Chrysler 2012 Annual Report Download - page 263

Download and view the complete annual report

Please find page 263 of the 2012 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

|

|

Fiat S.p.A.

Statutory

Financial

Statements

at 31 December

2012

Notes

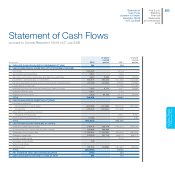

262

As the cash flows are assumed equivalent to expected net profit, the discount rates applied are based on the estimated cost of equity.

Different and increasing rates were applied over the specific cash flow projection period (2013-2018) to reflect the level of risk associated

with achieving targets and with the geographic distribution of earnings. The weighted average discount rate for the projection period

ranged from 10.0-13.0% for EMEA, 14.7-17.7% for LATAM, and 12.2-14.7% for Chrysler. For the terminal value, the weighted average

discount rate was 13.7%, which prudently includes a 3% premium to reflect the execution risks associated with achieving targets. A

change of 50 basis points in the discount rate would impact the value in use of the investment by approximately €500 million.

The estimates and assumptions made, in addition to the analysis based on historic and prospective P/E multiples for comparable listed

companies used as a control, provide reasonable support for maintaining the carrying amounts recognized for the investment in FGA

unchanged at 31 December 2012.

Accounting standards, amendments and interpretations adopted from 1 January 2012

On 7 October 2010, the IASB issued amendments to IFRS 7 – Financial Instruments: Disclosures that were adopted by the Company

from 1 January 2012. The amendments allow users of financial statements to improve their understanding of transfers of financial

assets (“derecognition”), including understanding the possible effects of any risks that may remain with the entity that transferred the

assets. The amendments also require additional disclosures if a disproportionate amount of transfer transactions are undertaken at the

end of a reporting period. Application of these amendments had no significant effect on either the disclosures in the financial statements

or measurement of the related items. For further details see Note 24 (Current debt).

Accounting standards, amendments and interpretations effective from 1 January 2012 but not applicable to the Company

The following amendment, effective from 1 January 2012, relates to matters that were not applicable to the Company at the date of

this Annual Report, but could affect the accounting treatment of future transactions or arrangements:

On 20 December 2010, the IASB issued a minor amendment to IAS 12 – Income Taxes, which clarifies the accounting for deferred

tax on investment properties measured at fair value. The amendment introduces the presumption that the carrying amount of

deferred taxes relating to investment properties measured at fair value under IAS 40 will be recovered through sale. As a result of the

amendments, SIC-21 Income Taxes – Recovery of Revalued Non-Depreciable Assets no longer applies. These amendments are

effective retrospectively for annual periods beginning on or after 1 January 2012

Accounting standards and amendments not yet applicable and not early adopted by the Company

On 12 May 2011, the IASB issued IFRS 10 – Consolidated Financial Statements replacing SIC-12 – Consolidation: Special Purpose

Entities and parts of IAS 27 – Consolidated and Separate Financial Statements (subsequently reissued as IAS 27 – Separate Financial

Statements which addresses the accounting treatment of investments in separate financial statements). The new standard builds

on existing principles by identifying the concept of control as the determining factor in whether an entity should be included in the

consolidated financial statements of the parent company. The new IAS 27 confirms that investments in subsidiaries, joint ventures and

associates are accounted either at cost or, alternatively, in accordance with IFRS 9. The same accounting treatment is to be applied

for each category of investments. Additionally, if an entity elects to measure its investments in associates or joint ventures at fair value

in its consolidated accounts (applying IFRS 9), it should also use the same method for the separate financial statements. The standard

is effective retrospectively, for annual reporting periods beginning on or after 1 January 2014 at the latest. Based on current analyses,

adoption of the reissued IAS 27 is not expected to have any significant effect on the valuation of investments held by the Company.

On 12 May 2011, the IASB issued IFRS 11 – Joint Arrangements superseding IAS 31 – Interests in Joint Ventures and SIC-13 – Jointly

Controlled Entities: Non-Monetary Contributions by Venturers. The new standard provides the criteria for identifying joint arrangements

by focusing on the rights and obligations of the arrangement, rather than its legal form and requires a single method to account for

interests in jointly-controlled entities, the equity method. The standard is effective retrospectively, at the latest for annual reporting

periods beginning on or after 1 January 2014. Following the issue of the new standard, IAS 28 – Investments in Associates has been

amended to include accounting for investments in jointly-controlled entities in its scope of application (from the effective date of the

standard).