Reebok 2010 Annual Report Download - page 166

Download and view the complete annual report

Please find page 166 of the 2010 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

|

|

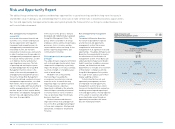

162 Group Management Report – Financial Review Risk and Opportunity Report

We also seek to enhance consumer

demand for our brands through

extensive marketing, product and brand

communication programmes. And we

focus on supply chain improvements to

speed up creation-to-shelf timelines

see Global Operations, p. 106.

Given the broad spectrum of our

Group’s product offering, retailer

feedback and other early indicators see

Internal Group Management System, p. 126, we

view the risk from consumer demand

shifts as unchanged versus the prior

year. We therefore rate the likelihood of

changes in consumer demand as likely,

and the potential financial impact as

moderate.

Industry consolidation risks

The adidas Group is exposed to risks

from market consolidation and strategic

alliances amongst competitors and/or

retailers. This can result in a reduction

of our bargaining power, or harmful

competitive behaviour such as price

wars. Abnormal product discounting

and reduced shelf space allocation from

retailers are the most common potential

outcomes of these risks. Sustained

promotional pressure in one of the

Group’s key markets could threaten

the Group’s sales and profitability

development.

To moderate this risk, we are committed

to maintaining a regionally balanced

sales mix and continually adapting the

Group’s distribution strategy with a

particular focus on controlled space

initiatives see Global Sales Strategy, p. 82.

Although the market capitalisation of

many companies within the sporting

goods industry increased substantially

in 2010, merger and acquisition activity

is forecasted to intensify in the light

of good credit market conditions as

well as improving corporate balance

sheets and business projections. As

a result, we continue to regard risks

from market consolidation as having a

probable likelihood of occurrence. The

potential financial impact is assessed as

significant.

Hazard risks

The adidas Group is exposed to external

risks such as natural disasters,

epidemics, fire and accidents. Physical

damage to our own or our suppliers’

premises, production units, warehouses

and stock in transit can lead to property

damage and business interruption.

These risks are mitigated by loss preven-

tion measures such as working with

reliable suppliers and logistics providers

who guarantee high safety standards. In

addition to the insurance coverage we

have secured, the Group has also imple-

mented contingency plans to minimise

potential negative effects.

We assess the potential occurrence of

hazard risks as unlikely. In connection

with the adjustment of our risk method-

ology in 2010, however, we have changed

our assessment of the potential financial

impact. Should those risks materialise,

we now expect hazard risks to have a

major financial impact, reflecting the

fundamental and devastating conse-

quences natural disasters or terrorist

acts might have on our business on a

theoretical basis.

Risks from loss of brand image

The adidas Group faces considerable

risk if we are unable to uphold high

levels of consumer awareness, affiliation

and purchase intent for our brands. In

addition, if the Group’s brands are not

allocating sufficient marketing resources

to activate our sports assets and brand

campaigns in a sustainable manner,

we face the risk of fading consumer

awareness and attractiveness. To

mitigate these risks, we have defined

clear mission statements, values and

goals for all our brands. These form the

foundation of our product and brand

communication strategies. We also

continually refine our product offering to

meet shifts in consumer demand and to

contemporise our offering to respond to

current trends.

Central to all our brand initiatives is

ensuring clear and consistent messaging

to our targeted consumer audience.

Market share gains at TaylorMade as well

as adidas’ achievements at the 2010 FIFA

World Cup give us confidence that brand

image risks for these brands are unlikely.

In addition, the successful introduction of

new Reebok product initiatives such as

in the toning category and ZigTech has

helped to stimulate consumer interest

and improve Reebok’s brand image.

Aggregating these factors, we

believe that the risk from loss of brand

image for the Group has only a possible

likelihood of occurrence. Nevertheless,

a considerable deterioration in brand

image could have a significant financial

impact on our Group.

Own-retail risks

New adidas, Reebok and Rockport

own-retail stores require considerable

up-front investment in furniture and

fittings as well as ongoing maintenance.

In addition, own-retail activities often

require longer-term lease or rent

commitments. Retail also employs

significantly more personnel in relation

to net sales than our wholesale business.

The higher portion of fixed costs

compared to our wholesale business

implies a larger profitability impact in

cases of significant sales declines.