MetLife 2006 Annual Report Download - page 143

Download and view the complete annual report

Please find page 143 of the 2006 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

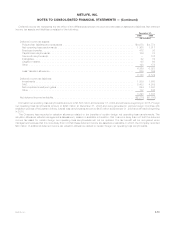

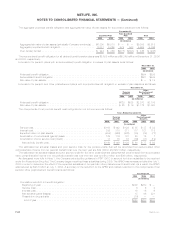

As described more fully in Note 1, effective December 31, 2006, the Company adopted SFAS 158. The adoption of SFAS 158 required

the recognition of the funded status of defined benefit pension and other postretirement plans and eliminated the additional minimum

pension liability provision of SFAS 87. The Company’s additional minimum pension liability was $78 million, and the intangible asset was

$12 million, at December 31, 2005. The excess of the additional minimum pension liability over the intangible asset of $66 million,

$41 million net of income tax, was recorded as a reduction of accumulated other comprehensive income. At December 31, 2006,

immediately prior to adopting SFAS 158, the Company’s additional minimum pension liability was $92 million. The additional minimum

pension liability of $59 million, net of income tax of $33 million, was recorded as a reduction of accumulated other comprehensive income.

The change in the additional minimum pension liability of $18 million, net of income tax, was reflected as a component of comprehensive

income for the year ended December 31, 2006. Upon adoption of SFAS 158, the Company eliminated the additional minimum pension

liability and recognized as an adjustment to accumulated other comprehensive income, net of income tax, those amounts of actuarial gains

and losses, prior service costs and credits, and the remaining net transition asset or obligation that had not yet been included in net

periodic benefit cost at the date of adoption. The following table summarizes the adjustments to the December 31, 2006 consolidated

balance sheet as a result of recognizing the funded status of the defined benefit plans:

Balance Sheet Caption

Pre

SFAS 158

Adjustments

Additional

Minimum

Pension

Liability

Adjustment

Adoption of

SFAS 158

Adjustment

Post

SFAS 158

Adjustments

December 31, 2006

(In millions)

Otherassets:Prepaidpensionbenefitcost .................... $1,937 $— $ (993) $ 944

Otherassets:Intangibleasset............................. $ 12 $(12) $ — $ —

Other liabilities: Accrued pension benefit cost . . . . . . . . . . . . . . . . . . . $ (505) $(14) $ (79) $ (598)

Other liabilities: Accrued other postretirement benefit cost . . . . . . . . . . . $ (802) $ — $ (99) $ (901)

Accumulated other comprehensive income (loss), before income tax:

Definedbenefitplans ................................. $ (66) $(26) $(1,171) $(1,263)

Minorityinterest ...................................... $— $ 8

Deferredincometax ................................... $ 8 $ 419

Accumulated other comprehensive income (loss), net of income tax:

Definedbenefitplans ................................. $ (41) $(18) $ (744) $ (803)

A December 31 measurement date is used for all of the Subsidiaries’ defined benefit pension and other postretirement benefit plans.

F-60 MetLife, Inc.

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)