Chrysler 2010 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2010 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

|

|

99

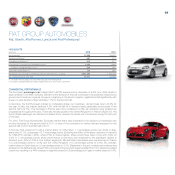

FIAT GROUP AUTOMOBILES

Fiat, Abarth, Alfa Romeo, Lancia and Fiat Professional

HIGHLIGHTS

(€ million) 2010 2009

Net revenues 27,860 26,293

Trading profit/(loss) 607 470

Operating profit/(loss) (*) 515 217

Investments in tangible and intangible assets 1,652 1,495

of which capitalized R&D costs 529 446

Total R&D expenditure (**) 722 669

Passenger cars and light commercial vehicles delivered (no. of units) 2,081,800 2,150,700

No. of employees at year end 57,611 54,038

(*) Includes restructuring costs and other unusual income/(expense)

(**) Includes capitalized R&D and R&D charged directly to the income statement

COMMERCIAL PERFORMANCE

The European passenger car market (EU27+EFTA) experienced a decrease of 4.9% over 2009 levels to

approximately 13.8 million vehicles. Demand in the first part of the year continued to be positively influenced by

government incentive programs. However, beginning in the second quarter, registrations fell significantly with

a year-on-year decline of approximately 11% for the second half.

In Germany, the first European market to completely phase out incentives, demand was down 23.4% for

the year. In Italy, the market declined 9.2%, with the fall off in demand being particularly pronounced in the

second half (-22.7%). The decrease in France was more contained (-2.2%), as incentives were phased out

progressively throughout the year. There was modest growth in the United Kingdom (+1.8%) and Spain (+3.1%)

and in Brazil passenger car demand increased 6.9%, despite the phase out of incentives during the first part

of the year.

For 2010, Fiat Group Automobiles’ European market share was impacted by the decision to reschedule new

product launches for the second half of 2011, in view of the contraction in market demand expected for the

second half of 2010 and first half of 2011.

In Europe, FGA closed 2010 with a market share of 7.5% (down 1.1 percentage points over 2009). In Italy,

share was 30.1%, a decrease of 2.7 percentage points. Excluding the effect of the sharp reduction in demand

for CNG/LPG vehicles (-25%), where FGA is market leader, share would have been in line with 2009. At

3.0% (-1.7 percentage points), share performance in Germany was impacted by the significant decline in

demand (over 40%) in FGA’s core market segments. Modest share decreases were experienced in France

(-0.3 percentage points to 4.0%) and the United Kingdom (-0.5 percentage points to 3.0%). By contrast,

market share in Spain was up 0.5 percentage points to 3.0%. Elsewhere in Europe, notable performance was

achieved in the Netherlands, where FGA’s eco-performing product range benefited from CO2 emissions-based

incentives, resulting in a 44% increase in registrations and a 0.8 percentage point gain in market share to 6.4%.