Chrysler 2012 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2012 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

|

|

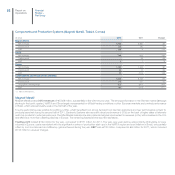

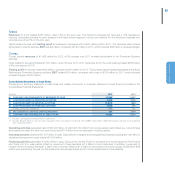

43

Report on Operations

The rating agencies review their ratings at least annually and, as such, the assignment of new ratings to Fiat during 2013 cannot be

excluded. It is not currently possible to predict the timing or outcome of any rating review. Any further downgrade may increase Fiat’s

cost of capital and potentially limit its access to sources of financing with a consequent material adverse effect on Fiat’s business

prospects, financial condition and results of operations.

Chrysler has been assigned a corporate credit rating of B1 (with a stable outlook) by Moody’s Investors Service and B+ (with a stable

outlook) by Standard & Poor’s Ratings Services. Because Chrysler has a lower corporate credit rating than Fiat, it is possible that further

integration between Fiat and Chrysler could result in a rating review of Fiat and potentially a lower credit rating.

Risks associated with restrictions arising out of Chrysler’s debt instruments

In connection with the refinancing transactions finalized at the end of May 2011, Chrysler entered into a credit agreement for the senior

secured credit facilities (including a revolving facility) and an indenture for two series of secured senior notes. These debt instruments

include covenants that restrict Chrysler’s ability to make certain distributions, prepay other debt, encumber assets, incur additional

indebtedness, engage in certain business combinations, or undertake various other business activities.

The credit agreement governing the senior secured credit facility and the indenture governing the secured senior notes contain restrictive

covenants that limit Chrysler’s ability to, among other things:

incur or guarantee additional secured indebtedness;

pay dividends or make distributions or purchase or redeem capital stock;

make certain other restricted payments;

incur liens;

transfer and sell assets;

enter into sale and lease-back transactions;

enter into transactions with affiliates (as defined in the relevant contractual documents), including Fiat; and

effect a consolidation, amalgamation or certain merger or change of control (except for the acquisition of control by Fiat).

These restrictive covenants could have an adverse effect on Chrysler’s business by limiting its ability to take advantage of financing,

mergers and acquisitions, joint ventures or other corporate opportunities. In addition, the Senior Credit Facilities contain, and future

indebtedness may contain, other and more restrictive covenants and also prohibit Chrysler from prepaying certain of its indebtedness.

The Senior Credit Facilities require Chrysler to maintain borrowing base collateral coverage and a liquidity threshold. A breach of any of

these covenants or restrictions could result in an event of default on the indebtedness and any of the other indebtedness of Chrysler or

result in cross-default under certain of its indebtedness.

Furthermore, the indenture governing the VEBA Trust Note limits the ability of Chrysler’s subsidiaries to incur debt.

If Chrysler is unable to comply with all of these covenants, it may be in default, which could result in the acceleration of its outstanding

indebtedness and foreclosure on mortgaged properties. In this case, Chrysler may not be able to repay its debt and it is unlikely

that it would be able to borrow sufficient additional funds. In any case, even if new financing is made available to Chrysler in such

circumstances, it may not be available on acceptable terms.

In addition, compliance with certain of these covenants could restrict Chrysler’s ability to take certain actions that its management

believes are in Chrysler’s best long-term interests.

Should Chrysler be unable to undertake strategic initiatives due to the covenants provided for by the above instruments, Fiat’s business

prospects, financial condition and results of operations could be adversely affected.