Reebok 2010 Annual Report Download - page 242

Download and view the complete annual report

Please find page 242 of the 2010 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248

|

|

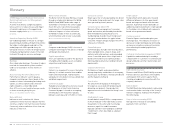

238 Additional Information Glossary

Green grass retailers

Golf distribution channel. Small golf specialty

shops typically located at a golf course.

Gross Domestic Product (GDP)

Market value of all finished goods and services

produced within a country in a given period of

time.

GDP = consumption + investment + government

spending + (exports − imports).

Gross margin

Gross profit as a percentage of net sales.

Gross margin = (gross profit / net sales) × 100.

Gross profit

Difference between net sales and the cost of

sales.

Gross profit = net sales – cost of sales.

H

Halo effect

The halo effect refers to the cognitive bias

effect that when we consider something

good (or bad) in one category, we are likely to

make a similar evaluation in other (related)

categories.

Hardware

Product category which comprises equipment

that is used rather than worn by the athlete,

such as bags, balls, fitness equipment, golf

clubs and hockey sticks.

Hedging

A strategy used to minimise exposure to

changes in prices, interest rates or exchange

rates by means of derivative financial

instruments (options, swaps, forward

contracts, etc.) see also Natural hedges.

I

Institutional investors

Investors such as investment companies,

mutual funds, brokerages, insurance

companies, pension funds, investment banks

and endowment funds. They are financially

sophisticated, with a greater knowledge of

investment vehicles and risks, and have the

means to make large investments.

Interest coverage

Indicates the ability of a company to cover

net interest expenses with income before net

interest and taxes.

Interest coverage = (income before net interest

expense and tax / net interest expense) × 100.

International Financial Reporting Standards

(IFRS)

Reporting standards (formerly called IAS)

which have been adopted by the International

Accounting Standards Board (IASB). The

objective is to achieve uniformity and

transparency in the accounting principles

that are used by businesses and other

organisations for financial reporting around the

world.

International Labour Organization

The International Labour Organization (ILO)

is a specialised agency of the United Nations

that engages in formulating and implementing

international social and workplace standards

and guidelines see also www.ilo.org.

ISO 14001

International Organization for Standardization

(ISO) Standard 14001 specifies the

requirements for an environmental

management system within companies/

organisations. It applies to those environmental

aspects over which the organisation has

control and over which it can be expected

to have an influence (e.g. energy and water

consumption).

J

Joint venture

A cooperation between companies involving

the foundation of a new, legally independent

business entity in which the founding

companies (two or more companies)

participate with equity and significant

resources.

K

Key accounts

Wholesalers or retailers which are primary

customers for the Group and account for a

large percentage of sales.

Kicks

Informal word for athletic footwear.

Kinesiology

The science of the psychological mechanisms

associated with human movement.

L

Leather Working Group

The Leather Working Group (LWG) was

formed in April 2005 to promote sustainable

and appropriate environmental stewardship

practices within the leather industry see also

www.leatherworkinggroup.com.

Licensed apparel

Apparel products which are produced and

marketed under a licence agreement. The

adidas Group has licence agreements with

sports organisations (e.g. FIFA, UEFA, IOC),

sports leagues (e.g. NFL, NBA), professional

teams (e.g. Real Madrid, AC Milan) and

universities (e.g. UCLA, Notre Dame).

Lien

The right to take and hold or sell the asset of a

debtor as security or payment for a debt.

Liquidity I, II, III

The liquidity ratio indicates how quickly a

company can liquidate its assets to pay for

current liabilities.

Liquidity I:

((Cash + short-term financial assets) / current

liabilities) × 100.

Liquidity II:

((Cash + short-term financial assets + accounts

receivable) / current liabilities) × 100.

Liquidity III:

((Cash + short-term financial assets + accounts

receivable + inventories) / current liabilities) × 100.

M

Market capitalisation

Total market value of all shares outstanding.

Market capitalisation = number of shares out-

standing × current market price.

Marketing working budget (MWB)

Promotion and communication spending

including sponsorship contracts with teams

and individual athletes, as well as advertising,

retail support, events and other communication

activities, but excluding marketing overhead

expenses. As MWB expenses are not

distribution channel-specific, they are not

allocated to the Group’s operating segments.

Mono-branded stores

adidas, Reebok or Rockport branded stores

not operated or owned by the adidas Group

but by franchise partners. This concept is

used especially in the emerging markets such

as China, benefiting from local expertise of

the respective franchise partners see also

Franchising.