Chrysler 2010 Annual Report Download - page 166

Download and view the complete annual report

Please find page 166 of the 2010 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

|

|

165

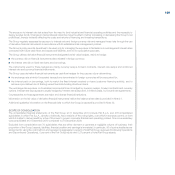

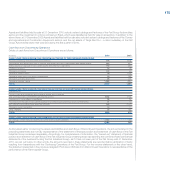

The above changes in accounting principle had the following effects In the current year:

(€ million) 2010

Income statement

Loss recognised for the adjustment to fair value of the previously held equity interest (2)

Other comprehensive income reclassified to the income statement (4)

Increase/(decrease) in profit/(loss) for the year as a result of applying the standard (6)

Other comprehensive income

Increase/(Decrease) in profit/(loss) for the year as a result of applying the standard (6)

Other comprehensive income reclassified to the income statement 4

Increase/(decrease) in other comprehensive income as a result of applying the standard (2)

(in €) 2010

Basic earnings per share

Increase/(decrease) in basic earnings per ordinary share as a result of applying the standard (0.005)

Increase/(decrease) in diluted earnings per ordinary share as a result of applying the standard (0.005)

IAS 27 (2008) – Consolidated and Separate Financial Statements

The revisions to IAS 27 principally affect the accounting for transactions and events that result in a change in the Group’s

interest in its subsidiaries and the attribution of a subsidiary’s losses to non-controlling interests. In accordance with the relevant

transitional provisions, the Group adopted these changes to IAS 27 prospectively. The adoption of the revised standard has

affected the accounting of certain increases and decreases in the Group’s ownership interest in its subsidiaries.

IAS 27 (2008) specifies that once control has been obtained, further transactions whereby the parent entity acquires additional

equity interests from non-controlling interests, or disposes of equity interests without losing control are transactions with

owners and therefore shall be accounted for as equity transactions. It follows that the carrying amounts of the controlling and

non-controlling interests must be adjusted to reflect the changes in their relative interests in the subsidiary and any difference

between the amount by which the non-controlling interest is adjusted and the fair value of the consideration paid or received is

recognised directly in equity and attributed to the owners of the parent. There is no consequential adjustment to the carrying

amount of goodwill and no gain or loss is recognised in profit or loss. Costs associated with these transactions are recognised

in equity in accordance with IAS 32 paragraph 35.

In prior years, in the absence of a specific principle or interpretation, if the Group purchased a non-controlling interest in a

subsidiary that it already controlled it recognised any excess of the acquisition cost over the carrying amount of the assets and

liabilities acquired as goodwill (the “Parent entity extension method”). If it disposed of a non-controlling interest without losing

control, however, the Group recognised any difference between the carrying amount of assets and liabilities of the subsidiary

and the consideration received in profit or loss.

In 2010, following the adoption of the above change, the Group recognised a reduction of €81 million directly in equity in relation

to the exercising of the 5% call option on Ferrari S.p.A., as well as in respect of a series of minor acquisitions and sales of non-

controlling interests in subsidiaries. The adoption of the new standard did not lead to the recognition of significant effects on

Income statements or on basic and diluted earnings per share.