MetLife 2006 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2006 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

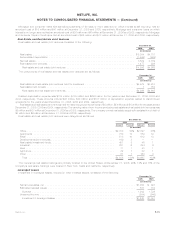

Swaptions are used by the Company primarily to sell, or monetize, embedded call options in its fixed rate liabilities. A swaption is an

optiontoenterintoaswapwithaneffectivedateequaltotheexercisedateoftheembeddedcallandamaturitydateequaltothematurity

date of the underlying liability. The Company receives a premium for entering into the swaption. Swaptions are included in options in the

preceding table.

Equity index options are used by the Company primarily to hedge minimum guarantees embedded in certain variable annuity products

offered by the Company. To hedge against adverse changes in equity indices, the Company enters into contracts to sell the equity index

within a limited time at a contracted price. The contracts will be net settled in cash based on differentials in the indices at the time of

exercise and the strike price. Equity index options are included in options in the preceding table.

The Company enters into financial forwards to buy and sell securities. The price is agreed upon at the time of the contract and payment

for such a contract is made at a specified future date.

Equity variance swaps are used by the Company primarily to hedge minimum guarantees embedded in certain variable annuity products

offered by the Company. In an equity variance swap, the Company agrees with another party to exchange amounts in the future, based on

changes in equity volatility over a defined period. Equity variance swaps are included in financial forwards in the preceding table.

Swap spread locks are used by the Company to hedge invested assets on an economic basis against the risk of changes in credit

spreads. Swap spread locks are forward starting swaps where the Company agrees to pay a coupon based on a predetermined reference

swap spread in exchange for receiving a coupon based on a floating rate. The Company has the option to cash settle with the counterparty

in lieu of maintaining the swap after the effective date. Swap spread locks are included in financial forwards in the preceding table.

Certain credit default swaps are used by the Company to hedge against credit-related changes in the value of its investments and to

diversify its credit risk exposure in certain portfolios. In a credit default swap transaction, the Company agrees with another party, at

specified intervals, to pay a premium to insure credit risk. If a credit event, as defined by the contract, occurs, generally the contract will

require the swap to be settled gross by the delivery of par quantities of the referenced investment equal to the specified swap notional in

exchange for the payment of cash amounts by the counterparty equal to the par value of the investment surrendered.

Credit default swaps are also used to synthetically create investments that are either more expensive to acquire or otherwise

unavailable in the cash markets. These transactions are a combination of a derivative and usually a U.S. Treasury or Agency security.

A synthetic guaranteed interest contract (“GIC”) is a contract that simulates the performance of a traditional GIC through the use of

financial instruments. Under a synthetic GIC, the policyholder owns the underlying assets. The Company guarantees a rate return on those

assets for a premium.

Total rate of return swaps (“TRRs”) are swaps whereby the Company agrees with another party to exchange, at specified intervals, the

difference between the economic risk and reward of an asset or a market index and LIBOR, calculated by reference to an agreed notional

principal amount. No cash is exchanged at the outset of the contract. Cash is paid and received over the life of the contract based on the

terms of the swap. These transactions are entered into pursuant to master agreements that provide for a single net payment to be made by

the counterparty at each due date. TRRs can be used as hedges or to synthetically create investments and are included in the other

classification in the preceding table.

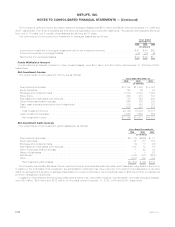

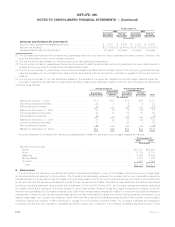

Hedging

The following table presents the notional amounts and fair value of derivatives by type of hedge designation at:

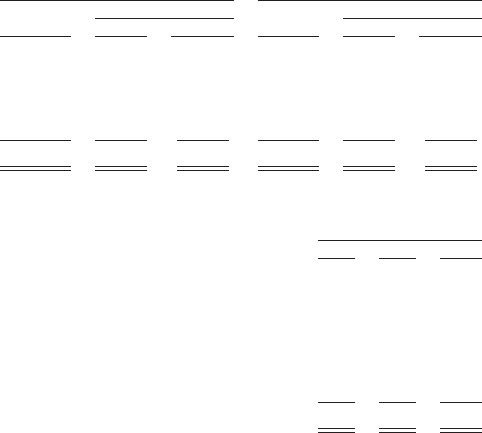

Notional

Amount Assets Liabilities Notional

Amount Assets Liabilities

Fair Value Fair Value

December 31, 2006 December 31, 2005

(In millions)

Fairvalue ................................. $ 7,978 $ 290 $ 85 $ 4,506 $ 51 $ 104

Cashflow ................................. 4,366 149 151 8,301 31 505

Foreignoperations ........................... 1,232 1 50 2,005 13 70

Non-qualifying . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123,203 2,063 1,173 79,528 1,928 502

Total ................................... $136,779 $2,503 $1,459 $94,340 $2,023 $1,181

The following table presents the settlement payments recorded in income for the:

2006 2005 2004

Years Ended

December 31,

(In millions)

Qualifying hedges:

Net investment income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 49 $ 42 $(147)

Interestcreditedtopolicyholderaccountbalances.................................. (35) 17 45

Otherexpenses........................................................ 3 (8) —

Non-qualifying hedges:

Netinvestmentgains(losses) ............................................... 296 86 51

Total.............................................................. $313 $137 $ (51)

Fair Value Hedges

The Company designates and accounts for the following as fair value hedges when they have met the requirements of SFAS 133:

(i) interest rate swaps to convert fixed rate investments to floating rate investments; (ii) foreign currency swaps to hedge the foreign

F-36 MetLife, Inc.

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)