Reebok 2014 Annual Report Download - page 151

Download and view the complete annual report

Please find page 151 of the 2014 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

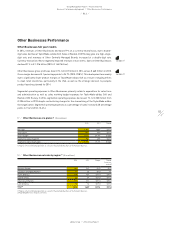

Group Management Report – Financial Review

147

2014

Subsequent Events and Outlook

/

03.4

/

adidas Group

/

2014 Annual Report

Global economy to grow in 2015 1)

Global GDP growth is projected to increase moderately to 3.0% in 2015. At 2.2%, developed economies

are expected to grow slightly faster than last year, supported by improving labour markets and

low financing costs. Growth in developing countries should benefit from the strengthened recovery

in high-income markets and accelerate somewhat in 2015. Oil prices are foreseen to remain

low, encouraging global growth and resulting in more divergent outlooks for oil-exporting and

oil-importing countries.

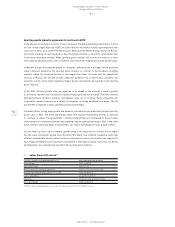

In Western Europe, external demand is likely to improve slightly, and consumer spending is

expected to remain resilient as a result of stronger real wages from declining oil prices. Financial

fragmentation as well as high unemployment and unresolved fiscal challenges in some countries

are forecasted to dampen the recovery. As a result, the region’s GDP is expected to expand at

around the same rate as in the previous year (2014: 1.3%). In Germany, private consumer demand

will prevail as the major driver of growth, which is however projected to be held back by subdued

investment spending.

European emerging markets are expected to grow at a moderate pace of 1.5% in 2015, as persistent

political tensions and uncertainty will slow down investment spending, while further currency

devaluations, high inflationary pressures and low real wages will impact private household demand.

Such a high-risk scenario would particularly affect Russia’s economy, which is forecasted to

contract 3.0% this year.

In the USA, private consumption is projected to remain the major source of growth supported by

declining energy prices. While the strong US dollar will dampen export activity, investment spending

is expected to increase. As a result, the US economy is forecasted to grow 3.2% in 2015.

Asia’s GDP is projected to increase 4.2% in 2015. With the exception of Japan, growth is expected

to remain relatively high during the year, supported by healthy industrial activity, manageable

inflationary pressures and significant wage increases. China should remain the fastest-growing

economy, forecasted to expand 7.3%, with external demand picking up and private consumption

remaining stable. While Japan is predicted to continue to grow at subdued levels, modestly profiting

from low oil prices, India is expected to drive growth through private domestic demand and

strengthened investment.

In Latin America, GDP growth is expected to increase somewhat to 1.2% in 2015, with exports and

investment supporting expansion. Positive performance in several countries will offset the slow

recovery of the largest economies, e.g. Brazil and Argentina, where currency fluctuations and the

unfavourable job market conditions with its negative implications for household consumption will

drive the forecasted decline in economic activity.

1) Sources: World Bank, HSBC Global Research.