MetLife 2006 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2006 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

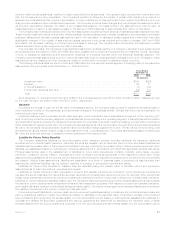

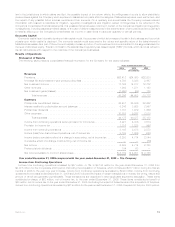

Revenues and Expenses

Premiums, Fees and Other Revenues

Premiums, fees and other revenues increased by $2,595 million, or 9%, to $32,554 million for the year ended December 31, 2006 from

$29,959 million for the comparable 2005 period. Excluding the impact of the acquisition of Travelers, which contributed $946 million during

the first six months of 2006 to the year over year increase, premiums, fees and other revenues increased by $1,649 million.

The following table provides the change in premiums, fees and other revenues by segment, excluding Travelers:

$ Change % Change

(In millions)

Reinsurance...................................................... $ 487 30%

International ...................................................... 469 28

Institutional....................................................... 458 28

Individual........................................................ 229 14

Corporate&Other .................................................. 4 —

Auto&Home ..................................................... 2 —

Totalchange .................................................... $1,649 100%

The growth in the Reinsurance segment was primarily attributable to premiums from new facultative and automatic treaties and renewal

premiums on existing blocks of business in the U.S. and international operations.

The growth in the International segment was primarily due to an increase in Mexico’s premiums, fees and other revenues due to growth

in the business and higher fees, partially offset by an adjustment for experience refunds on a block of business and various one- time other

revenue items in both years. In addition, South Korea’s premiums, fees and other revenues increased due to business growth, as well as

the favorable impact of foreign currency exchange rates. In addition, Brazil’s premiums, fees and other revenues increased due to business

growth and higher bancassurance business, as well as an increase in amounts retained under reinsurance arrangements. Chile’s

premiums, fees and other revenues increased primarily due to higher institutional premiums through its bank distribution channel, partially

offset by lower annuity sales. In addition, business growth in the United Kingdom, Argentina, Australia and Taiwan, as well as the favorable

impact of changes in foreign currency exchange rates, contributed to the increase in the International segment.

The growth in the Institutional segment was primarily due to growth in the dental, disability, accidental death & dismemberment (“AD&D”)

products, as well as growth in the long-term care (“LTC”) and individual disability insurance (“IDI”) businesses, all within the non-medical

health & other business. Additionally, growth in the group life business is attributable to the impact of sales and favorable persistency

largely in the term life business. These increases in the non-medical health & other and group life businesses were partially offset by a

decrease in the retirement & savings business. The decline in retirement & savings was primarily due to a decline in premiums from

structured settlements predominantly due to lower sales, partially offset by an increase in master terminal funding premiums (“MTF”).

The growth in the Individual segment was primarily due to higher fee income from universal life and investment-type products and an

increase in premiums from other life products, partially offset by a decrease in immediate annuity premiums and a decline in premiums

associated with the Company’s closed block business as this business continues to run-off.

Net Investment Income

Net investment income increased by $2,375 million, or 16%, to $17,192 million for the year ended December 31, 2006 from

$14,817 million for the comparable 2005 period. Excluding the impact of the acquisition of Travelers, which contributed $1,473 million

during the first six months of 2006 to the year over year increase, net investment income increased by $902 million of which management

attributes $666 million to growth in the average asset base and $236 million to an increase in yields. This increase was primarily due to an

overall increase in the asset base, an increase in fixed maturity security yields, improved results on real estate and real estate joint

ventures, mortgage loans, and other limited partnership interests, as well as higher short-term interest rates on cash equivalents and short-

term investments. These increases were partially offset by a decline in investment income from securities lending results, and bond and

commercial mortgage prepayment fees.

Interest Margin

Interest margin, which represents the difference between interest earned and interest credited to PABs, decreased in the Institutional

and Individual segments for the year ended December 31, 2006 as compared to the prior year. Interest earned approximates net

investment income on investable assets attributed to the segment with minor adjustments related to the consolidation of certain separate

accounts and other minor non-policyholder elements. Interest credited is the amount attributed to insurance products, recorded in

policyholder benefits, and the amount credited to PABs for investment-type products, recorded in interest credited to PABs. Interest

credited on insurance products reflects the current period impact of the interest rate assumptions established at issuance or acquisition.

Interest credited to PABs is subject to contractual terms, including some minimum guarantees. This tends to move gradually over time to

reflect market interest rate movements and may reflect actions by management to respond to competitive pressures and, therefore,

generally does not introduce volatility in expense.

Net Investment Gains (Losses)

Net investment losses increased by $1,257 million to a loss of $1,350 million for the year ended December 31, 2006 from a loss of

$93 million for the comparable 2005 period. Excluding the impact of the acquisition of Travelers, which contributed a loss of $272 million

during the first six months of 2006 to the year over year increase, net investment losses increased by $985 million. The increase in net

investment losses was due to a combination of losses from the mark-to-market on derivatives and foreign currency transaction losses

during 2006, largely driven by increases in U.S. interest rates and the weakening of the dollar against the major currencies the Company

hedges, notably the euro and pound sterling.

15MetLife, Inc.