MetLife 2006 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2006 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

issued long-term debt, the payment of common stock dividends, the payment of dividends on the preferred shares, the payment of debt

and equity issuance costs, and the repurchase of its common stock by RGA.

Net cash used in investing activities decreased by $3.7 billion to $18.9 billion for the year ended December 31, 2006 from $22.6 billion

for the comparable 2005 period. Net cash used in investing activities in the prior year included cash used to acquire Travelers of

$11.0 billion, less cash acquired of $0.9 billion for a net total cash paid of $10.1 billion, which was funded by $6.8 billion in securities

issuances and $4.2 billion of cash provided by operations and the sale of invested assets. During the current year, cash available for

investment as a result of cash collateral received in connection with the securities lending program increased by $7.2 billion. Cash

available from operations and available for investment decreased by $1.4 billion. Cash available for the purchase of invested assets

increased by $4.3 billion as a result of the increase in securities lending activities of $7.2 billion as well as a decrease in the cash required

for acquisitions of $4.2 billion, offset by the decrease in issuance of preferred stock, junior subordinated debt securities, and long-term

debt aggregating $5.7 billion as well as the decrease in cash flow from operations of $1.4 billion. Cash available for investing activities was

used to increase purchases of fixed maturity securities, other invested assets, and short-term investments, as well as increase the

origination of mortgage and consumer loans and decrease net sales of real estate and real estate joint ventures and equity securities.

Net cash used in investing activities was $22.6 billion and $14.4 billion for the years ended December 31, 2005 and 2004, respectively.

The $8.2 billion increase in net cash used in investing activities in 2005 over the comparable 2004 period was primarily due to the

acquisition of Travelers and CitiStreet Associates, the increase in net purchases of fixed maturity securities and an increase in the

origination of mortgage and consumer loans, primarily in commercial loans, as compared to the 2004 period. This was partially offset by an

increase in repayments of mortgage and consumer loans, an increase in sales of equity real estate and a decrease in the cash used for

short-term investments. In addition, the 2005 period includes proceeds associated with the sale of SSRM and MetLife Indonesia.

The Holding Company

Capital

Restrictions and Limitations on Bank Holding Companies and Financial Holding Companies — Capital. The Holding Company and its

insured depository institution subsidiary, MetLife Bank, are subject to risk-based and leverage capital guidelines issued by the federal

banking regulatory agencies for banks and financial holding companies. The federal banking regulatory agencies are required by law to

take specific prompt corrective actions with respect to institutions that do not meet minimum capital standards. As of their most recently

filed reports with the federal banking regulatory agencies, MetLife, Inc. and MetLife Bank met the minimum capital standards as per federal

banking regulatory agencies with all of MetLife Bank’s risk-based and leverage capital ratios meeting the federal banking regulatory

agencies’ “well capitalized” standards and all of MetLife, Inc.’s risk-based and leverage capital ratios meeting the “adequately capitalized”

standards.

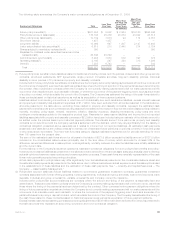

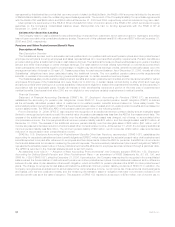

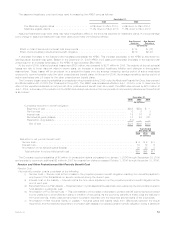

The following table contains the RBC ratios and the regulatory requirements for MetLife, Inc., as a bank holding company, and MetLife

Bank:

MetLife, Inc.

RBC Ratios — Bank Holding Company

2006 2005

Regulatory

Requirements

Minimum

Regulatory

Requirements

“Well Capitalized”

December 31,

TotalRBCRatio.................................. 9.89% 9.57% 8.00% 10.00%

Tier1RBCRatio................................. 9.51% 9.21% 4.00% 6.00%

Tier1LeverageRatio.............................. 5.55% 5.39% 4.00% n/a

MetLife Bank

RBC Ratios — Bank

2006 2005

Regulatory

Requirements

Minimum

Regulatory

Requirements

“Well Capitalized”

December 31,

TotalRBCRatio................................ 11.44% 11.78% 8.00% 10.00%

Tier1RBCRatio ............................... 10.88% 11.22% 4.00% 6.00%

Tier1LeverageRatio ............................ 5.98% 5.96% 4.00% 5.00%

Liquidity

Liquidity is managed to preserve stable, reliable and cost-effective sources of cash to meet all current and future financial obligations

and is provided by a variety of sources, including a portfolio of liquid assets, a diversified mix of short- and long-term funding sources from

the wholesale financial markets and the ability to borrow through committed credit facilities. The Holding Company is an active participant in

the global financial markets through which it obtains a significant amount of funding. These markets, which serve as cost-effective sources

of funds, are critical components of the Holding Company’s liquidity management. Decisions to access these markets are based upon

relative costs, prospective views of balance sheet growth and a targeted liquidity profile. A disruption in the financial markets could limit the

Holding Company’s access to liquidity.

The Holding Company’s ability to maintain regular access to competitively priced wholesale funds is fostered by its current high credit

ratings from the major credit rating agencies. Management views its capital ratios, credit quality, stable and diverse earnings streams,

diversity of liquidity sources and its liquidity monitoring procedures as critical to retaining high credit ratings.

Liquidity is monitored through the use of internal liquidity risk metrics, including the composition and level of the liquid asset portfolio,

timing differences in short-term cash flow obligations, access to the financial markets for capital and debt transactions and exposure to

contingent draws on the Holding Company’s liquidity.

43MetLife, Inc.