Chrysler 2010 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2010 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

|

|

67

For light commercial vehicles, a total of 390,400 units were delivered, representing a 27.1% year-on-year increase. In Europe, Fiat Professional increased

deliveries 19.7% to 183,300 units. In Italy, Fiat Professional achieved a 44.0% market share, gaining approximately 3 percentage points over 2009, while

share in Europe was 12.8% (stable vs. 2009).

In Brazil, Fiat Group Automobiles maintained its leadership position, delivering a total of 761,400 passenger cars and light commercial vehicles,

representing a year-on-year increase of 1.6%. With the overall market growing 10.6%, FGA achieved a 22.8% share for the year (-1.7 percentage points).

For 2010, Maserati reported €586 million in revenues, an increase of 30.8% over 2009, primarily attributable to excellent sales performance for the

new GranCabrio. A total of 5,675 cars were delivered to the network during the year, an increase of 26.4%, with positive performance in the majority of

Maserati’s 59 national markets.

For 2010, Ferrari reported €1,919 million in revenues, up 7.9% over 2009, mainly reflecting higher sales volumes driven by the new 458 Italia and 599 GTO,

the continued success of the Ferrari California, as well as the positive contribution from the customization program. A total of 6,573 cars were delivered to

the network during the year (+5.4% over 2009).

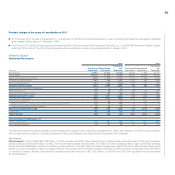

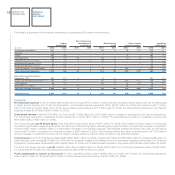

Components and Production Systems

The Components and Production Systems businesses reported revenues of €10,865 million, a 23.6% increase driven primarily by volume growth in

all sectors.

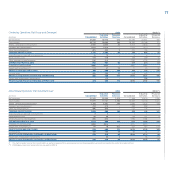

(€ million) 2010 2009 % change

Fiat Powertrain 4,211 3,372 24.9

Components (Magneti Marelli) 5,402 4,528 19.3

Metallurgical Products (Teksid) 776 578 34.3

Production Systems (Comau) 1,023 728 40.5

Eliminations (547) (417) -

Total 10,865 8,789 23.6

For 2010, Fiat Powertrain (the Passenger and Commercial Vehicles business line of the former FPT Powertrain Technologies sector) reported €4,211

million in revenues, an increase of 24.9% over the previous year. This includes the effect of full consolidation of Fiat Powertrain Polska Sp. z.o.o. (formerly

Fiat-GM Powertrain Polska) following acquisition of the JV partner’s 50% stake during the year. On a like-for-like basis, the increase in revenues was

11.1%. Sales to Fiat Group companies accounted for 87% of revenues (90% on a comparable scope of operations and 92% for 2009), with the remainder

primarily consisting of diesel engines sold to external customers. A total of 2,347,000 engines (+2.5% on a like-for-like basis) and 2,233,000 transmissions

(+1.1%) were sold during the year.

Magneti Marelli reported 2010 revenues of €5,402 million, representing a 19.3% increase over 2009. For Europe overall, the increase reflected strong

performance for light commercial vehicles and recovery in the medium-large passenger car segments, which were particularly hard hit in 2009. In Italy and

Poland, revenues reflected the overall decline for A and B-segment cars following the elimination of government eco-incentives. The sector experienced

strong performance in both China and Brazil and a significant recovery in the NAFTA region, where volume growth was primarily driven by new product

launches.

All business lines recorded an increase in production volumes. The Lighting business achieved significant growth linked to the recovery of its core

European markets and volume increases in Asian markets and the NAFTA region. The Suspension Systems business also saw a strong recovery,

with volume increases primarily concentrated in Brazil and the USA. Sales for Electronics Systems were up in China and Brazil, and the Engine Control

business also benefited significantly from performance in those markets.

Teksid reported revenues of €776 million for 2010, up 34.3% principally due to an increase over 2009 volumes, which were severely impacted by the

market crisis. The Cast Iron business unit recorded a 21.8% increase in volumes, driven primarily by growth in components for heavy vehicles, with positive

performance in the Mercosur and NAFTA regions, as well as in Europe. Volumes for the Aluminum business unit were up 15.3%.

Comau had revenues of €1,023 million for 2010, with the 40.5% increase over 2009 principally attributable to operations in China, Latin America and North

America.