Chrysler 2012 Annual Report Download - page 260

Download and view the complete annual report

Please find page 260 of the 2012 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

|

|

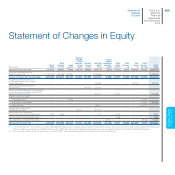

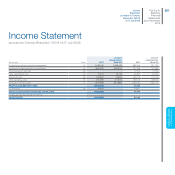

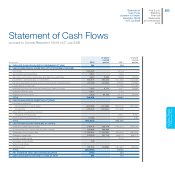

259

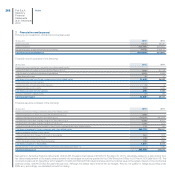

Fiat S.p.A. - Statutory

Financial Statements

at 31 December 2012

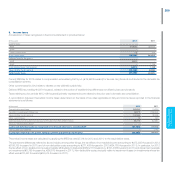

if it neither transfers nor retains substantially all the risks and rewards of ownership of the receivable, it determines whether it has

retained control of the receivable. In this case:

if the Company has not maintained control, it derecognizes the receivable and recognizes separately as assets and liabilities any

rights and obligations created or retained in the transfer

if the Company has retained control, it continues to recognize the receivable to the extent of its continuing involvement in the

receivable

On derecognition of a receivable, the difference between the carrying amount of the receivable and the consideration received or

receivable for the transfer of the receivable is recognized in profit or loss.

Assets held for sale

This item includes non-current assets (or assets included in disposal groups) whose carrying amount will be recovered principally

through a sale transaction rather than through continuing use. Assets held for sale (or disposal groups) are measured at the lower of

their carrying amount and fair value less disposal costs.

Employee benefits

Post-employment benefit plans

The Company provides pension plans and other post-employment benefit plans to its employees. Pension plans in which the Company

is obliged to participate under Italian law are defined contribution plans, while other post-employment benefit plans, in which the

Company’s participation is generally subject to collective bargaining agreements, are defined benefit plans. Costs associated with

payments to defined contribution plans are recognized in the income statement when incurred. Defined benefit plans are based on an

employee’s working life and on the salary or wage received by the employee over a predetermined period of service.

Until 31 December 2006, the leaving entitlement payable to employees of Group companies in Italy (Trattamento di Fine Rapporto or

“TFR”) qualified as a defined benefit plan. Legislation relating to TFR was amended by Law 296 of 27 December 2006 and subsequent

decrees and regulations issued in the first half of 2007. As a result of those changes, and specifically with regard to companies with 50

employees or more, TFR is only considered a defined benefit plan for benefits accrued prior to 1 January 2007 (and not yet paid out as

at the balance sheet date), while benefits accruing after that date are classified as defined contributions.

The Company’s obligation to fund defined benefit plans and the associated annual cost recognized in the income statement are

determined on an actuarial basis using the projected unit credit method. The portion of net cumulative actuarial gains and losses which

exceeds the greater of 10% of the present value of the defined benefit obligation and 10% of the fair value of the plan assets at the

end of the previous year is amortized over the average remaining service lives of employees (the “corridor approach”). The portion of

actuarial gains and losses that does not exceed this threshold is deferred.

Upon first-time adoption of IFRS, the Company elected to recognize all cumulative actuarial gains and losses existing at 1 January

2004, despite having elected the corridor approach for recognition of subsequent actuarial gains and losses.

For defined benefit plans, any costs associated with the increase in present value of the liability nearer to the payment date are

recognized under financial expense.

Liabilities associated with defined benefit plans are recognized in the statement of financial position at their present value adjusted

for unrecognized actuarial gains and losses, arising from application of the corridor approach, and unrecognized past service costs.

Other long-term employee benefits

The accounting treatment for other long-term benefits is the same as for post-employment benefit plans except that actuarial gains and

losses and past service costs are fully recognized in the income statement in the year in which they arise and the corridor approach is

not applied.