MetLife 2006 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2006 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

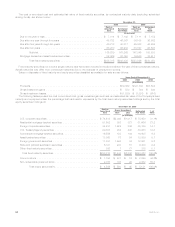

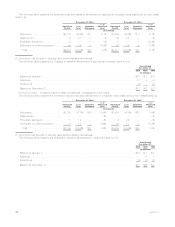

(1) The assets of the asset-backed securitizations and collateralized debt obligations are reflected at fair value at December 31, 2006. The

assets of the real estate joint ventures, other limited partnership interests and other investments are reflected at the carrying amounts at

which such assets would have been reflected on the Company’s balance sheet had the Company consolidated the VIE from the date of its

initial investment in the entity.

(2) The maximum exposure to loss of the asset-backed securitizations and collateralized debt obligations is equal to the carrying amounts of

retained interests. In addition, the Company provides collateral management services for certain of these structures for which it collects a

management fee. The maximum exposure to loss relating to real estate joint ventures, other limited partnership interests and other

investments is equal to the carrying amounts plus any unfunded commitments, reduced by amounts guaranteed by other partners.

(3) Real estate joint ventures include partnerships and other ventures which engage in the acquisition, development, management and

disposal of real estate investments.

(4) Other limited partnership interests include partnerships established for the purpose of investing in public and private debt and equity

securities, as well as limited partnerships.

(5) Other investments include securities that are not asset-backed securitizations or collateralized debt obligations.

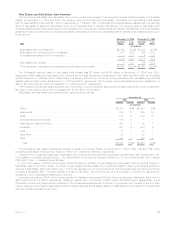

Securities Lending

The Company participates in a securities lending program whereby blocks of securities, which are included in fixed maturity and equity

securities, are loaned to third parties, primarily major brokerage firms. The Company requires a minimum of 102% of the fair value of the

loaned securities to be separately maintained as collateral for the loans. Securities with a cost or amortized cost of $43.3 billion and

$32.1 billion and an estimated fair value of $44.1 billion and $33.0 billion were on loan under the program at December 31, 2006 and 2005,

respectively. Securities loaned under such transactions may be sold or repledged by the transferee. The Company was liable for cash

collateral under its control of $45.4 billion and $33.9 billion at December 31, 2006 and 2005, respectively. Security collateral of $100 million

and $207 million, on deposit from customers in connection with the securities lending transactions at December 31, 2006 and 2005,

respectively, may not be sold or repledged and is not reflected in the consolidated financial statements.

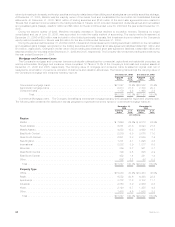

Separate Accounts

The Company had $144.4 billion and $127.9 billion held in its separate accounts, for which the Company does not bear investment risk,

as of December 31, 2006 and 2005, respectively. The Company manages each separate account’s assets in accordance with the

prescribed investment policy that applies to that specific separate account. The Company establishes separate accounts on a single client

and multi-client commingled basis in compliance with insurance laws. Effective with the adoption of SOP 03-1, on January 1, 2004, the

Company reported separately, as assets and liabilities, investments held in separate accounts and liabilities of the separate accounts if:

• such separate accounts are legally recognized;

• assets supporting the contract liabilities are legally insulated from the Company’s general account liabilities;

• investments are directed by the contractholder; and

• all investment performance, net of contract fees and assessments, is passed through to the contractholder.

The Company reports separate account assets meeting such criteria at their fair value. Investment performance (including investment

income, net investment gains (losses) and changes in unrealized gains (losses)) and the corresponding amounts credited to contrac-

tholders of such separate accounts are offset within the same line in the consolidated statements of income.

The Company’s revenues reflect fees charged to the separate accounts, including mortality charges, risk charges, policy administration

fees, investment management fees and surrender charges. Separate accounts not meeting the above criteria are combined on a

line-by-line basis with the Company’s general account assets, liabilities, revenues and expenses.

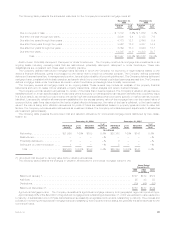

Quantitative and Qualitative Disclosures About Market Risk

The Company must effectively manage, measure and monitor the market risk associated with its invested assets and interest rate

sensitive insurance contracts. It has developed an integrated process for managing risk, which it conducts through its Corporate Risk

Management Department, ALM Committees and additional specialists at the business segment level. The Company has established and

implemented comprehensive policies and procedures at both the corporate and business segment level to minimize the effects of potential

market volatility.

The Company regularly analyzes its exposure to interest rate, equity market and foreign currency exchange risk. As a result of that

analysis, the Company has determined that the fair value of its interest rate sensitive invested assets is materially exposed to changes in

interest rates. The equity and foreign currency portfolios do not expose the Company to material market risk (as described below).

MetLife generally uses option adjusted duration to manage interest rate risk and the methods and assumptions used are generally

consistent with those used by the Company in 2005. The Company analyzes interest rate risk using various models including multi-

scenario cash flow projection models that forecast cash flows of the liabilities and their supporting investments, including derivative

instruments. The Company uses a variety of strategies to manage interest rate, equity market, and foreign currency exchange risk,

including the use of derivative instruments.

Market Risk Exposures

The Company has exposure to market risk through its insurance operations and investment activities. For purposes of this disclosure,

“market risk” is defined as the risk of loss resulting from changes in interest rates, equity market prices and foreign currency exchange

rates.

Interest Rates. The Company’s exposure to interest rate changes results from its significant holdings of fixed maturity securities, as well as its interest

rate sensitive liabilities. The fixed maturity securities include U.S. and foreign government bonds, securities issued by government agencies, corporate bonds

and mortgage-backed securities, all of which are mainly exposed to changes in medium- and long-term treasury rates. The interest rate sensitive liabilities for

purposes of this disclosure include GICs and annuities, which have the same type of interest rate exposure (medium- and long-term treasury rates) as fixed

maturity securities. The Company employs product design, pricing and asset/liability management strategies to reduce the adverse effects of interest rate

movements. Product design and pricing strategies include the use of surrender charges or restrictions on withdrawals in some products. Asset/liability

management strategies include the use of derivatives, the purchase of securities structured to protect against prepayments, prepayment restrictions and

74 MetLife, Inc.