Chrysler 2012 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2012 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

|

|

67

Report on Operations

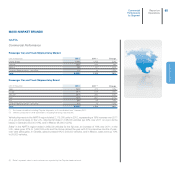

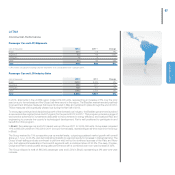

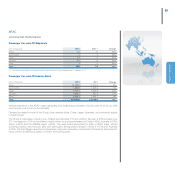

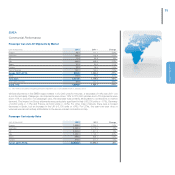

LATAM

Commercial Performance

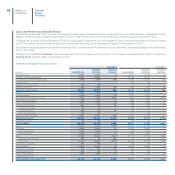

Passenger Car and LCV Shipments

(units in thousands) 2012 2011 (*) Change

Brazil 845 778 9%

Argentina 84 98 -15%

Venezuela 99 -

Other 41 43 -5%

Total 979 929 5%

(*) Pro-forma calculation including Chrysler shipments as if consolidated from 1 January 2011.

Passenger Car and LCV Industry Sales

(units in thousands) 2012 2011 Change

Brazil 3,635 3,426 6%

Argentina 805 817 -1%

Venezuela 108 101 7%

Other 1,295 1,243 4%

Total 5,843 5,587 5%

In 2012, shipments in the LATAM region totaled 979,000 units, representing an increase of 5% over the prior

year (on a pro-forma basis) and the Group’s all-time record in the region. The Brazilian market reacted positively

to government stimulus measures that were introduced in May and remained in place through the end of 2012.

Those measures will be gradually phased out during the first half of 2013.

To encourage continued and disciplined growth of the domestic car industry, the Brazilian government launched

a new automotive regime (Inovar Auto Program) for the period 2013 to 2017. This program provides a range of

tax incentive schemes for investments dedicated to improvements in energy efficiency and localized R&D and

engineering to promote the country’s technological development. Fiat is well positioned to participate in and

benefit from this program.

In Brazil, the passenger car and LCV market was up 6% over 2011 to 3,635,000 units. Group sales increased

11% to 845,000 units from 760,000 in 2011 (on a pro-forma basis), representing an all-time record for the Group

in Brazil.

The Group marked its 11th consecutive year as market leader, outpacing sustained market growth with overall

share up 1.1 p.p. to 23.3%, and demonstrating its ability to respond rapidly to increases in market demand. The

Group’s best-selling products continued to perform well, led by the continued success of the Palio and Novo

Uno. Fiat retained its leadership in the A and B segments with a combined share of 30.2%. The Jeep, Chrysler,

Dodge and Ram brands posted strong sales performance with a combined year-over-year increase of 32%.

The Group shipped a total of 845,000 passenger cars and LCVs in Brazil, representing a 9% year-over-year

increase.