — Decrease in the current accident year non-catastrophe loss and loss adjustment expense

ratio before catastrophes

33

Total decrease in current accident year loss and loss adjustment expenses before catastrophes 70

Reserve changes — Increase in net unfavorable prior accident year reserve development (48)

Net decrease in losses and loss adjustment expenses 22

Operating expenses

Increase in amortization of deferred policy acquisition costs (17)

Increase in insurance operating costs and expenses (16)

Increase in operating expenses (33)

Decrease in underwriting results from 2006 to 2007 $

(58)

Earned premium decreased by $47

Specialty Commercial earned premium decreased by $47, or 3%, to $1,515. Refer to the earned premium discussion for a description of

the decrease in earned premium.

Losses and loss adjustment expenses decreased by $22

Current accident year loss and loss adjustment expenses before catastrophes decreased by $70

Specialty Commercial current accident year loss and loss adjustment expenses before catastrophes decreased by $70 in 2007 to $999,

due to a decrease in earned premium and a 2.2 point decrease in the loss and loss adjustment expense ratio before catastrophes and prior

accident year development, to 66.0. The decrease in the loss and loss adjustment expense ratio before catastrophes and prior accident

year development was driven by a lower loss and loss adjustment ratio on directors and officers insurance in professional liability and a

decrease in non-catastrophe property loss costs on property business, partially offset by a higher loss and loss adjustment expense ratio

on casualty business.

Increase in net unfavorable prior accident year development by $48

Net unfavorable prior accident year reserve development increased from $34, or 2.3 points, in 2006 to $82, or 5.4 points, in 2007. Net

unfavorable prior accident year reserve development of $82 in 2007 consisted primarily of a $47 strengthening of workers’

compensation loss and loss adjustment expense reserves for accident years 1987 to 2001, a $34 strengthening of general liability reserves,

primarily related to accident years 1987 to 1997 and a $25 strengthening of general liability reserves for accident years more than 20 years

old. Partially offsetting the unfavorable reserve development in 2007 was a $22 release of reserves for surety business for accident years

2003 to 2006.

Net unfavorable prior accident year reserve development of $34 in 2006 included a $35 strengthening of reserves for construction

defects claims on casualty business for accident years 1997 and prior and a $20 strengthening of allocated loss adjustment expense

reserves on workers’ compensation policies for claim payments expected to emerge after 20 years of development, partially offset by a

$35 reduction in catastrophe reserves related to the 2005 hurricanes.

Operating expenses increased by $33

Insurance operating costs and expenses increased by $16, primarily due to a $16 increase in policyholder dividends. The $16 increase

in policyholder dividends was largely due to a $10 reduction in estimated policyholder dividends recorded in 2006 and a $7 increase in

estimated policyholder dividends recorded in 2007. The $7 increase in dividends in 2007 was primarily driven by an increase in the

estimated amount of dividends payable to certain workers’ compensation policyholders due to underwriting profits. Amortization of

deferred policy acquisition costs increased by $17, due largely to an increase in amortization for professional liability, fidelity and

surety business driven largely by the increase in earned premiums for that business and a reduction in ceding commissions. The

expense ratio increased by 1.8 points, to 27.5, due largely to the reduction in ceding commission on professional liability business and

the decrease in earned premiums.