Chrysler 2012 Annual Report Download - page 139

Download and view the complete annual report

Please find page 139 of the 2012 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

|

|

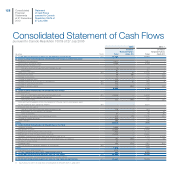

Notes

138 Consolidated

Financial

Statements

at 31 December

2012

If changes are made to a plan that alter the benefits due for past service or if a new plan is introduced regarding past service then past

service costs are recognised in profit or loss on a straight-line basis over the average period remaining until the benefits vest. If a change

is made to a plan that significantly reduces the number of employees who are members of the plan or that alters the conditions of the

plan such that employees will no longer be entitled to the same benefits for a significant part of their future service, or if such benefits

will be reduced, the profit or loss arising from such changes is immediately recognised in the income statement.

All other costs and income arising from the measurement of pension plan provisions are allocated by function in the income statement,

except for interest cost on unfunded defined benefit plans which is reported as part of financial expenses.

Costs arising from defined contribution plans are recognised as an expense as incurred.

Share-based compensation plans

Share-based compensation plans that may be settled by the delivery of shares are measured at fair value at the grant date. This

fair value is expensed over the vesting period of the benefit with a corresponding increase in equity. Periodically, the Group reviews

its estimate of the benefits expected to vest through the plan and recognises any difference in estimate in profit or loss, with a

corresponding increase or decrease in equity.

Share-based compensation plans that may be settled in cash or by the delivery of other financial assets are recognised as a liability

and measured at fair value at the end of each reporting period and when settled. Any subsequent changes in fair value are recognised

in profit or loss.

Provisions

The Group records provisions when it has an obligation, legal or constructive, to a third party, when it is probable that an outflow of

Group resources will be required to satisfy the obligation and when a reliable estimate of the amount can be made.

Changes in estimates are reflected in the income statement in the period in which the change occurs.

Treasury shares

Treasury shares are presented as a deduction from equity. The original cost of treasury shares and the proceeds of any subsequent

sale are presented as movements in equity.

Revenue recognition

Revenue is recognised if it is probable that the economic benefits associated with a transaction will flow to the Group and the revenue

can be measured reliably. Revenues are stated net of discounts, allowances, settlement discounts and rebates, as well as costs for

sales incentive programs, determined on the basis of historical costs, country by country, and charged against profit for the period

in which the corresponding sales are recognised. The Group’s sales incentive programs include the granting of retail financing at

significant discount to market interest rates. The corresponding cost is recognised at the time of the initial sale.

Revenues from the sale of products are recognised when the risks and rewards of ownership of the goods are transferred to the

customer, the sales price is agreed or determinable and receipt of payment can be assumed; this corresponds generally to the date

when the vehicles are made available to non-group dealers, or the delivery date in the case of direct sales. New vehicle sales with a

buy-back commitment are not recognised at the time of delivery but are accounted for as operating leases when it is probable that

the vehicle will be bought back. More specifically, vehicles sold with a buy-back commitment are accounted for as Inventories. The

difference between the carrying amount (corresponding to the manufacturing cost) and the estimated resale value (net of reconditioning

costs) at the end of the buy-back period is recognised on the income statement on a straight-line basis over the contract term. The

initial sale price received is recognised in liabilities as a down payment. The difference between the initial sale price and the buy-back

price is recognised as rental revenue on a straight-line basis over the term of the operating lease. The proceeds from the sale of such

assets are recognised as Revenues.

Revenues from services and from construction contracts are recognised by reference to the stage of completion.

Revenues also include lease rentals and interest income from financial services companies.