The Hartford 2007 Annual Report Download - page 195

Download and view the complete annual report

Please find page 195 of the 2007 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

THE HARTFORD FINANCIAL SERVICES GROUP, INC.

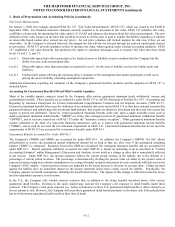

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued)

F-18

1. Basis of Presentation and Accounting Policies (continued)

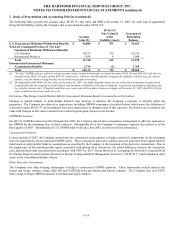

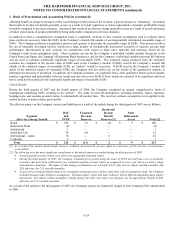

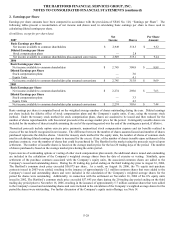

The following table presents the fair value of fixed maturity securities by pricing source as of December 31, 2007 and 2006.

2007 2006

Fair Value

Percentage

of Total

Fair Value

Fair Value

Percentage

of Total

Fair Value

Priced via third party pricing services $ 66,771 83.4% $ 69,023 87.3%

Priced via independent broker quotations 7,561 9.4% 4,309 5.4%

Priced via matrices 5,426 6.8% 5,605 7.1%

Priced via other methods 297 0.4% 137 0.2%

Total $ 80,055 100.0% $ 79,074 100.0%

The fair value of a financial instrument is the amount at which the instrument could be exchanged in a current transaction between

knowledgeable, unrelated willing parties using inputs, including assumptions and estimates, a market participant would utilize. As

such, the estimated fair value of a financial instrument may differ significantly from the amount that could be realized if the security

was sold immediately.

Other-Than-Temporary Impairments on Available-for-Sale Securities

One of the significant estimates inherent in the valuation of investments is the evaluation of investments for other-than-temporary

impairments. The evaluation of impairments is a quantitative and qualitative process, which is subject to risks and uncertainties and is

intended to determine whether declines in the fair value of investments should be recognized in current period earnings. The risks and

uncertainties include changes in general economic conditions, the issuer’ s financial condition or near term recovery prospects, the

effects of changes in interest rates or credit spreads and the recovery period. The Company’ s accounting policy requires that a decline

in the value of a security below its cost or amortized cost basis be assessed to determine if the decline is other-than-temporary. If the

security is deemed to be other-than-temporarily impaired, a charge is recorded in net realized capital losses equal to the difference

between the fair value and cost or amortized cost basis of the security. In addition, for securities expected to be sold, an other-than-

temporary impairment charge is recognized if the Company does not expect the fair value of a security to recover to cost or amortized

cost prior to the expected date of sale. The fair value of the other-than-temporarily impaired investment becomes its new cost basis.

The Company has a security monitoring process overseen by a committee of investment and accounting professionals (“the

committee”) that identifies securities that, due to certain characteristics, as described below, are subjected to an enhanced analysis on a

quarterly basis.

Securities not subject to EITF Issue No. 99-20, “Recognition of Interest Income and Impairment on Purchased Beneficial Interests and

Beneficial Interests That Continued to Be Held by a Transferor in Securitized Financial Assets” (“non-EITF Issue No. 99-20

securities”) that are in an unrealized loss position, are reviewed at least quarterly to determine if an other-than-temporary impairment is

present based on certain quantitative and qualitative factors. The primary factors considered in evaluating whether a decline in value

for non-EITF Issue No. 99-20 securities is other-than-temporary include: (a) the length of time and the extent to which the fair value

has been or is expected to be less than cost or amortized cost, (b) the financial condition, credit rating and near-term prospects of the

issuer, (c) whether the debtor is current on contractually obligated interest and principal payments and (d) the intent and ability of the

Company to retain the investment for a period of time sufficient to allow for recovery.

For certain securitized financial assets with contractual cash flows including ABS, EITF Issue No. 99-20 requires the Company to

periodically update its best estimate of cash flows over the life of the security. If the fair value of a securitized financial asset is less

than its cost or amortized cost and there has been a decrease in the present value of the estimated cash flows since the last revised

estimate, considering both timing and amount, an other-than-temporary impairment charge is recognized. The Company also considers

its intent and ability to retain a temporarily impaired security until recovery. Estimating future cash flows is a quantitative and

qualitative process that incorporates information received from third party sources along with certain internal assumptions and

judgments regarding the future performance of the underlying collateral. In addition, projections of expected future cash flows may

change based upon new information regarding the performance of the underlying collateral.

Each quarter, during this analysis, the Company asserts its intent and ability to retain until recovery those securities judged to be

temporarily impaired. Once identified, these securities are systematically restricted from trading unless approved by the committee.

The committee will only authorize the sale of these securities based on predefined criteria that relate to events that could not have been

foreseen. Examples of the criteria include, but are not limited to, the deterioration in the issuer’ s creditworthiness, a change in

regulatory requirements or a major business combination or major disposition.