Chrysler 2012 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2012 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

|

|

42

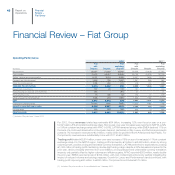

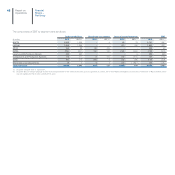

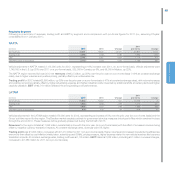

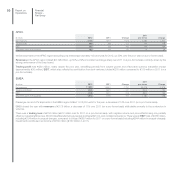

Risks associated with environmental and other government regulation

The Group’s products and activities are subject to numerous environmental laws and regulations (local, national and international) which

are becoming increasingly stringent in many countries in which it operates (particularly in the European Union). Such regulations govern,

among other things, products – with requirements relating to emissions of polluting gases, reduced fuel consumption and safety

becoming increasingly strict – and industrial plants – with requirements for emissions, treatment of waste and water and prohibitions

on soil contamination. In order to comply with such laws and regulations, the Group employs considerable resources and expects it will

continue to incur substantial costs in the future.

In addition, government initiatives to stimulate consumer demand for products sold by the Group, such as changes in tax treatment

or purchase incentives for new vehicles, can substantially influence the timing and level of revenues. The size and duration of such

government measures are unpredictable and outside of the Group’s control. Any adverse change in government policy relating to those

measures could have material adverse effects on the Group’s business prospects, earnings and financial position.

Risks associated with management

The Group’s success is largely dependent on the ability of its senior executives and other members of management to effectively

manage the Group and individual areas of business. The loss of any senior executive, manager or other key employees without an

adequate replacement or the inability to attract, retain and incentivize senior executive managers, other key employees or new qualified

personnel could therefore have a material adverse effect on the Group’s business prospects, earnings and financial position.

Risks associated with financing requirements

The Group’s future performance will depend on, among other things, its ability to finance debt repayment obligations and planned

investments from operating cash flow, available liquidity, the renewal or refinancing of existing bank loans and facilities and possible

recourse to capital markets or other sources of financing. Although the Group has measures in place that are designed to ensure levels

of working capital and liquidity are maintained, further declines in sales volumes could have a negative impact on the cash-generating

capacity of its operating activities. The Group could, therefore, find itself in the position of having to seek additional financing and/or

having to refinance existing debt, including in unfavorable market conditions with limited availability of funding and a general increase

in funding costs. Any difficulty in obtaining financing could have material adverse effects on the Group’s business prospects, earnings

and financial position.

Risks associated with Fiat indebtedness as a result of the acquisition of control of Chrysler

Even after the acquisition of control by Fiat, Chrysler continues to manage financial matters, including funding and cash management,

separately. Additionally, Fiat has not provided guarantees or security or undertaken any other similar commitment in relation to any

financial obligation of Chrysler, nor does it have any commitment to provide funding to Chrysler in the future.

In any case, certain bonds issued by Fiat include provisions that may be affected by circumstances related to Chrysler. In particular

these bonds include cross-default clauses which may accelerate Fiat’s obligation to repay its bonds in the event that a “material

subsidiary” of Fiat fails to pay certain debt obligations on maturity or is otherwise subject to an acceleration in the maturity of any of

its obligations. As a result of Fiat’s acquisition of control over Chrysler, Chrysler Group LLC is a “material subsidiary” and certain of its

subsidiaries may become material subsidiaries of Fiat within the meaning of those bonds. Therefore, the cross-default provision could

require early repayment of the Fiat bonds in the event Chrysler’s debt obligations are accelerated or are not repaid at maturity. There

can be no assurance that the obligation to accelerate the repayment by Chrysler of its debts will not arise or that it will be able to pay

its debt obligations when due at maturity.

Risks associated with Fiat’s credit rating

The ability to access the capital markets or other forms of financing and the related costs are dependent, amongst other things,

on the Group’s credit ratings. Following downgrades by the major rating agencies, Fiat is currently rated below investment grade,

with corporate credit ratings of Ba3 (being B1 the senior unsecured rating) with negative outlook from Moody’s Deutschland GmbH

(“Moody’s”) , BB- with a stable outlook from Standard & Poor’s Credit Market Services Italy S.r.l. (“S&P”), and BB with negative outlook

from Fitch Ratings España S.A.U. (“Fitch”).

Main Risks and

Uncertainties to

which Fiat S.p.A.

and its Subsidiaries

are Exposed

Report on

Operations