MetLife 2006 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2006 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

Management attributed $92 million of this increase to the deferred annuity business and the remainder of $25 million to the other

investment-type products. Interest margin is the difference between interest earned and interest credited to PABs related to the general

account on these businesses. Interest earned approximates net investment income on invested assets attributed to these businesses with

net adjustments for other non-policyholder elements. Interest credited approximates the amount recorded in interest credited to PABs.

Interest credited to PABs is subject to contractual terms, including some minimum guarantees, and may reflect actions by management to

respond to competitive pressures. Interest credited to PABs tends to move gradually over time to reflect market interest rate movements,

subject to any minimum guarantees, and therefore, generally does not introduce volatility in expense.

Fee income from separate account products increased by $126 million, net of income tax, primarily related to growth in the business

and favorable market conditions.

Favorable underwriting results in life products contributed $37 million, net of income tax, to the increase in income from continuing

operations. Underwriting results are generally the difference between the portion of premium and fee income intended to cover mortality,

morbidity or other insurance costs less claims incurred and the change in insurance-related liabilities. Underwriting results are significantly

influenced by mortality, morbidity, or other insurance-related experience trends and the reinsurance activity related to certain blocks of

business and, as a result, can fluctuate from period to period.

The decrease in the closed block-related policyholder dividend obligation of $27 million, net of income tax, lower annuity net

guaranteed benefit costs of $12 million, net of income tax, and lower DAC amortization of $6 million, net of income tax, all contributed

to the increase.

These increases in income from continuing operations were partially offset by lower net investment income on blocks of business that

are not driven by interest margins of $17 million, net of income tax.

Theincreaseinincomefromcontinuingoperationswaspartiallyoffset by higher expenses of $10 million, net of income tax, primarily

due to higher operating costs offset by the impact of revisions to certain expense, premium tax and policyholder liability estimates in the

current year and certain asset write-offs in the prior year.

Additionally, offsetting the increase in income from continuing operations was a revision to the estimate for policyholder dividends of

$9 million, net of income tax, which occurred in the prior year.

The changes in tax rates between years accounted for a decrease in income from continuing operations of $15 million.

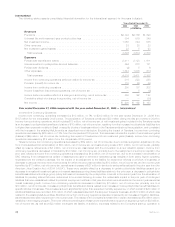

Revenues

Total revenues, excluding net investment gains (losses), increased by $1,532 million, or 12%, to $13,972 million for the year ended

December 31, 2005 from $12,440 million for the comparable 2004 period. The acquisition of Travelers accounted for $975 million of the

increase. Excluding the impact of the acquisition of Travelers, total revenues, excluding net investment gains (losses) increased by

$557 million, or 4%, to $12,997 million for the year ended December 31, 2005 from $12,440 million for the comparable 2004 period.

This increase included higher fee income primarily from variable annuity and universal life products of $239 million resulting from a

combination of growth in the business and improved overall market performance. Policy fees from variable life and annuity and investment-

type products are typically calculated as a percentage of the average assets in policyholder accounts. The value of these assets can

fluctuate depending on equity performance.

In addition, management attributed higher premiums of $170 million in 2005 to the active marketing of income annuity products.

Although premiums associated with the Company’s closed block of business continue to decline, as expected, by $94 million, an increase

in premiums of $130 million from other life products more than offset the decline of the closed block. Included in the premium increase of

the other life products was the impact of growth in the business and a new reinsurance strategy where more business was retained.

Net investment income increased by $111 million. Net investment income from the general account portion of investment-type products

increased by $136 million, which was partially offset by a decrease of $25 million on other businesses. Management attributed $75 million

of this increase to corporate and real estate joint venture income and bond and commercial mortgage prepayment fees partially offset by a

decline in bond yields, as well as $61 million due to growth in the average asset base.

Expenses

Total expenses increased by $881 million, or 8%, to $12,126 million for the year ended December 31, 2005 from $11,245 million for the

comparable 2004 period. The acquisition of Travelers accounted for $761 million of the increase. Excluding the impact from the acquisition

of Travelers, total expenses increased by $120 million, or 1%, to $11,365 million for the year ended December 31, 2005 from

$11,245 million for the comparable 2004 period.

Higher expenses were primarily the result of higher policyholder benefits primarily due to the increase in future policy benefits of

$207 million, commensurate with the net increase in premium on annuity and life products discussed above, partially offset by $5 million

due to better mortality in life products.

Also partially offsetting the increase in policyholder benefits was a reduction in the closed block-related policyholder dividend obligation

of $41 million and a benefit of $18 million associated with the hedging of guaranteed annuity benefit riders. The reduction in the closed

block-related policyholder dividend obligation was driven by lower net investment income, offset by higher realized gains in the closed

block.

Interest credited to PABs decreased by $45 million due primarily to a $41 million decrease on the general account portion of investment-

type products. Management attributed this decrease to lower crediting rates of $91 million partially offset by $50 million solely due to

growth in the average PABs. In addition, total expenses increased by $13 million due to a revision in the estimate of policyholder dividends

in the prior period.

Other expenses increased primarily due to higher corporate incentive expenses of $60 million and higher general spending of

$28 million. The current year included revisions to prior period estimates for certain expense, premium tax and policyholder liabilities which

reduced the current year expenses while the prior period included certain asset write-offs which increased the prior year expenses. The

impact of these two items resulted in a decrease in other expenses of $73 million. Also offsetting the increase in other expenses was lower

DAC amortization of $9 million resulting from net investment losses and adjustments for management’s update of assumptions used to

determine estimated gross margins partially offset by growth in the business.

25MetLife, Inc.