Duke Energy 2011 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2011 Duke Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

|

|

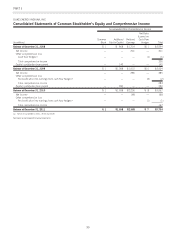

PART II

DUKE ENERGY CORPORATION •DUKE ENERGY CAROLINAS, LLC •DUKE ENERGY OHIO, INC. •DUKE ENERGY INDIANA, INC.

Combined Notes to Consolidated Financial Statements – (Continued)

from continuing operations within operating, investing and financing

cash flows within the Consolidated Statements of Cash Flows. With

respect to cash overdrafts, book overdrafts are included within

operating cash flows while bank overdrafts are included within

financing cash flows.

Dividend Restrictions and Unappropriated Retained Earnings.

Duke Energy does not have any legal, regulatory or other

restrictions on paying common stock dividends to shareholders.

However, as further described in Note 4, due to conditions

established by regulators at the time of the Duke Energy/Cinergy

merger in April 2006, certain wholly-owned subsidiaries, including

the Subsidiary Registrants, have restrictions on paying dividends or

otherwise advancing funds to Duke Energy. At December 31, 2011

and 2010, an insignificant amount of Duke Energy’s consolidated

Retained Earnings balance represents undistributed earnings of equity

method investments.

New Accounting Standards.

The following new accounting standards were adopted by Duke

Energy during the year ended December 31, 2011 and the impact of

such adoption, if applicable has been presented in the accompanying

Consolidated Financial Statements:

Financial Accounting Standards Board (FASB) Accounting

Standards Codification (ASC) 605 — Revenue Recognition. In

October 2009, the FASB issued new revenue recognition accounting

guidance in response to practice concerns related to the accounting

for revenue arrangements with multiple deliverables. This new

accounting guidance primarily applies to all contractual arrangements

in which a vendor will perform multiple revenue generating activities

and addresses the unit of accounting for arrangements involving

multiple deliverables, as well as how arrangement consideration

should be allocated to the separate units of accounting. For the Duke

Energy Registrants, the new accounting guidance was effective

January 1, 2011, and applied on a prospective basis. This new

accounting guidance did not have a material impact to the

consolidated results of operations, cash flows or financial position of

the Duke Energy Registrants.

ASC 805 — Business Combinations. In November 2010, the

FASB issued new accounting guidance in response to diversity in the

interpretation of pro forma information disclosure requirements for

business combinations. The new accounting guidance requires an

entity to present pro forma financial information as if a business

combination occurred at the beginning of the earliest period

presented as well as additional disclosures describing the nature and

amount of material, nonrecurring pro forma adjustments. This new

accounting guidance was effective January 1, 2011, and will be

applied to all business combinations consummated after that date.

ASC 820 — Fair Value Measurements and Disclosures. In

January 2010, the FASB amended existing fair value measurements

and disclosures accounting guidance to clarify certain existing

disclosure requirements and to require a number of additional

disclosures, including amounts and reasons for significant transfers

between the three levels of the fair value hierarchy, and presentation

of certain information in the reconciliation of recurring Level 3

measurements on a gross basis. For the Duke Energy Registrants,

certain portions of this revised accounting guidance were effective on

January 1, 2010, with additional disclosures effective for periods

beginning January 1, 2011. The adoption of this accounting

guidance resulted in additional disclosure in the notes to the

consolidated financial statements but did not have an impact on the

Duke Energy Registrants’ consolidated results of operations, cash

flows or financial position. See Note 15 for additional disclosures

required by the revised accounting guidance in ASC 820.

ASC 350 — Intangibles–Goodwill and Other. In September

2011, the FASB amended existing goodwill impairment testing

accounting guidance to provide an entity testing goodwill for

impairment with the option of performing a qualitative assessment

prior to calculating the fair value of a reporting unit in step one of a

goodwill impairment test. Under this revised guidance, a qualitative

assessment would require an evaluation of economic, industry, and

company-specific considerations. If an entity determines, on a basis

of such qualitative factors, that the fair value of a reporting unit is

more likely than not less than the carrying value of a reporting unit,

the two-step impairment test, as required under pre-existing

applicable accounting guidance, would be required. Otherwise, no

further impairment testing would be required. The revised goodwill

impairment testing accounting guidance is effective for the Duke

Energy Registrants’ annual and interim goodwill impairment tests

performed for fiscal years beginning January 1, 2012, with early

adoption of this revised guidance permitted for annual and interim

goodwill impairment tests performed as of a date before

September 15, 2011. Since annual goodwill impairment tests are

performed by Duke Energy as of August 31, the Duke Energy

Registrants early adopted this revised accounting guidance during the

third quarter of 2011 and applied that guidance to their annual

goodwill impairment tests for 2011.

The following new accounting standards were adopted by Duke

Energy during the year ended December 31, 2010 and the impact of

such adoption, if applicable has been presented in the accompanying

Consolidated Financial Statements:

ASC 860 — Transfers and Servicing. In June 2009, the FASB

issued revised accounting guidance for transfers and servicing of

financial assets and extinguishment of liabilities, to require additional

information about transfers of financial assets, including securitization

transactions, as well as additional information about an enterprise’s

continuing exposure to the risks related to transferred financial assets.

This revised accounting guidance eliminated the concept of a

Qualifying Special Purpose Entity (QSPE) and required those entities

which were not subject to consolidation under previous accounting

rules to now be assessed for consolidation. In addition, this

accounting guidance clarified and amended the derecognition criteria

for transfers of financial assets (including transfers of portions of

108