SunTrust 2006 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2006 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

|

|

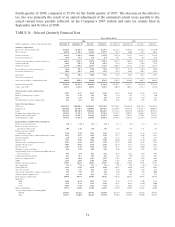

Derivative hedging instrument activities are as follows:

Notional Values1

(Dollars in millions) Asset Hedges Liability Hedges Total

Balance, January 1, 2005 $3,870 $13,482 $17,352

Additions 2,300 4,223 6,523

Terminations (300) (300) (600)

Hedge accounting correction (18) (1,100) (1,118)

Maturities (52) (3,773) (3,825)

Balance, December 31, 2005 $5,800 $12,532 $18,332

Additions 1,500 5,850 7,350

Maturities (300) (2,200) (2,500)

Terminations - (1,700) (1,700)

Dedesignations - (8,394) (8,394)

Balance, December 31, 2006 $7,000 $6,088 $13,088

1Includes only derivative financial instruments which are currently qualifying hedges under SFAS No. 133. Certain other derivatives that are effective for

risk management purposes, but which are not in designated hedging relationships under SFAS No. 133, are not incorporated in this table. Excludes hedges

for the Company's mortgage loans held for sale. As of December 31, 2006 and 2005, the notional amount of mortgage derivative contracts totaled $6.8

billion and $14.4 billion, respectively.

The following table presents the expected maturities of derivative financial instruments:

As of December 31, 2006 1

1 Year

or Less

1-2

Years

2-5

Years

5-10

Years

After 10

Years Total

(Dollars in millions)

Cash Flow Asset Hedges

Notional amount - swaps $4,900 $600 $1,500 $- $- $7,000

Net unrealized gain (loss) (30) (9) 24 - - (15)

Weighted average receive rate 23.68 % 3.95 % 5.50 % - % - % 4.09 %

Weighted average pay rate 25.35 5.35 5.35 - - 5.35

Fair Value Asset Hedges

Notional amount - forwards $6,787 $- $- $- $- $6,787

Net unrealized gain 3--- -3

Cash Flow Liability Hedges

Notional amount - swaps and options 3$- $1,115 $1,150 $- $- $2,265

Net unrealized gain -2121 - -42

Weighted average receive rate 2- % 5.37 % 5.37 % - % - % 5.37 %

Weighted average pay rate 2- 3.85 4.18 - - 3.98

Fair Value Liability Hedges

Notional amount - swaps $- $173 $1,950 $1,700 $- $3,823

Net unrealized loss - (5) (90) (71) - (166)

Weighted average receive rate 2- % 2.48 % 3.73 % 4.10 % - % 3.84 %

Weighted average pay rate 2- 5.37 5.37 5.37 - 5.37

1Includes only derivative financial instruments which are currently qualifying hedges under SFAS No. 133. Certain other derivatives that are effective for risk management purposes, but which are not in

designated hedging relationships under SFAS No. 133, are not incorporated in this table.

2All interest rate swaps have variable pay or receive rates with resets of six months or less, and are the pay or receive rates in effect at December 31, 2006.

3Includes interest rate swaptions with notional of $0.4 billion and the option to pay a fixed rate of 4.31% beginning May 2007. As the rates on the swaptions were not applicable at December 31, 2006, they

have been excluded from the weighted average pay and receive calculations.

45