MetLife 2006 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2006 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

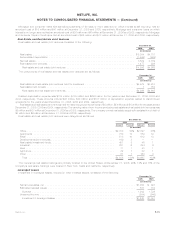

Future Adoption of New Accounting Pronouncements

In February 2007, the FASB issued SFAS No. 159, the Fair Value Option for Financial Assets and Financial Liabilities (“SFAS 159”).

SFAS 159 permits all entities the option to measure most financial instruments and certain other items at fair value at specified election

dates and to report related unrealized gains and losses in earnings. The fair value option will generally be applied on an instrument-by-in-

strument basis and is generally an irrevocable election. SFAS 159 is effective for fiscal years beginning after November 15, 2007. The

Company is evaluating which eligible financial instruments, if any, it will elect to account for at fair value under SFAS 159 and the related

impact on the Company’s consolidated financial statements.

In December 2006, the FASB issued FSP EITF 00-19-2, Accounting for Registration Payment Arrangements (“FSP EITF 00-19-2”). FSP

EITF 00-19-2 specifies that the contingent obligation to make future payments or otherwise transfer consideration under a registration

payment arrangement should be separately recognized and measured in accordance with SFAS No. 5, Accounting for Contingencies. FSP

EITF 00-19-2 is effective immediately for registration payment arrangements and the financial instruments subject to those arrangements

that are entered into or modified subsequent to December 21, 2006. For registration payment arrangements and financial instruments

subject to those arrangements that were entered into prior to December 21, 2006, the guidance in the FSP is effective for fiscal years

beginning after December 15, 2006. The Company does not expect FSP EITF 00-19-2 to have a material impact on the Company’s

consolidated financial statements.

In September 2006, the FASB issued SFAS No. 157, Fair Value Measurements (“SFAS 157”). SFAS 157 defines fair value, establishes a

framework for measuring fair value in GAAP and requires enhanced disclosures about fair value measurements. SFAS 157 does not require

any new fair value measurements. The pronouncement is effective for fiscal years beginning after November 15, 2007. The guidance in

SFAS 157 will be applied prospectively with the exception of: (i) block discounts of financial instruments; and (ii) certain financial and hybrid

instruments measured at initial recognition under SFAS 133 which is to be applied retrospectively as of the beginning of initial adoption (a

limited form of retrospective application). The Company is currently evaluating the impact of SFAS 157 on the Company’s consolidated

financial statements. Implementation of SFAS 157 will require additional disclosures in the Company’s consolidated financial statements.

In July 2006, the FASB issued FSP No. FAS 13-2, Accounting for a Change or Projected Change in the Timing of Cash Flows Relating to

Income Taxes Generated by a Leveraged Lease Transaction (“FSP 13-2”). FSP 13-2 amends SFAS No. 13, Accounting for Leases,to

require that a lessor review the projected timing of income tax cash flows generated by a leveraged lease annually or more frequently if

events or circumstances indicate that a change in timing has occurred or is projected to occur. In addition, FSP 13-2 requires that the

change in the net investment balance resulting from the recalculation be recognized as a gain or loss from continuing operations in the

same line item in which leveraged lease income is recognized in the year in which the assumption is changed. The guidance in FSP 13-2 is

effective for fiscal years beginning after December 15, 2006. The Company does not expect FSP 13-2 to have a material impact on the

Company’s consolidated financial statements.

In June 2006, the FASB issued FIN No. 48, Accounting for Uncertainty in Income Taxes — an interpretation of FASB Statement No. 109

(“FIN 48”). FIN 48 clarifies the accounting for uncertainty in income tax recognized in a company’s financial statements. FIN 48 requires

companies to determine whether it is “more likely than not” that a tax position will be sustained upon examination by the appropriate taxing

authorities before any part of the benefit can be recorded in the financial statements. It also provides guidance on the recognition,

measurement and classification of income tax uncertainties, along with any related interest and penalties. Previously recorded income tax

benefits that no longer meet this standard are required to be charged to earnings in the period that such determination is made. FIN 48 will

also require significant additional disclosures. FIN 48 is effective for fiscal years beginning after December 15, 2006. Based upon the

Company’s evaluation work completed to date, the Company expects to recognize a reduction to the January 1, 2007 balance of retained

earnings of between $35 million and $60 million.

In March 2006, the FASB issued SFAS No. 156, Accounting for Servicing of Financial Assets — an amendment of FASB Statement

No. 140 (“SFAS 156”). Among other requirements, SFAS 156 requires an entity to recognize a servicing asset or servicing liability each time

it undertakes an obligation to service a financial asset by entering into a servicing contract in certain situations. SFAS 156 will be applied

prospectively and is effective for fiscal years beginning after September 15, 2006. The Company does not expect SFAS 156 to have a

material impact on the Company’s consolidated financial statements.

In September 2005, the AICPA issued SOP 05-1, Accounting by Insurance Enterprises for Deferred Acquisition Costs in Connection

with Modifications or Exchanges of Insurance Contracts (“SOP 05-1”). SOP 05-1 provides guidance on accounting by insurance

enterprises for DAC on internal replacements of insurance and investment contracts other than those specifically described in SFAS No. 97,

Accounting and Reporting by Insurance Enterprises for Certain Long-Duration Contracts and for Realized Gains and Losses from the Sale

of Investments. SOP 05-1 defines an internal replacement as a modification in product benefits, features, rights, or coverages that occurs

by the exchange of a contract for a new contract, or by amendment, endorsement, or rider to a contract, or by the election of a feature or

coverage within a contract. It is effective for internal replacements occurring in fiscal years beginning after December 15, 2006.

In addition, in February 2007 related TPAs were issued by the AICPA to provide further clarification of SOP 05-1. The TPAs are effective

concurrently with the adoption of the SOP. Based on the Company’s interpretation of SOP 05-1 and related TPAs, the adoption of SOP 05-1

will result in a reduction to DAC and VOBA relating primarily to the Company’s group life and health insurance contracts that contain certain

rate reset provisions. The Company estimates that the adoption of SOP 05-1 as of January 1, 2007 will result in a cumulative effect

adjustment of between $275 million and $310 million, net of income tax, which will be recorded as a reduction to retained earnings. In

addition, the Company estimates that accelerated DAC and VOBA amortization will reduce 2007 net income by approximately $25 million

to $35 million, net of income tax.

F-22 MetLife, Inc.

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)