Duke Energy 2011 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2011 Duke Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

|

|

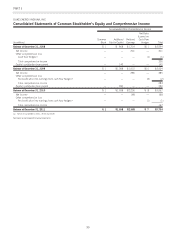

PART II

DUKE ENERGY CORPORATION •DUKE ENERGY CAROLINAS, LLC •DUKE ENERGY OHIO, INC. •DUKE ENERGY INDIANA, INC.

Combined Notes to Consolidated Financial Statements – (Continued)

Operations for the debt component. After construction is completed,

the Duke Energy Registrants are permitted to recover these costs

through inclusion in the rate base and the corresponding depreciation

expense or nuclear fuel expense.

AFUDC equity is recorded in the Consolidated Statements of

Operations and is a permanent difference item for income tax

purposes (i.e., a permanent difference between financial statement

and income tax reporting), thus reducing the Duke Energy

Registrants’ effective tax rate during the construction phase in which

AFUDC equity is being recorded. The effective tax rate is

subsequently increased in future periods when the completed

property, plant and equipment is placed in service and depreciation

of the AFUDC equity commences. See Note 22 for information

related to the impacts of AFUDC equity on the Duke Energy

Registrants’ effective tax rate.

For non-regulated operations, interest is capitalized during the

construction phase in accordance with the applicable accounting

guidance.

Asset Retirement Obligations.

The Duke Energy Registrants recognize asset retirement

obligations for legal obligations associated with the retirement of long-

lived assets that result from the acquisition, construction,

development and/or normal use of the asset, and for conditional asset

retirement obligations. The term conditional asset retirement

obligation refers to a legal obligation to perform an asset retirement

activity in which the timing and (or) method of settlement are

conditional on a future event that may or may not be within the

control of the entity. The obligation to perform the asset retirement

activity is unconditional even though uncertainty exists about the

timing and (or) method of settlement. Thus, the timing and (or)

method of settlement may be conditional on a future event. When

recording an asset retirement obligation, the present value of the

projected liability is recognized in the period in which it is incurred, if

areasonableestimateoffairvaluecanbemade.Thepresentvalueof

the liability is added to the carrying amount of the associated asset.

This additional carrying amount is then depreciated over the

estimated useful life of the asset.

The present value of the initial obligation and subsequent

updates are based on discounted cash flows, which include

estimates regarding the timing of future cash flows, the selection of

discount rates and cost escalation rates, among other factors. These

underlying assumptions and estimates are made as of a point in time

and are subject to change. The obligations for nuclear

decommissioning are based on site-specific cost studies and assume

prompt dismantlement, which reflects dismantling the site after

operations are ceased. The nuclear decommissioning asset retirement

obligation also assumes Duke Energy Carolinas will store spent fuel

on site until such time that it can be transferred to a DOE facility.

SeeNote9forfurtherinformationregardingTheDukeEnergy

Registrants’ asset retirement obligations.

Revenue Recognition and Unbilled Revenue.

Revenues on sales of electricity and gas are recognized when

either the service is provided or the product is delivered. Unbilled

retail revenues are estimated by applying average revenue per

kilowatt-hour or per thousand cubic feet (Mcf) for all customer classes

to the number of estimated kilowatt-hours or Mcfs delivered but not

billed. Unbilled wholesale energy revenues are calculated by applying

the contractual rate per megawatt-hour (MWh) to the number of

estimated MWh delivered but not yet billed. Unbilled wholesale

demand revenues are calculated by applying the contractual rate per

megawatt (MW) to the MW volume delivered but not yet billed. The

amount of unbilled revenues can vary significantly from period to

period as a result of numerous factors, including seasonality,

weather, customer usage patterns and customer mix.

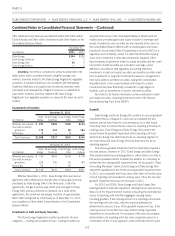

At December 31, 2011 and 2010, the Duke Energy registrants

had unbilled revenues within Restricted Receivables of Variable

Interest Entities and Receivables on their respective Consolidated

Balance Sheets as follows:

(in millions)

December 31,

2011

December 31,

2010

Duke Energy $674 $751

Duke Energy Carolinas 293 322

Duke Energy Ohio(a) 50 54

Duke Energy Indiana 212

(a) Primarily relates to wholesale sales within the Commercial Power segment.

Additionally, Duke Energy Ohio, including Duke Energy

Kentucky, and Duke Energy Indiana sell, on a revolving basis, a

portion of their retail and wholesale accounts receivable to CRC.

These transfers meet sales/derecognition criteria and therefore, Duke

Energy Ohio and Duke Energy Indiana, account for the transfers of

receivables to CRC as sales, and accordingly the receivables sold are

not reflected on the Consolidated Balance Sheets of Duke Energy

Ohio and Duke Energy Indiana. Receivables for unbilled revenues

related to retail and wholesale accounts receivable at Duke Energy

Ohio and Duke Energy Indiana included in the sales of accounts

receivable to CRC at December 31, 2011 and 2010 were as follows:

(in millions)

December 31,

2011

December 31,

2010

Duke Energy Ohio $89 $112

Duke Energy Indiana 115 125

See Note 17 for additional information.

Accounting for Risk Management, Hedging Activities and Financial

Instruments.

The Duke Energy Registrants may use a number of different

derivative and non-derivative instruments in connection with its

commodity price, interest rate and foreign currency risk management

activities, including swaps, futures, forwards and options. All

derivative instruments except for those that qualify for the normal

104