MetLife 2006 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2006 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

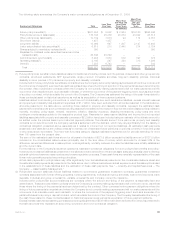

capital and surplus of each of these subsidiaries was in excess of the minimum capital and surplus amounts referenced above, and their

total adjusted capital was in excess of the most recent referenced RBC-based amount calculated at December 31, 2006.

The Holding Company entered into a net worth maintenance agreement with Mitsui Sumitomo MetLife Insurance Company Limited

(“MSMIC”), an investment in Japan of which the Holding Company owns approximately 50% of the equity. Under the agreement, the

Holding Company agreed, without limitation as to amount, to cause MSMIC to have the amount of capital and surplus necessary for MSMIC

to maintain a solvency ratio of at least 400%, as calculated in accordance with the Insurance Business Law of Japan, and to make such

loans to MSMIC as may be necessary to ensure that MSMIC has sufficient cash or other liquid assets to meet its payment obligations as

they fall due. As of the date of the most recent calculation, the capital and surplus of MSMIC was in excess of the minimum capital and

surplus amount referenced above.

In connection with the acquisition of Travelers, MetLife International Holdings, Inc. (“MIH”), a subsidiary of the Holding Company,

committed to the Australian Prudential Regulatory Authority that it will provide or procure the provision of additional capital to MetLife

General Insurance Limited (“MGIL”), an Australian subsidiary of MIH, to the extent necessary to enable MGIL to meet insurance capital

adequacy and solvency requirements. In addition, MetLife International Insurance, Ltd. (“MIIL”), a Bermuda insurance company, was

acquired as part of the Travelers transaction. In connection with the assumption of a block of business by MIIL from a company in liquidation

in 1995, Citicorp Life Insurance Company (“CLIC”), an affiliate of MIIL and a subsidiary of the Holding Company, agreed with MIIL and the

liquidator to make capital contributions to MIIL to ensure that, for so long as any policies in such block remain outstanding, MIIL remains

solvent and able to honor the liabilities under such policies. As a result of the merger of CLIC into Metropolitan Life that occurred in October

2006, this became an obligation of Metropolitan Life. In connection with the acquisition of Travelers, the Holding Company also committed

to the South Carolina Department of Insurance to take necessary action to maintain the minimum capital and surplus of MetLife

Reinsurance Company of South Carolina (“MRSC”), formerly The Travelers Life and Annuity Reinsurance Company, at the greater of

$250,000 or 10% of net loss reserves (loss reserves less DAC).

Management does not anticipate that these arrangements will place any significant demands upon the Company’s liquidity sources.

Litigation. Various litigation, including putative or certified class actions, and various claims and assessments against the Company, in

addition to those discussed elsewhere herein and those otherwise provided for in the Company’s consolidated financial statements, have

arisen in the course of the Company’s business, including, but not limited to, in connection with its activities as an insurer, employer,

investor, investment advisor and taxpayer. Further, state insurance regulatory authorities and other federal and state authorities regularly

make inquiries and conduct investigations concerning the Company’s compliance with applicable insurance and other laws and

regulations.

It is not feasible to predict or determine the ultimate outcome of all pending investigations and legal proceedings or provide reasonable

ranges of potential losses except as noted elsewhere herein in connection with specific matters. In some of the matters referred to herein,

very large and/or indeterminate amounts, including punitive and treble damages, are sought. Although in light of these considerations, it is

possible that an adverse outcome in certain cases could have a material adverse effect upon the Company’s consolidated financial

position, based on information currently known by the Company’s management, in its opinion, the outcome of such pending investigations

and legal proceedings are not likely to have such an effect. However, given the large and/or indeterminate amounts sought in certain of

these matters and the inherent unpredictability of litigation, it is possible that an adverse outcome in certain matters could, from time to

time, have a material adverse effect on the Company’s consolidated net income or cash flows in particular quarterly or annual periods.

Other. Based on management’s analysis of its expected cash inflows from operating activities, the dividends it receives from

subsidiaries, including Metropolitan Life, that are permitted to be paid without prior insurance regulatory approval and its portfolio of

liquid assets and other anticipated cash flows, management believes there will be sufficient liquidity to enable the Company to make

payments on debt, make cash dividend payments on its common and preferred stock, pay all operating expenses, and meet its cash

needs. The nature of the Company’s diverse product portfolio and customer base lessens the likelihood that normal operations will result in

any significant strain on liquidity.

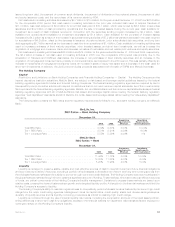

Consolidated Cash Flows. Net cash provided by operating activities decreased by $1.4 billion to $6.6 billion for the year ended

December 31, 2006 from $8.0 billion for the comparable 2005 period. The decrease in operating cash flows is primarily due to reinsurance

receivables related to the sale of certain small market recordkeeping businesses. Partially offsetting the decrease is an increase in

operating cash flows in 2006 over the comparable 2005 period is primarily attributable to the acquisition of Travelers.

Net cash provided by operating activities was $8.0 billion and $6.5 billion for the years ended December 31, 2005 and 2004,

respectively. The $1.5 billion increase in operating cash flows in 2005 over the comparable 2004 period was primarily attributable to the

acquisition of Travelers, growth in disability, dental, LTC business, group life and retirement & savings, as well as continued growth in the

annuity business.

Net cash provided by financing activities increased by $0.9 billion to $15.4 billion for the year ended December 31, 2006 from

$14.5 billion for the comparable 2005 period. Net cash provided by financing activities increased primarily as a result of an increase of

$7.2 billion in the amount of securities lending cash collateral received in connection with the securities lending program, a decrease in

long-term debt repayments of $0.7 billion and an increase of short-term debt borrowings of $0.1 billion. Such increases were offset by

decreases in financing cash flows resulting from a decrease in issuance of preferred stock, junior subordinated debt securities, and long-

term debt aggregating $5.7 billion which were principally used to finance the acquisition of Travelers in 2005 combined with a decrease of

$0.9 billion associated with a decrease in net policyholder account balance deposits and an increase of $0.5 billion of treasury stock

acquired under the share repurchase program which was resumed in the fourth quarter of 2006.

Net cash provided by financing activities was $14.5 billion and $8.3 billion for the years ended December 31, 2005 and 2004,

respectively. The $6.2 billion increase in net cash provided by financing activities in 2005 over the comparable 2004 period was primarily

attributable to the Holding Company’s funding of the acquisition of Travelers through the issuance of long-term debt, junior subordinated

debt securities and preferred shares. In addition, there was an increase in the amount of securities lending cash collateral invested in

connection with the program. This increase was partially offset by a decrease in net cash provided by PABs, the repayment of previously

42 MetLife, Inc.