MetLife 2006 Annual Report Download - page 153

Download and view the complete annual report

Please find page 153 of the 2006 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

-

165

-

166

|

|

determined by the product of the initial target multiplied by a factor of 0.0 to 2.0. The factor applied is based on measurements of the

Holding Company’s performance with respect to: (i) the change in annual net operating earnings per share, as defined; and (ii) the

proportionate total shareholder return, as defined, with reference to the three-year performance period relative to other companies in the

S&P Insurance Index with reference to the same three-year period. Performance Share awards will normally vest in their entirety at the end

of the three-year performance period (subject to certain contingencies) and will be payable entirely in shares of the Holding Company’s

common stock.

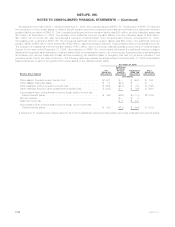

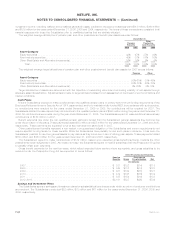

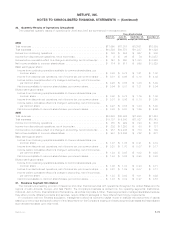

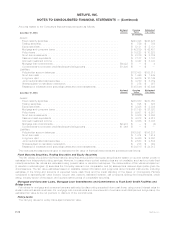

The following is a summary of Performance Share activity for the year ended December 31, 2006:

Performance

Shares

Weighted Average

Grant Date

Fair Value

Outstanding at January 1, 2006 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,029,700 $36.87

Granted........................................................ 884,875 $48.43

Forfeited ....................................................... (65,000) $41.37

Outstanding at December 31, 2006 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,849,575 $42.24

Performance Shares expected to vest at December 31, 2006 . . . . . . . . . . . . . . . . . . . . . . 1,820,742 $42.16

Performance Share amounts above represent aggregate initial target awards and do not reflect potential increases or decreases

resulting from the final performance factor to be determined at the end of the respective performance period. None of the Performance

Shares vested during the year ended December 31, 2006.

Performance Share awards are accounted for as equity awards but are not credited with dividend-equivalents for actual dividends paid

on the Holding Company’s common stock during the performance period. Accordingly, the fair value of Performance Shares is based upon

the closing price of the Holding Company’s common stock on the date of grant, reduced by the present value of estimated dividends to be

paid on that stock during the performance period.

Compensation expense related to initial Performance Shares granted prior to January 1, 2006 and expected to vest is recognized

ratably during the performance period. Compensation expense related to initial Performance Shares granted on or after January 1, 2006

and expected to vest is recognized ratably over the performance period or the period to retirement eligibility, if shorter. Performance Shares

expected to vest and the related compensation expenses may be further adjusted by the performance factor most likely to be achieved, as

estimated by management, at the end of the performance period. Compensation expense of $74 million and $24 million, related to

Performance Shares was recognized for the years ended December 31, 2006 and 2005, respectively.

As of December 31, 2006, there was $59 million of total unrecognized compensation costs related to Performance Share awards. It is

expected that these costs will be recognized over a weighted average period of 1.59 years.

Long-Term Performance Compensation Plan

Prior to January 1, 2005, the Company granted stock-based compensation to certain members of management under the LTPCP. Each

participant was assigned a target compensation amount (an “Opportunity Award”) at the inception of the performance period with the final

compensation amount determined based on the total shareholder return on the Holding Company’s common stock over the three-year

performance period, subject to limited further adjustment approved by the Holding Company’s Board of Directors. Payments on the

Opportunity Awards are normally payable in their entirety (subject to certain contingencies) at the end of the three-year performance period,

and may be paid in whole or in part with shares of the Holding Company’s common stock, as approved by the Holding Company’s Board of

Directors. There were no new grants under the LTPCP during the years ended December 31, 2006 and 2005.

A portion of each Opportunity Award under the LTPCP is expected to be settled in shares of the Holding Company’s common stock

while the remainder will be settled in cash. The portion of the Opportunity Award expected to be settled in shares of the Holding Company’s

common stock is accounted for as an equity award with the fair value of the award determined based upon the closing price of the Holding

Company’s common stock on the date of grant. The compensation expense associated with the equity award, based upon the grant date

fair value, is recognized into expense ratably over the respective three-year performance period. The portion of the Opportunity Award

expected to be settled in cash is accounted for as a liability and is remeasured using the closing price of the Holding Company’s common

stock on the final day of each subsequent reporting period during the three-year performance period.

Compensation expense of $14 million, $46 million and $49 million, related to LTPCP Opportunity Awards was recognized for the years

ended December 31, 2006, 2005 and 2004, respectively.

The aggregate fair value of LTPCP Opportunity Awards outstanding at December 31, 2006 was $41 million, all of which has been

recognized. LTPCP Opportunity Awards with an aggregate fair value of $65 million vested during the year ended December 31, 2006, and

settled in the form of 906,989 shares and $16 million in cash. It is expected that approximately 760,000 additional shares and $15 million in

cash will be issued in future settlement of LTPCP Opportunity Awards expected to become payable in the second quarter of 2007.

StatutoryEquityandIncome

Each insurance company’s state of domicile imposes minimum risk-based capital (“RBC”) requirements that were developed by the

National Association of Insurance Commissioners (“NAIC”). The formulas for determining the amount of RBC specify various weighting

factors that are applied to financial balances or various levels of activity based on the perceived degree of risk. Regulatory compliance is

determined by a ratio of total adjusted capital, as defined by the NAIC, to authorized control level RBC, as defined by the NAIC. Companies

below specific trigger points or ratios are classified within certain levels, each of which requires specified corrective action. Each of the

Holding Company’s U.S. insurance subsidiaries exceeded the minimum RBC requirements for all periods presented herein.

The NAIC adopted the Codification of Statutory Accounting Principles (“Codification”) in 2001. Codification was intended to standardize

regulatory accounting and reporting to state insurance departments. However, statutory accounting principles continue to be established

F-70 MetLife, Inc.

METLIFE, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)